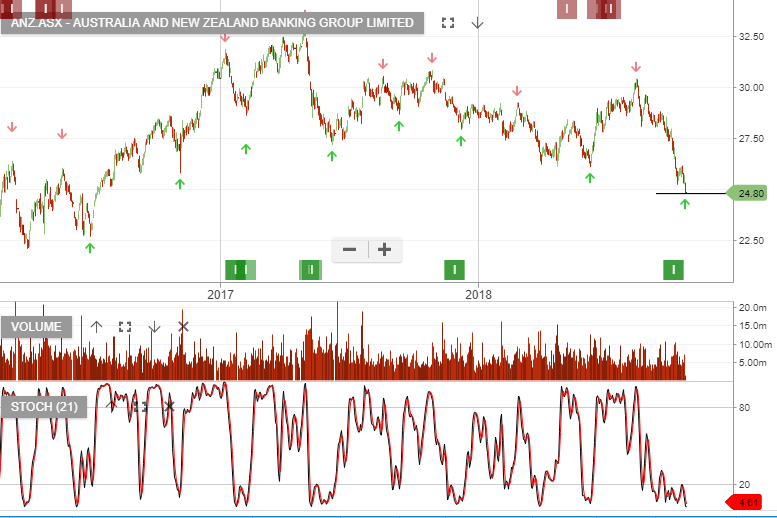

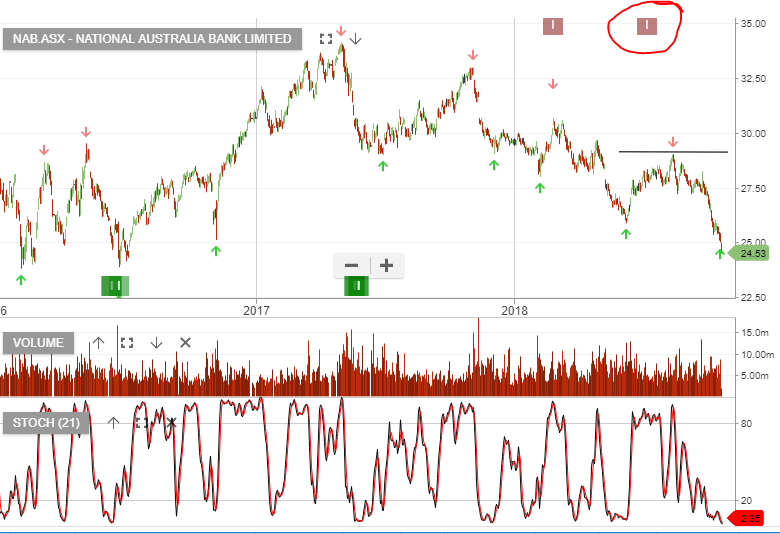

ANZ, NAB & Bank ETF Continue To Probe Lower

ANZ is expected to report its FY18 result on 31 October.

The share price has now broken the June low support area and looks vulnerable to more downside pressure.

NAB is scheduled to report its FY18 result on the 1st of November. The next downside target is near the $24.00 area.

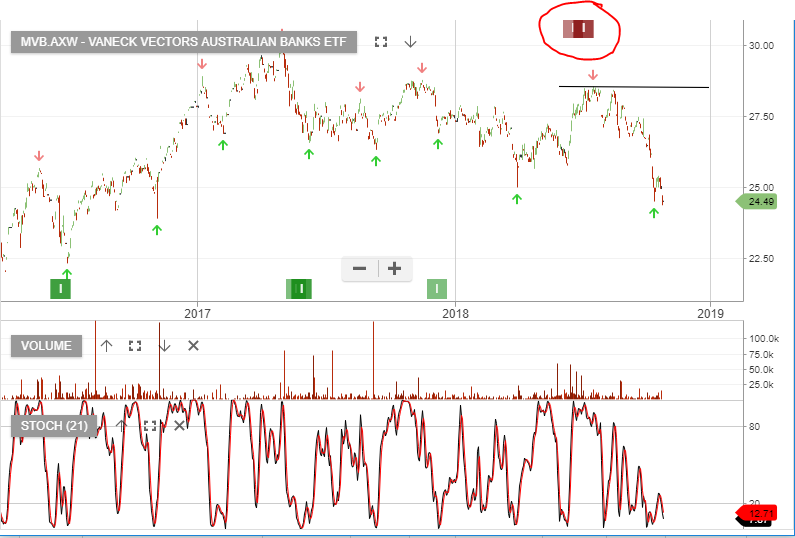

Vaneck Vestors Australian Bank ETF has been under ALGO Engine sell conditions since early July. The sell-off so far represents a 20% correction.