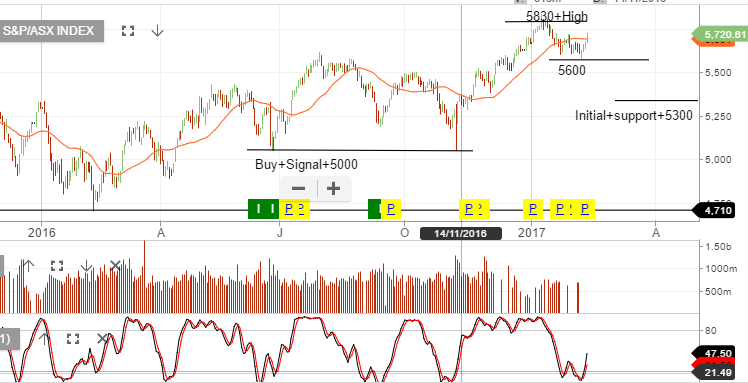

Since the the beginning of 2015, there have only been two periods of time when the SP 500 has corrected lower by over 10%.

The first was from August 18 to the 24th, 2015. During these 5 trading days, the SP 500 fell from 2103 to 1831, 272 points, or 13%.

The second time was from December 30th, 2015 to January 20th, 2016. During these 18 trading days, the SP 500 dropped from 2074 to 1804, 270 points, or 13%

Of the many complex components that make up equity market pricing, and the fundamental events which can trigger widespread selling of global equities, it’s worthwhile to note that both of these periods of extreme stock market pressure were preceded by credit stress in regional bonds markets: The Greek bond market in 2015 and the Chinese bond market in early 2016.

Over the last three weeks, there have been early signs that these two bond markets may be in trouble again.

On January 20th, Greek 2-yr bond yields were trading at 6%. Last week they traded over 10% as negotiations with the EU creditors and the IMF are showing familiar acrimony and lack of progress.

This 400 basis point increase in yield reflects growing scepticism that any refinancing agreements will be reached at the EU finance minister’s meeting on February 20th.

As a point of reference, Greek 2-yr bonds were yielding over 25% when the contagion fears unsettled the market in 2015.

In China, the 2-yr yields have traded 40 basis points higher since the beginning of the year to just over 3%.

But more importantly, trading volumes in China’s bond futures market have exploded over the last two months as investors look to hedge the growing risks of rising rates and potential defaults. Turnover in the 2-yr to 10-yr Chinese bond curve has quadrupled since October as bond prices have dropped.

In early 2016, stress in China’s bond market caused investors to dump the Chinese Yuan, which lost over 7.5% during the broad global equity market correction.

It’s not our base case that global equity markets are drawing close to a sharp correction lower.

However, we feel it’s important that investors are cognizant about the state of markets which have triggered such events in the past. In short, the time to make a plan for a market sell off is before it happens, not while it’s happening.

As such, Investor Signals can offer investors trading access to local and global bond markets, International stocks and credit markets, In addition to ASX equities and derivatives.