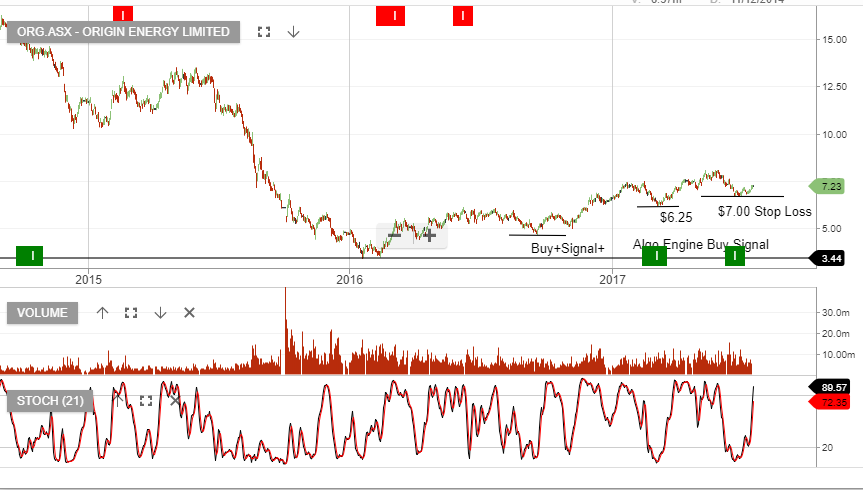

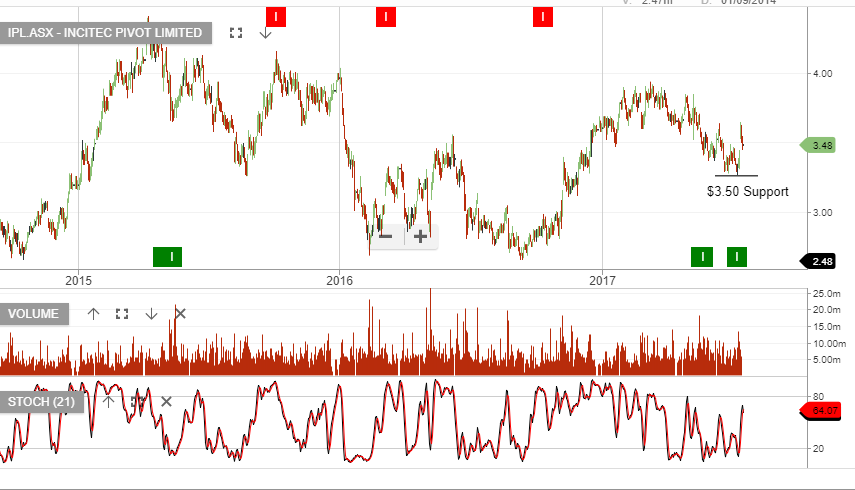

Algo Update – AMC & IPL

We continue to like the buy-side opportunity in AMC and IPL, following the recent Algo Engine buy signals.

We continue to like the buy-side opportunity in AMC and IPL, following the recent Algo Engine buy signals.

MPL, SHL & CSL are worth adding to your watch-list. We see the current price levels in these names, at or near new buying support.

