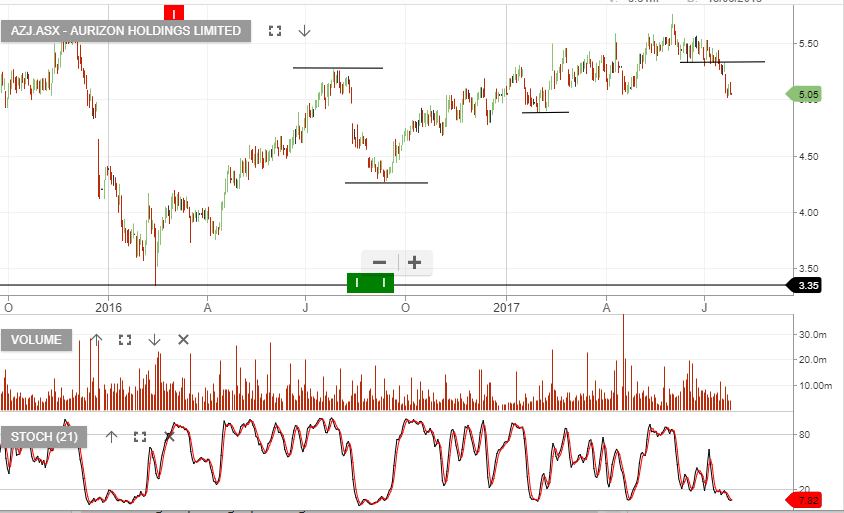

AZJ – Selling Pressure

AZJ has recognised an A$526m impairment to its Bulk assets, and continues its Inter-modal review.

AZJ noted continues to face challenging market conditions and we feel investor sentiment will be negative leading into the FY17 results on 14 August 2017.

AZJ has previously guided towards FY17 EBIT within A$800-850m range.

Regular viewers of the ASX top 50 video market report, will recognise AZJ as a stock we’ve been warning about, in 2017. Our concern relates to the sustainability of the high dividend payout ratio and the probability of the company being forced to announce a cut at the August result.