BHP Group is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

The company announced its FY19 earnings, which were in line with consensus expectations. Operating costs are slightly elevated but high iron ore prices will offset this in FY20.

FY19 reported EBITDA US$23.2bn and underlying attributable profit of $9.1bn. The market was disappointed that no buyback was announced but BHP did declare a final div of US$0.78 per share.

Total dividends for the year were US$1.33 per share, based on 74% payout ratio.

FY20 revenue is forecast to be $48bn, EBIT $19bn, net profit $11.5bn, which will place the stock on a 10x PE multiple and a forward yield of 6.5%.

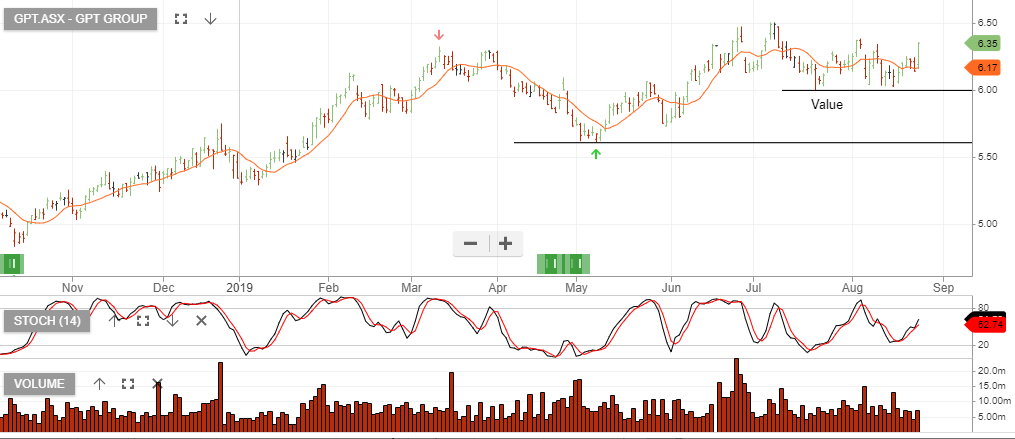

We see value support for BHP & RIO near the current price range.