Currently, ASX leading Financials are being dragged higher as the US equity rally continues into the lead up to their fourth quarter earnings results. We’re somewhat sceptical of the valuation support and yesterday started hedging our banking exposure in client portfolios. This was done through using in-the-money European-style calls over CBA and slightly in the money February calls over NAB, as two examples.

In the case of CBA, we stay exposed to the February dividend and franking credit but have hedged a price pullback of up to 5% between now and March.

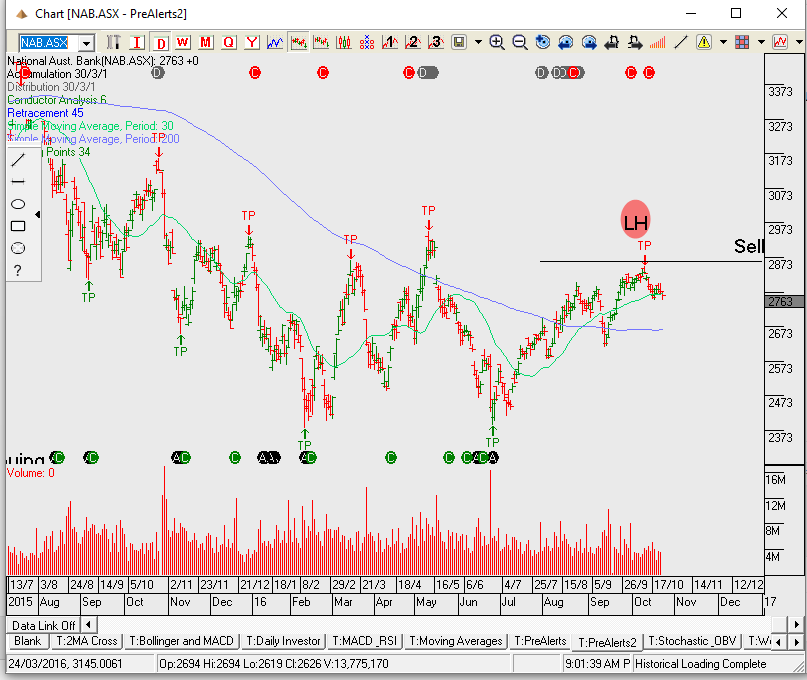

In NAB, we’ve hedged to a similar extend but without the need to protect the dividend. NAB’s next payment period is not until May

There is a saying in the financial markets that a “rising tide floats all boats” This old adage has been used recently to describe how the rally in US bank shares has lifted the share prices of Australian banks.

Since November 4th, shares of Citibank have gained 14%, shares of JP Morgan have gained 16%, shares of Bank of America have risen by 17% and Goldman Sachs shares have rallied by over 20%.

Over the same period of time, shares of ANZ have gained 6%, shares of Westpac have gained 8%, CBA shares have lifted by 8.5% and shares of the NAB have rallied by 11%.

Interest rates in the US began bottoming out in late September, which was positive news for most US financial names. In addition, the election of Donald Trump is being hailed as a “game changer” for the U.S. banking sector, as the Republican sweep of the White House and both houses of Congress appears to have shifted investor’s expectations about interest rates, regulation and the broader business environment.

With respect to the Australian banking names, these two key points aren’t applicable.

The RBA may have moved to a neutral bias on domestic interest rates, but there’s no realistic expectations for a rate hike anytime in the foreseeable future. And, if any regulatory changes are legislated in the Australian banking industry over the next 12 months, they are more likely to be restrictive, as opposed to accommodative.

With this in mind, we will use this recent rally in Australian banking names to implement our derivative overlay strategy and sell covered call options to enhance returns on bank share holdings.

Stay tuned to the Investor Signals daily blog for specific timing and price information.

