Honeywell International Inc. – Common strategic separation of the Aerospace division is finalized for 29 June 2026. Additionally, its quantum computing subsidiary, Quantinuum, has filed for an IPO (ticker: QNT).

Announced on 8 May that its quantum computing subsidiary, Quantinuum, has publicly filed for an IPO (ticker: QNT). The 2026 Annual Shareowners Meeting is scheduled for 22 May 2026.

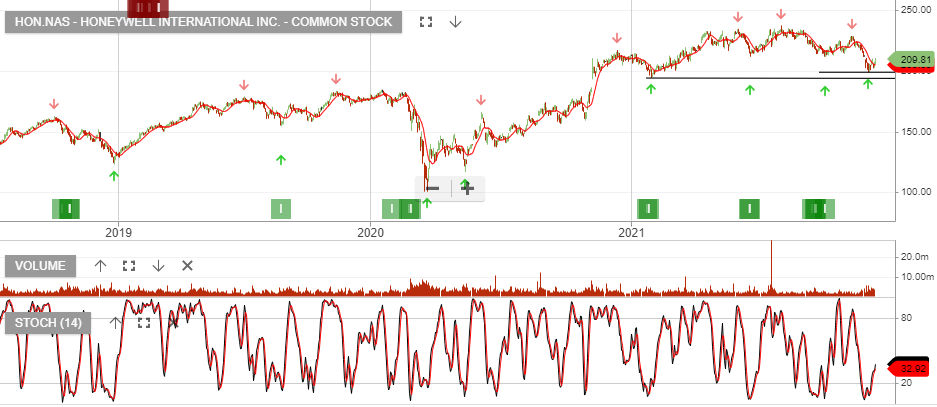

Honeywell International Inc. – Common is currently a “transformation play.” While near-term revenue headwinds and supply chain issues are weighing on the stock, the June 29 Aerospace spin-off is the primary catalyst we’re watching.

Q1 2026 Earnings Highlights (Released April 23, 2026) Honeywell reported mixed results for the first quarter of 2026:

Adjusted EPS:$2.45, beating the analyst consensus of $2.32 (up 11% year-over-year).

Revenue:$9.14 billion, missing the estimated $9.30 billion. Organic sales growth was 2%, slowed by mechanical supply chain constraints in Aerospace and geopolitical disruptions in the Middle East.

Margins: Segment margins expanded 90 basis points to 23.3%, driven by strong pricing discipline and cost removals.

Backlog: Rose 15% to a robust $38 billion, indicating strong future demand.

Strategic Catalyst: The Aerospace Spin-Off The biggest upcoming driver for HON is the planned separation of its Aerospace business:

Spin-Off Date: Scheduled for June 29, 2026.

Objective: To create two “pure-play” companies: one focused on Aerospace Technologies and the other (RemainCo) on Industrial/Building Automation and Energy.

Divestitures: Honeywell also recently announced the sale of its Warehouse and Workflow Solutions (WWS) and Productivity Solutions and Services (PSS) businesses, expected to close in the second half of 2026.

Consensus:“Moderate Buy” with 13 Buy ratings and 8 Hold ratings.

Price Targets: Analysts have a median target of $245.00 – $250.21, implying a potential upside of roughly 15-20% from current levels.

Recent Changes: Following the revenue miss, firms like Citigroup and Barclays slightly lowered their price targets (e.g., Citi from $265 to $257) but maintained “Buy/Overweight” ratings, citing long-term value in the portfolio breakup.