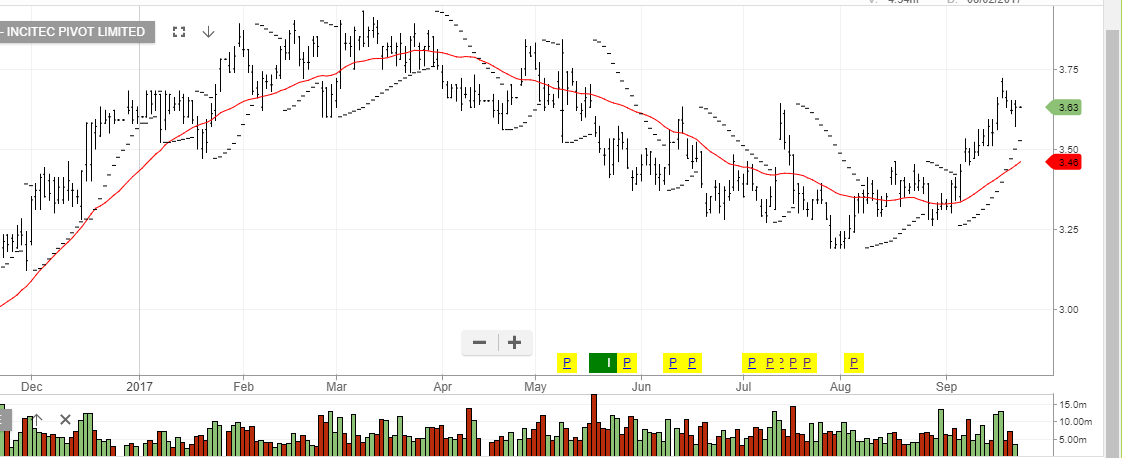

ALGO Update: Buy The Dip In IPL

On August 5th, we posted a buy signal on IPL at $3.20. Since then the stock has traded as high as $3.72, but slipped lower into the weekend.

One of the market stories supporting IPL has been that company officials have been actively buying shares, which is usually a good reflection of the company’s earnings and growth outlook.

More importantly, analysts’ earnings growth expectations of 90% over the next three years also illustrates a buoyant outlook for the business.

We still prefer the long side of IPL and suggest that investors could look to buy a pullback into the $3.45 support level.

Incitec Pivot

ASX XJO Index

ASX XJO Index Fortesque Metals Group

Fortesque Metals Group Ramsay Health Care

Ramsay Health Care Tabcorp

Tabcorp

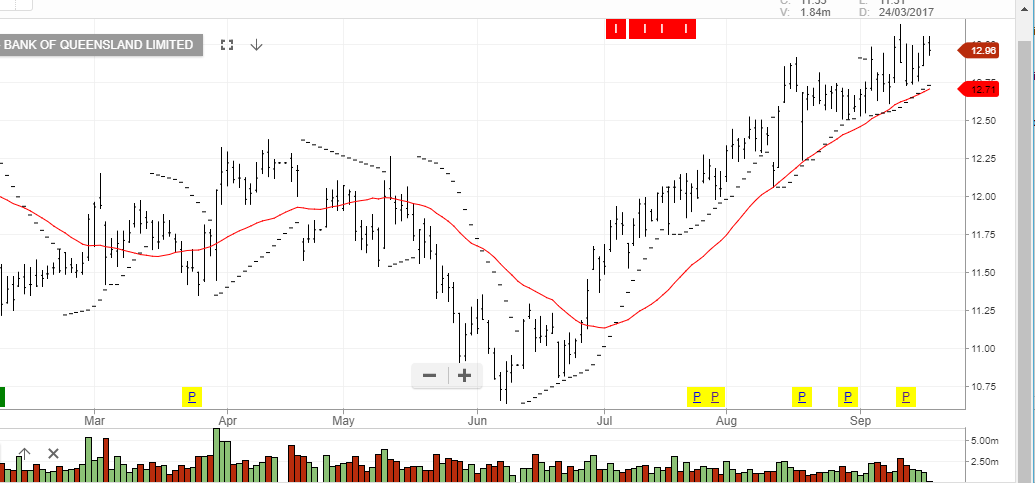

Bank of Queensland

Bank of Queensland