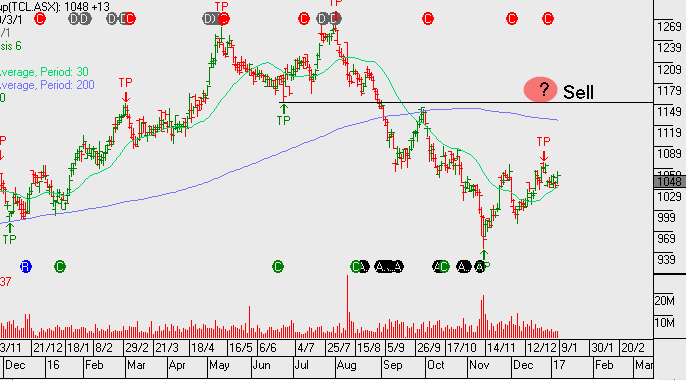

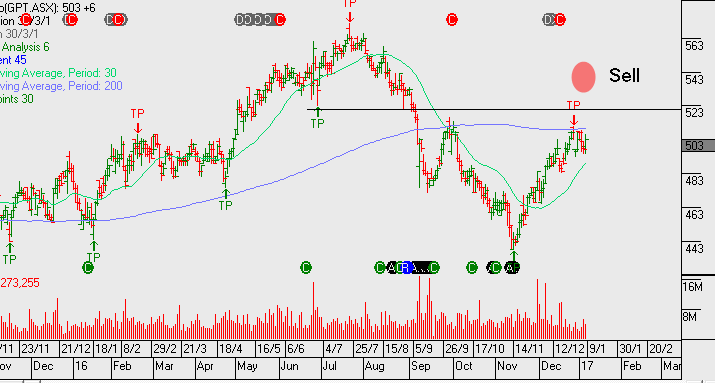

Australian Bank Profit Announcements – Key Dates

Bank profit announcements start in February with the following key dates worth noting.

SUN 9 February, BEN 13 February, CBA 15 February along with 1Q17 trading updates from ANZ and NAB in February.

Following the recent rally in bank shares, we see the current trading range as full value, therefore, placing the banks at risk of being buffeted by any increase in market volatility. Although net interest margins have improved, the prospects of earnings growth is modest with the outlook between 1% – 4% growth at both top and bottom-line.

We also remain concerned that the cycle for bad debts is likely to rise from the current historic low levels.