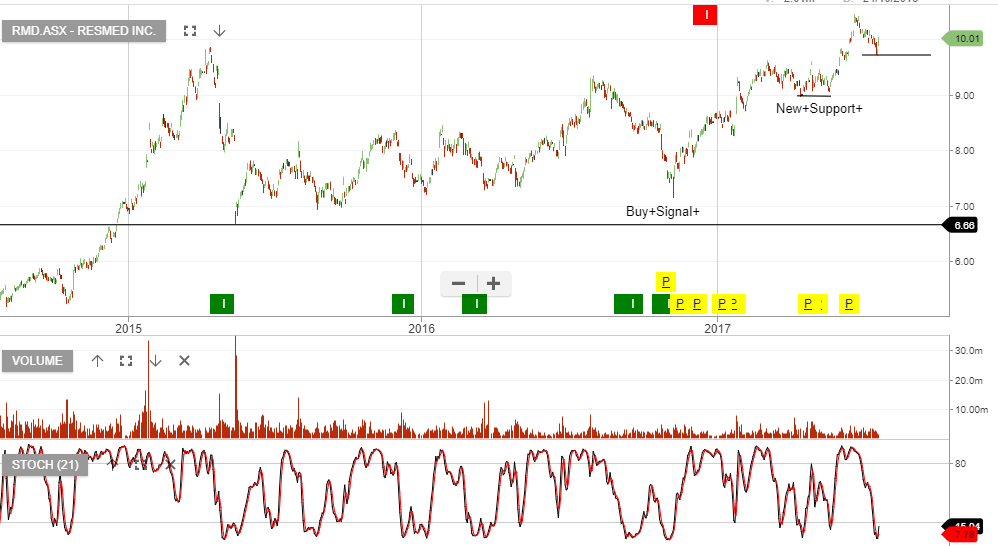

Our Algo Engine has triggered multiple buy signals in Resmed, since the stock price began a series of “higher low” formations going back to 2015.

The recent strong rally started in late 2016 after making a low at around $7.00.

With the stock now trading at $10.00, the PE is pushing into the high 20’s.

The upcoming earnings result on the 2nd August will have to deliver 10 – 15% underlying EPS growth to meet market expectations.

CIMIC has reported a solid interim earnings result. The company delivered a 22% increase in NPAT to $323m.

We expect 10 – 15% EPS growth into FY18, placing the stock on a forward yield of 3.7%

Our Algo Engine triggered a recent buy signal in CIMIC at or near $37.50.

Crown Resorts is likely to announce further capital management initiatives at the FY17 result on 4th of August.

Crown recently sold its remaining stake in MLCO, realizing net proceeds of A$1.3b. Our view is that these proceeds will be used to either reduce debt, or embark on the next stage of its capital management program.

Our Algo Engine triggered a recent buy signal at or near $12.00

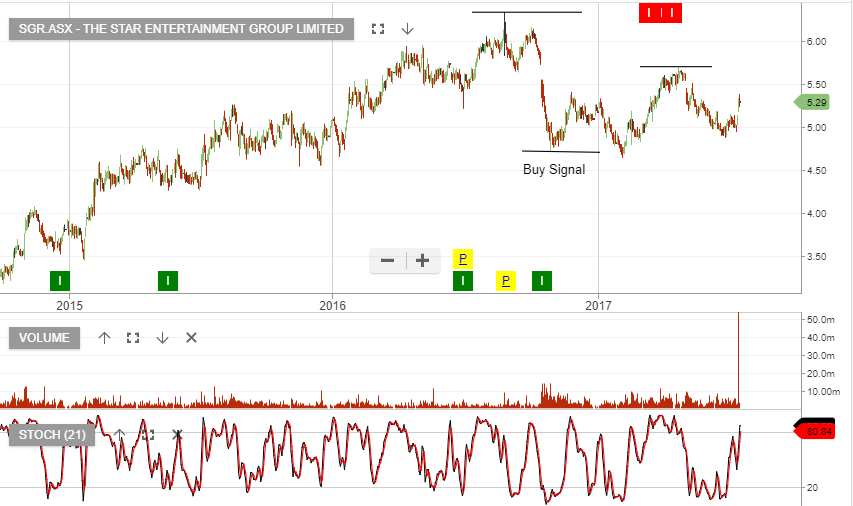

The Australian-listed Star yesterday informed its investors that Ellerston Capital (25% owned by James Packer) now has a 5.07% stake.

Institutional investor, Perpetual, which is already Star’s biggest shareholder, also increased their holding when Malaysian casino giant Genting sold down its stake.

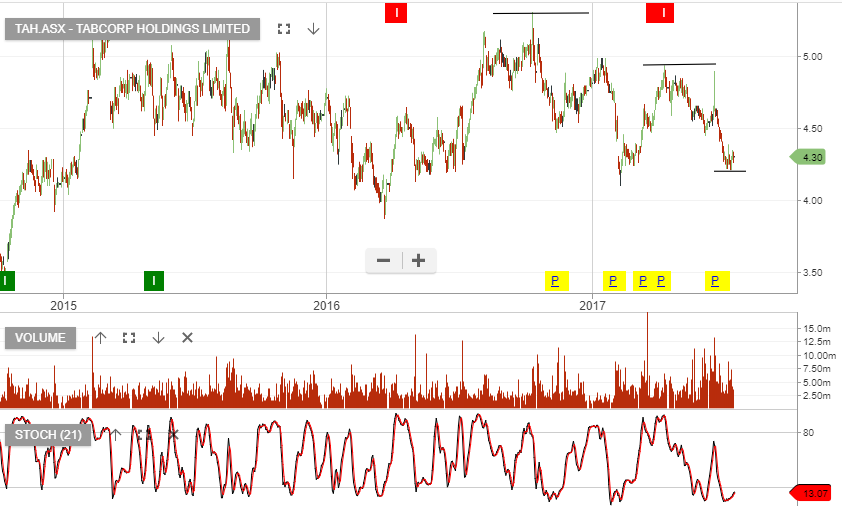

Star & Tabcorp have “lower high” formations, where as Crown is displaying a bullish, “higher low” formation.

