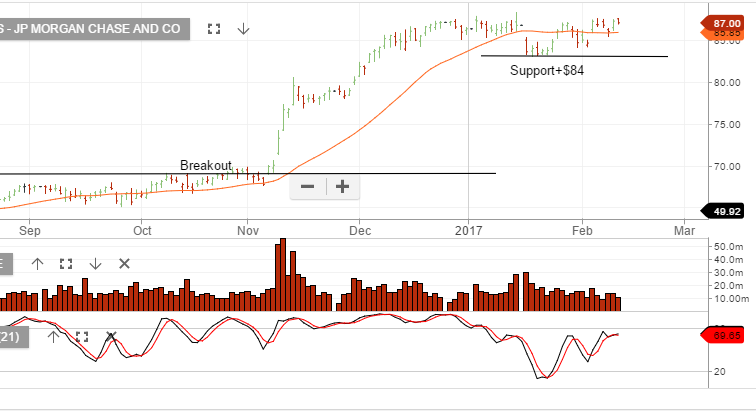

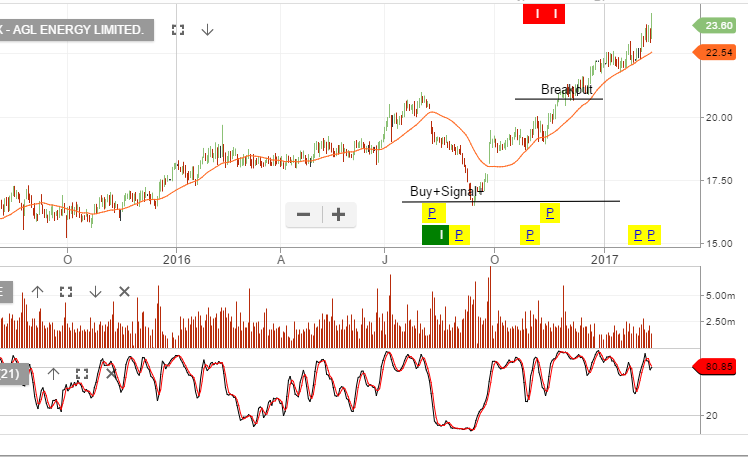

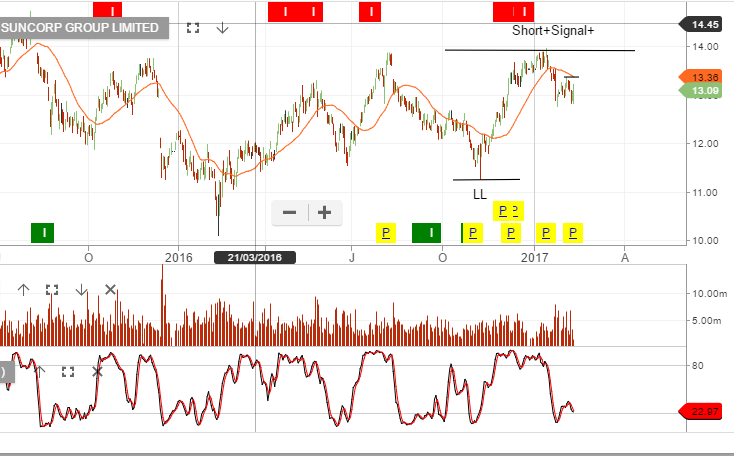

Chart Update – Banks

Goldman Sachs and JP Morgan remain within the consolidation range which began in early December.

In our local market we’ve seen BOQ & BEN sell off 10% from the January peak-to-trough. NAB reported weak revenue growth and higher than expected expenses, leading to a 1% fall in profit.

CBA report their half year results on Wednesday, we expect NPAT of $4.8b and DPS $2.00. 3 – 5% underlying EPS growth on the same time last year.

ANZ corrected 10% from peak-to-trough.

We’ll watch the US banks in the weeks ahead to see which way they break from their current consolidation range.