Algo Signal – Buy Graincorp

Our Algo Engine has triggered a buy signal in GNC. The price action has now retraced back to $9.00 and filled the price gap from mid-May.

Our Algo Engine has triggered a buy signal in GNC. The price action has now retraced back to $9.00 and filled the price gap from mid-May.

The S&P/ASX 200 Index finished the week up 1.08%.

The best performer was the Energy sector, up 2.7% & the worst performer was the Health Care sector, down 1.1%.

The XJO continues to trade below the recent 5850 “lower high” formation.

Our Algo Engine flagged a recent buy signal in TWE at or near $12.30.

The recent share pullback creates an attractive entry point. Asia demand looks strong and FY18 earnings should see underlying profit increase over 20% to $360 million.

We believe TWE is still in the early stages of building a significant business across Asia, which will help to support the “buy on the dip” approach.

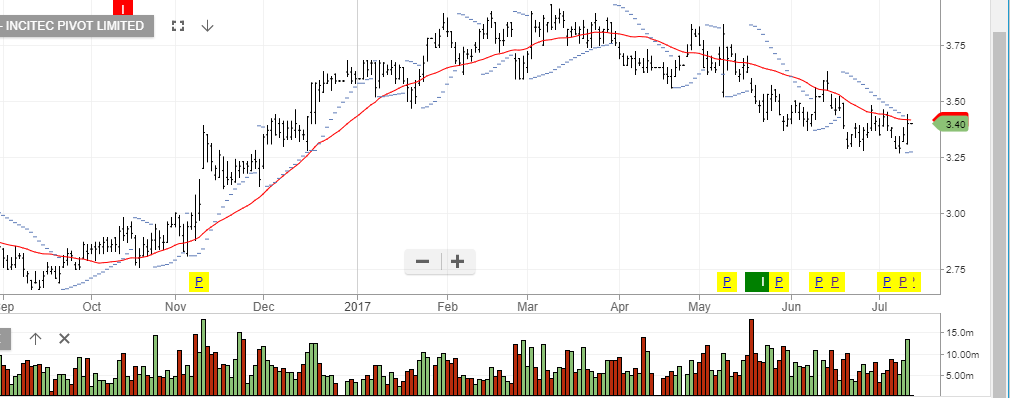

On 11th of July we reminded readers of the blog that we viewed the recent Algo Engine signal on IPL, as one our preferred buy-side signals.

IPL today has opened up 6.5% higher and is now up over 10% from the recent low.

Considering the recent volatility in fertiliser prices, we suggest taking profits in the current $3.55/60 price range.

Incitec Pivot

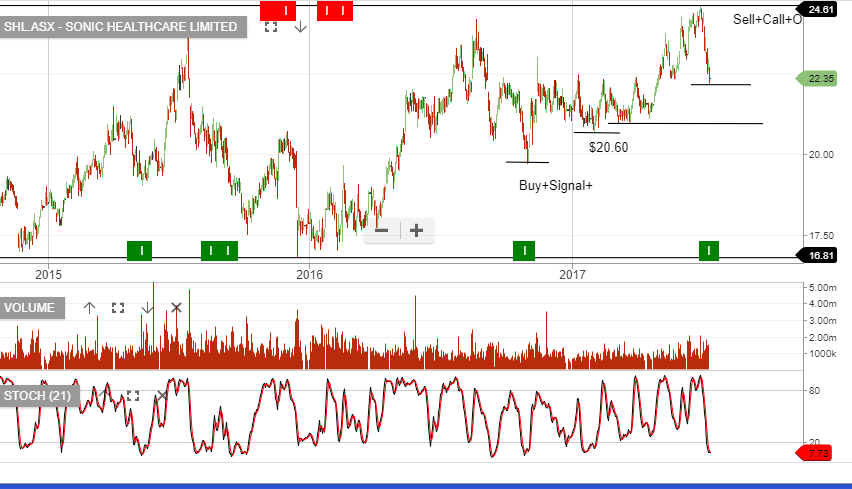

Our Algo Engine triggered a buy signal in Sonic Healthcare, following the recent sell-off from $24.60 back down to $22.30.

We continue to see Sonic delivering 6 – 8% EPS growth and a 3.7% dividend yield. The stock is fair value at or near the current price and investors can consider SHL as a suitable buy-write for enhancing portfolio cash flow.

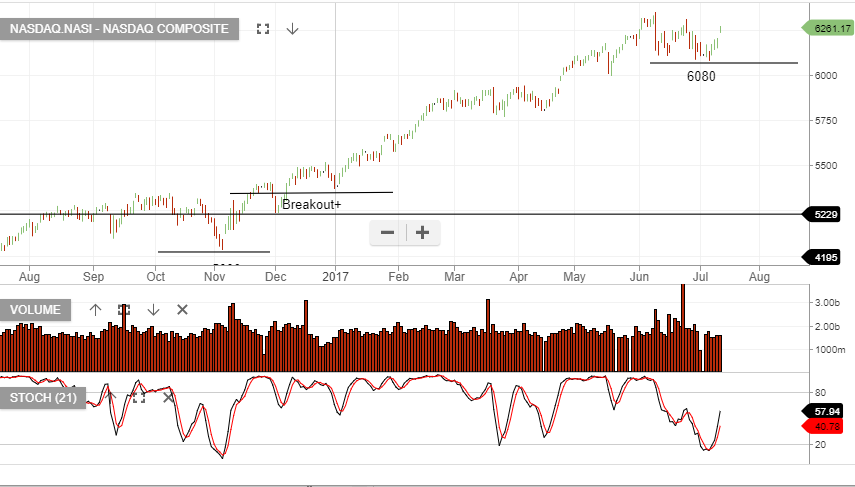

The Dow Jones and NASDAQ charts below show the indices continuing with the “higher high and higher low” formation.

The XJO shows a slightly more bearish pattern, as our local market struggles below the recent 5850 high.

Recent Algo Engine buy signals in BSL and AWC have performed well, with prices rallies of 20%+ in the past few months.

China has been ramping up production of both alumina and aluminium in the lead-up to potential capacity cuts. Alumina Ltd (AWC) is potentially the largest beneficiary, given it is a pure-play on the industry.

Rio Tinto and South32 also seem well-placed to benefit. We will reconsider these names on the next Algo Engine buy signal.

We’ve been buyers of BHP on the recent pullback to $22.50 with an upside target of $25 – $26.

We advise, either locking in gains within this price range, or alternatively, selling at-the-money call options into September.

We continue to like the setup in CTX, WOW and IPL. We also feel that TCL and SYD are now approaching oversold levels.

Our Algo Engine triggered a sell signal in GE back in December 2016.

At that time GE was trading at or near $32.50 and since then the stock has sold off and is now trading $26.00.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453