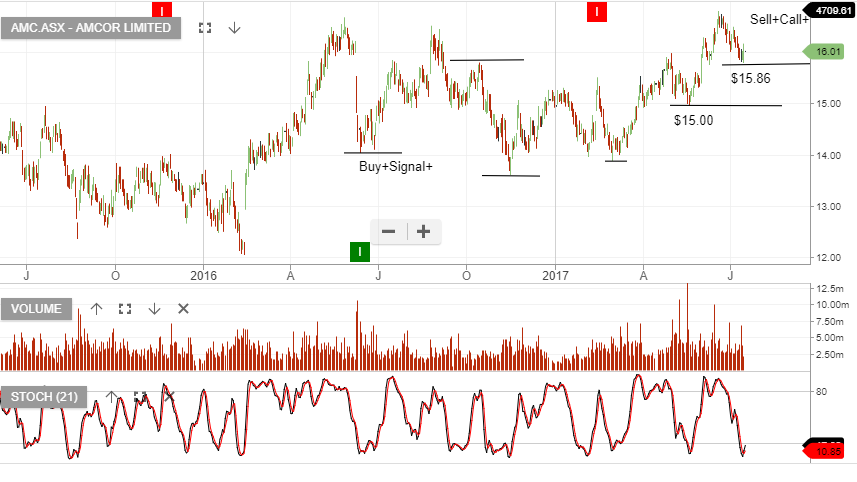

Amcor is trading on a high multiple of 19x forward earnings and a 3.8% dividend yield. However, the earnings are relatively defensive and we’re expecting 8% underlying EPS growth.

The stock should find support at or near $16 and is an appropriate consideration as a buy-write for client portfolios.

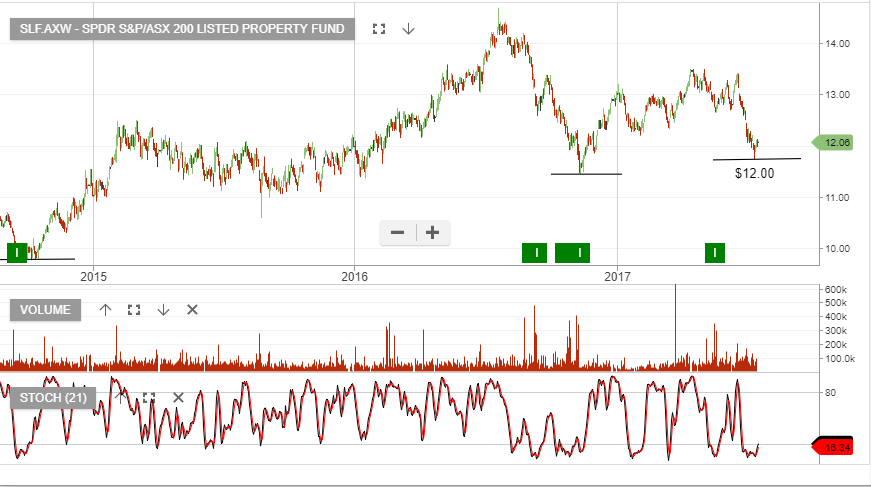

We’ve been highlighting the buying opportunities in WOW, ORG, IPL, GPT, TCL & SYD over the last few weeks.

We continue to like these names and see supportive technical and fundamental factors, which we believe will create investor value.

Our Algo Engine recently triggered a buy signal in a number of ASX listed REIT’s as well as the SPDR Property Fund ETF.

Looking at the buying interest in US REITs across the last few trading sessions, we anticipate similar support for the sector on our local market.

Our Algo Engine is flagging the “higher low” formation in OGC and it appears the stock is now trading in an oversold range.

Watch the short-term momentum indicators for a positive reversal and then apply a stop-loss below the final pivot point.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453