ASX – Buy Near $58.00

Our Algo Engine triggered a buy signal in ASX recently and with the stock now moving into our targeted “value range”, we will begin accumulating.

ASX

Our Algo Engine triggered a buy signal in ASX recently and with the stock now moving into our targeted “value range”, we will begin accumulating.

ASX

Lendlease, ASX, CSL and Aristocrat are names that we covered in Monday’s Opportunities in Review webinar.

Again, we draw your attention to these high quality businesses that have seen a recent correction in their share price.

We believe these names are close to finding support and should be the focus of establishing entry conditions. Watch the short-term momentum indicators for a reversal higher.

Click below to watch the short two minute video

Both AMC and TCL have been under recent selling pressure as bond yields in the US have moved higher.

The defensive nature of both businesses has seen their share price trade as a proxy to bonds.

With TCL and AMC both scheduled to have their AGM tomorrow, we believe there could be a rally in the share price as investors gain more clarity on future earnings growth.

We’re mindful that Algo Engine sell signals are displayed, however we’re willing to commit to Amcor as our preferred opportunity, of the two names.

Amcor

Our Algo Engine triggered sell signals across the domestic banking names back in June.

Since then, on average, the group has sold off approximately 15% and on a 2-year basis, the sector is now down more than 30%.

ANZ announced this week, that its 2H18 cash earnings will be adversely impacted by $711m of after-tax charges related to legal costs and customer remediation from the Royal Commission.

ANZ releases their full-year NPAT on October 31st.

A second sector risk yet to play-out, is the potential for deteriorating credit quality. This risk has been exacerbated over recent years by “add backs”, where short term earnings are improved through lowering the provisions for bad loans.

Looking ahead, CBA chief Matt Comyn will face the royal commission on Thursday morning, followed by WBC’s Brian Hartzer Thursday afternoon and ANZ’s Shayne Elliott on Friday.

During the recent run-up in US interest rates, yield sensitive names have faced heavy selling pressure over the last 8 weeks.

However, as a “risk off” wave now appears to be hitting equity markets, it’s likely bond yields will consolidate, and in the process provide some selling reprieve for the yield sensitive names.

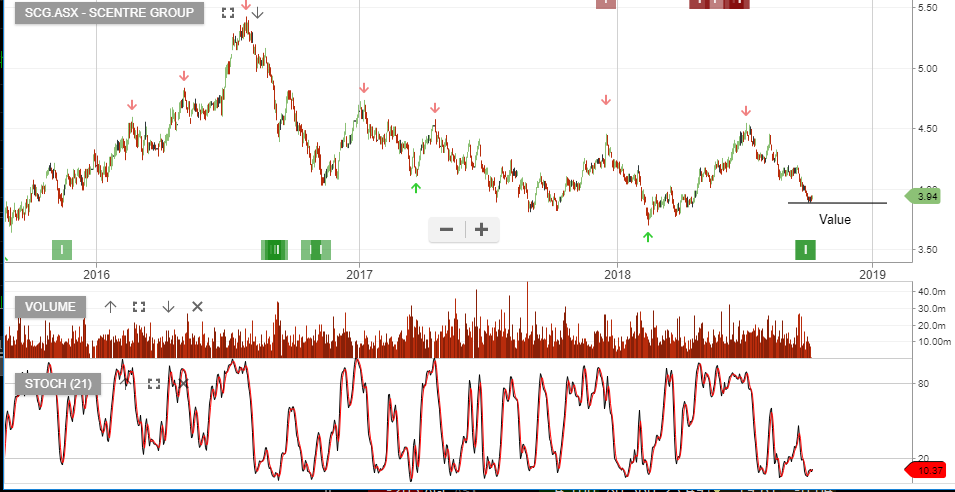

SCG and SYD are two examples where we now feel the prices reflect good value.

Sydney Airport

Scentre Group

Our Algo Engine has generated buy signals in both Webjet and Flight Centre over recent days. We continue to like the supportive earnings backdrop for WEB & FLT and therefore, we’re adding these names to our watch list.

The charts below show the slightly discounted entry levels we’re looking for.

Join our “Opportunities in Review” webinar on Monday to learn more about our high conviction ideas.

Our Algo Engine generated a buy signal in ASX recently and we recommend to keep this name on your watch list.

Our target is for a sub $60.00 entry level, where we feel buying support will begin to build.

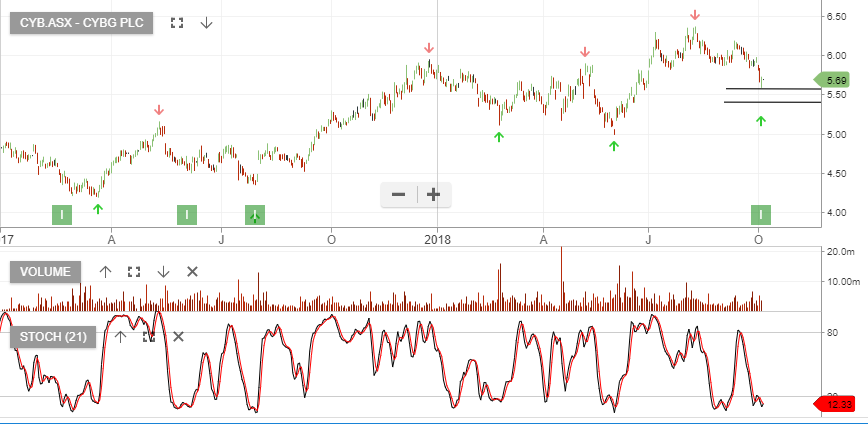

Our ALGO engine triggered a buy signal for CYB into yesterday’s ASX close at $5.69.

This “higher low” pattern is referenced to the intra-day low of $5.20 posted on June 4th.

CYB at $5.50 – $5.60 appears to be a good buying opportunity. We expect earnings upgrades next year following integration with Virgin Money.

CYB

AGL is a current holding within the ASX Top 50 and 100 model portfolios.

With the share price trading at $19.50, we consider a pessimistic view is now priced in.

We suggest buying AGL and looking to sell covered call options to enhance the cash flow.

Qantas will provide its 1Q19 trading update on 25 October 2018.

QAN was added to our ASX Top 50 model portfolio in July of 2017 at $5.25.

Due to the recent spike in oil prices, the share price has been drifting lower and nearing our original entry level.

Along those lines, we expect the trading update to include how the company’s dynamic hedging program is insulating their bottom line from higher fuel prices.

We see good value at current levels for a move back into the $7.90 area over the medium-term.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453