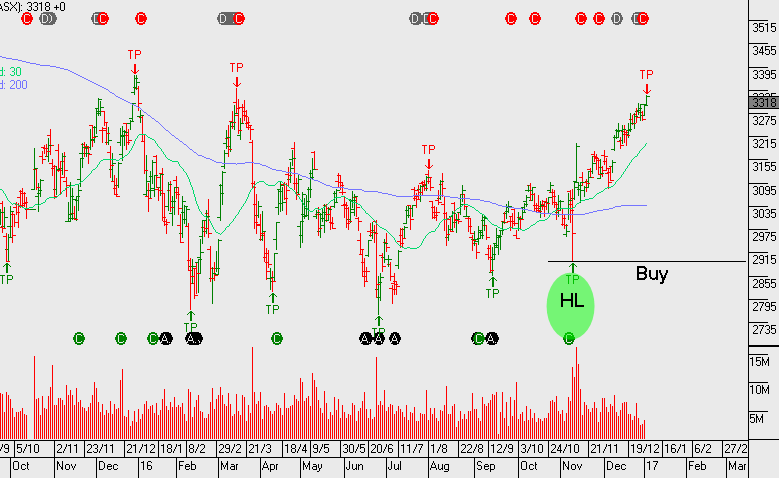

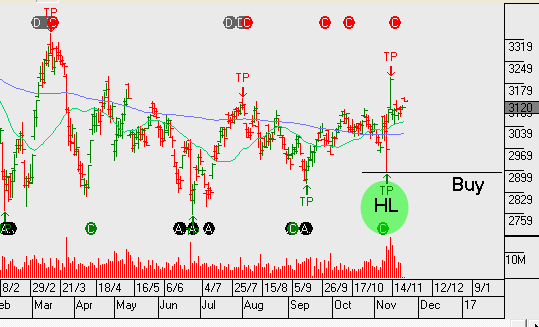

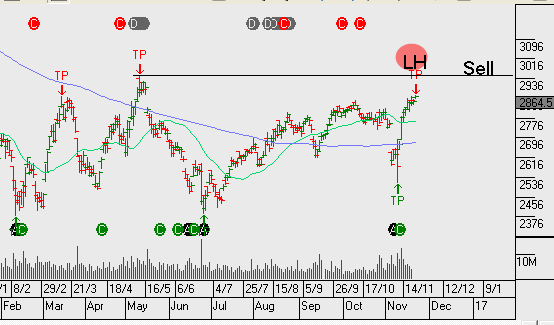

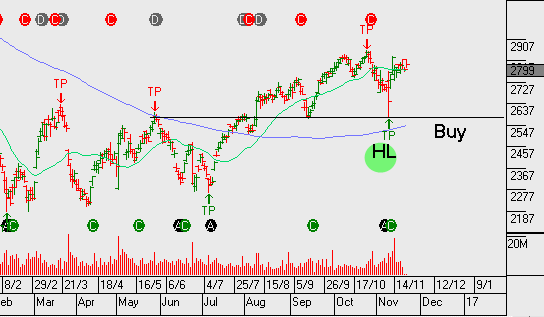

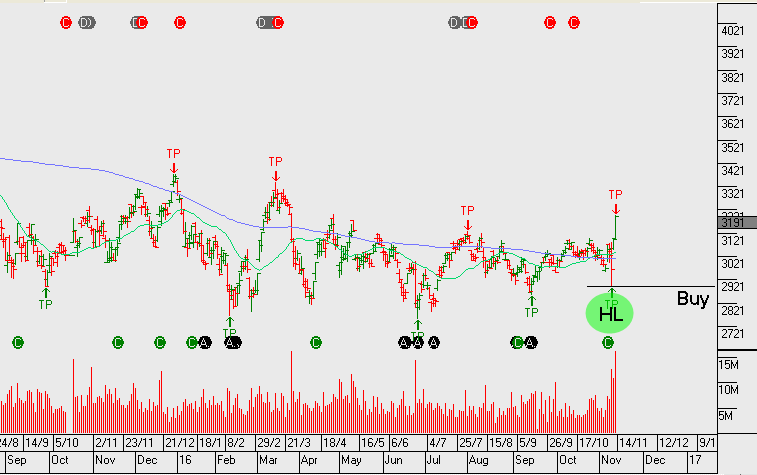

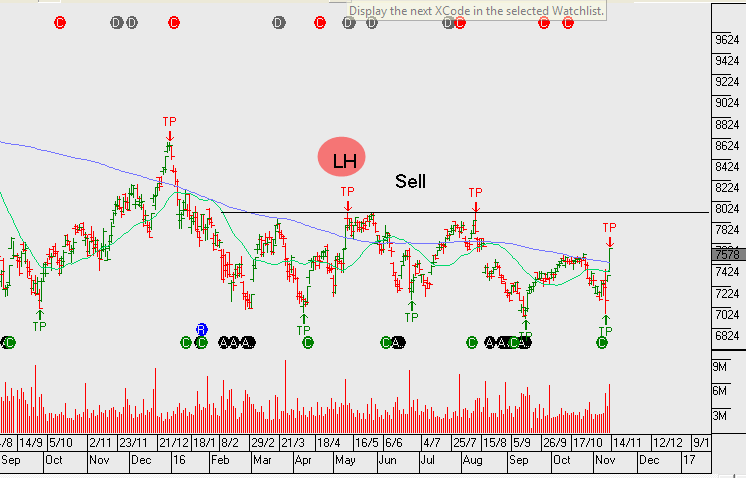

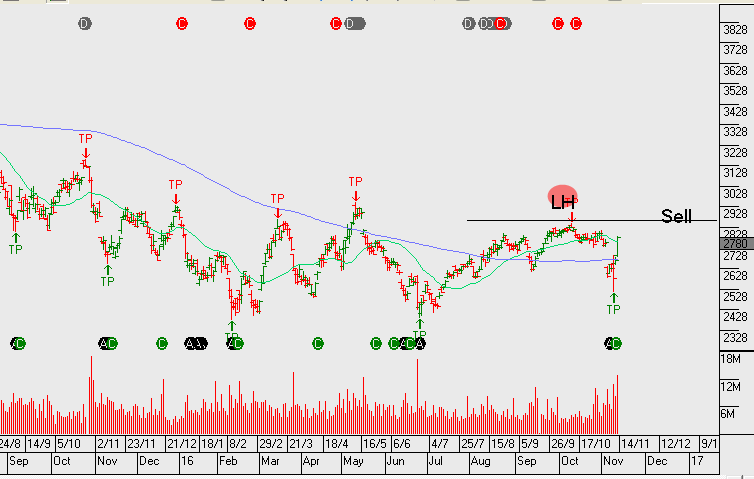

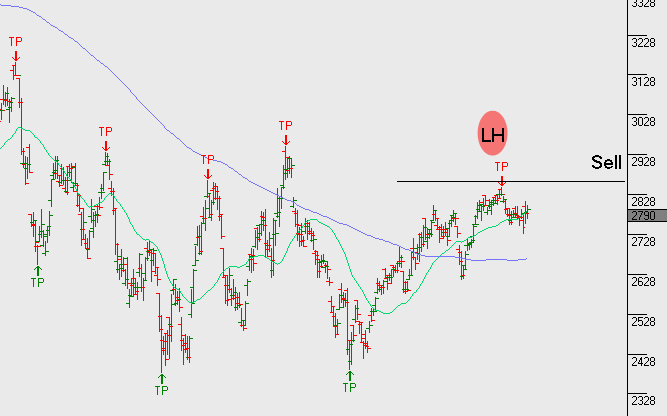

We now have ANZ and WBC creating a higher low formation. However, CBA and NAB still remain below the recent highs within the downtrend that’s been in place since May 2015.

Back in August, ANZ was the first to break the downtrend and now WBC has followed. Within the regional banks, between BOQ and BEN, it’s Bendigo that’s displaying a more bullish price pattern.

Although the breakout in financials is strong at present, we don’t see too much further upside. As reflected in the recent earnings results, the banks are having difficulties growing top line revenue. Our largest bank exposure in client portfolios is Westpac. We’ve left this name uncovered at present, however, it’s likely we’ll identify a point this week to add covered calls to enhance the yield.

ANZ goes ex-dividend $0.80 on Monday & WBC also goes ex-dividend $1.00 on Monday.

National Australia Bank delivered 2H16 earnings which showed strong organic capital generation and underlying earnings trends that were relatively strong compared to their banking peers. In addition, it’s also worth noting that the SME business segment is showing early signs of a pickup in credit growth; this is an area where NAB has traditionally led its competitors.

NAB trades on almost a 10% discount to its peers and we may begin to see scope for this discount gap to close.

Consistent across all the major banks, we continue to see mortgage margins under pressure. This remains a concern, especially for Westpac and CBA as they’re likely be impacted the greatest by declining mortgage margins.

