CIMIC Takeover Offer for UGL

CIMIC (CIM.ASX) announced it intends to make a takeover offer for UGL at $3.15 per share. This is almost a 50% premium to UGL’s last traded price and values the business at $520m.

Pre UGL, FY17 EPS growth in CIM is forecast to increase by 5% to approximately $1.90, assuming they payout around $1.10 in dividends, it places the stock on a forward yield of 4%, (100% franking credit).

It’s worth adding CIM.ASX to your watch list as the UGL acquisition will help strengthen the investment case.

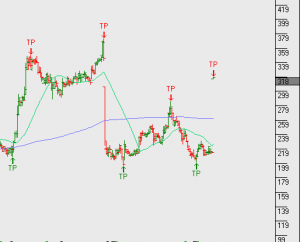

CIM.ASX

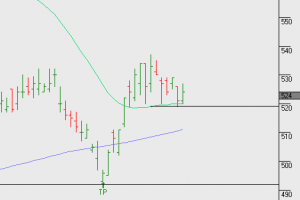

UGL.ASX