XJO – Chart Update

The ASX 200 (XJO) is only 10 points away from testing the 5611 high set on the 1st of August 2016.

The ASX 200 (XJO) is only 10 points away from testing the 5611 high set on the 1st of August 2016.

Cochlear generated an algo buy signal at $114 and it looks like the price may build a base and trade higher. Apply a stop loss on a break of the $113 December low.

Crown Resorts has announced several changes to their strategic business plan to simplify the business and enhance their balance sheet.

The firm has decided to cancel its Alon project in Las Vegas, sell off a major stake in its Macau casino business and cancel plans to spin off its international business.

The company will sell off almost half of its holdings in Melco Crown Entertainment for $1.6 billion, using the proceeds to cut debt, pay a special dividend of $500 million and enable a share buyback of around $300 million. Crown’s share of Melco’s annual net profit dropped by 60% in 2016 to $43 million following a corruption crackdown by Chinese authorities.

We still like the long side of CWN, although our upside target has been lowered from $14.00 to $12.50 following earnings revisions due to CWN’s reduced stake in Melco. CWN currently trades on 10x FY 17 estimated EBITDA and is on pace for a 5% yield for FY 2017.

Caltex delivered upbeat profit guidance following strong performances in Lytton and Marketing & Supply divisions. Fy17 revenue $16b, EBIT $900m on EPS of $2.30 and DPS of $1.20. This represent year on year underlying growth of around 10%.

The chart below shows the market’s favourable reaction to the updated guidance with CTX rallying $1.40 from yesterday’s session lows. CTX trades on Fy17 PE of 13x and 4% dividend yield.

Here is our strategy recommendation on Caltex…

Buy CTX at market, sell May $32.50 call for $1.00 credit. March dividend will be $0.50+

Total return if exercised 13%+ in 5.5 months.

A quick look at the ASX top 50 following the overnight FOMC meeting.

The US Stock market slipped lower on the back of the Federal Open Market Committee’s (FOMC) policy announcement today. The market wasn’t surprised by the FED’s 25 basis point increase in the Overnight Fed Funds target, but the “Dot Plot” forward guidance shows policymakers are looking for 3 rate hikes of 25 basis points in 2017.

This view is more aggressive than the 50 basis point move the FOMC discussed back in September, which pushed equities lower and lifted the yield on the US 10-year treasury notes to a three year high of 2.57%. It’s worth noting that the 10-year yield traded at 1.35% in July; which means the yield on the US benchmark treasury note has essentially doubled in less than 5 months.

In her post-announcement press conference, FED chief, Janet Yellen, described the move as a “very modest adjustment”, which suggests this year’s forward guidance may mean another move on rates as early as May 2017.

We don’t see this a trend-changer in the major US stock indexes. However, we do see scope for a near-term correction back to the 19,450 level in the DOW Jones 30 and a move back to 2190 in the SP 500.

This is a 5 minute video looking at the buy and sell signals within the Dow Jones top 30 stocks.

Investor Signals now offers US stocks and we can work in partnership with you to build and manage a portfolio that captures both long and short trading signals.

email me leon@investorsignals.com if you’d like to discuss what we can do to help with your US portfolio exposure.

Over the last four years, Wesfarmers’ share price has traded in an $8.00 range between $38.00 and $46.00. Although the diversified company has consistently paid out fully franked dividends and has been yielding around 5% over the past few years, the lack of share price appreciation has been a concern for longer-term shareholders.

While the Bunnings division of the company has been gaining market share with the demise of Masters, it seems the market rates Wesfarmers earnings lower reflecting a view that the Coles division faces increased competition from the discount chain, Aldi.

Wesfamers has also entered the UK hardware sector with the acquisition of Homebase January of this year, which has yet to show a similar level of success as the Bunnings division.

We don’t expect the limited upside of the share price to improve anytime soon and will continue to employ the covered call strategy on rallies up to the $43.00 area; collecting the franking credits, a dividend of over $2.00 per share and the option premium. Our strategy is helping to boost cash flow to 13%+ per annum

Short trades carry more risk than we’d like at present, due to the strength in global equity indexes. We mange this through running tight stop losses.

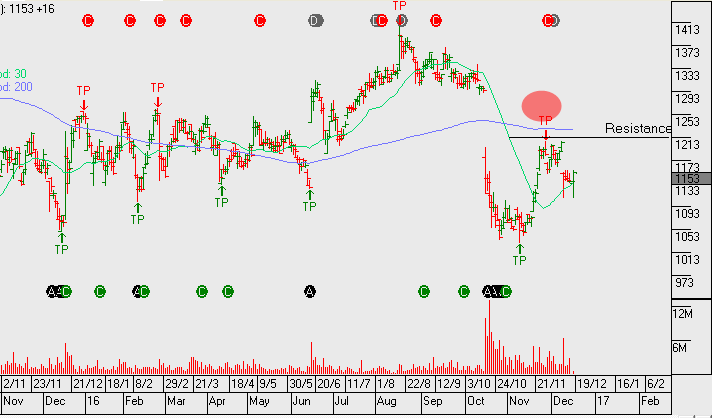

Suncorp has now filled the price gap and we may see buying exhaust at or near today’s high price of $13.65

We’re watching Qantas on the short side. Resistance at $3.60 is likely to cap any rally and momentum will remain weak whilst oil prices trade higher following the OPEC cuts.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453