NAB FY17 underlying profit is expected to be $10b on EPS of $2.30 and DPS of $1.70 placing the stock on a forward yield of 6.5%.

Financials globally are getting a boost following the US election, however, we remain cautious and look to sell call options into the rally.

Shares of the National Australia Bank (NAB) are pushing back toward the $28.00 level after announcing that its final dividend will be unchanged at 99 cents per share as full-year cash earnings rose 4.2% to $6.48 billion.

Forward guidance suggests a drop in FY17 dividend to 85 cents as bad and doubtful debt charges rose 7.0% to $800 million, expenses rose 2.2% and net interest fell to 1.88%. Based on these figures, the FY17 growth forecast of -1% is the lowest in the sector, which is likely to limit further out performance to peer banks in the near-term.

The forward guidance equates to NAB trading on a P/E multiple of 12x , which is a 6% discount to peers, and a forward yield of 6.2%

NAB is scheduled to report its FY16 result on Thursday and we’re expecting FY16 cash earnings of $6.4b. The final dividend will likely be around $0.98 fully franked & we continue to expect the dividend to be cut next year.

We are forecasting a 2H16 credit impairment charge of $500m which is an increase of $125m on the 1H16 number.

Based on a slight reduction in dividends the FY18 yield is 6.75%.

Selling covered calls at or near $28.50 into early next year, with a view towards collecting the upcoming dividend is our preferred strategy.

NAB.ASX reported 3Q16 cash profit of $1.6bn for the quarter, slightly below consensus forecasts with revenue down but offset by better than expected cost management.

FY17 dividends are expected to be around $1.70 placing the stock on a forward yield of 6.1%.

Sophisticated Investor?

We have special opportunities available for Sophisticated Investors. If you're interested, and qualify, please provide your details below.