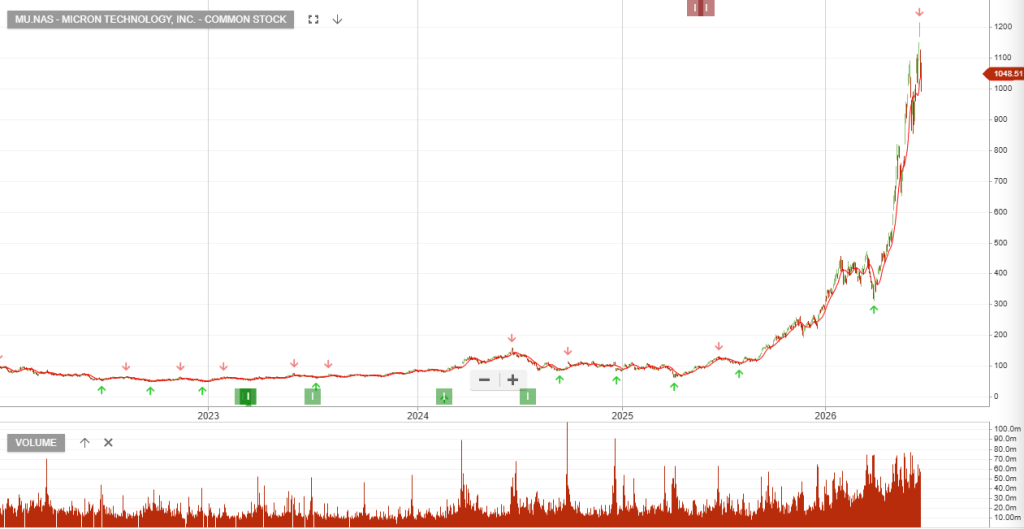

Micron

Micron’s gross margin, the profit left after accounting for the cost of goods sold, jumped to 84.9% in the third quarter from 74.9% in the prior period and 39% a year earlier. Margins topped analyst estimates.

Net income during the quarter was $28.24 billion, or $24.46 per share, versus $1.89 billion, or $1.68 per share in the year-ago period.

While all four of Micron’s business units saw revenue multiply, the most explosive growth was in the core data center business, where sales climbed more than sevenfold to $11.5 billion from $1.53 billion in the same period a year ago. In addition to memory, Micron also recorded over $5 billion in data center solid state drive revenue, the company said in a presentation.

Cloud memory was up over 300% to $13.77 billion.

The company’s mobile and client business unit saw a 250% growth in revenue to $11.52 billion, and even memory for automotive and embedded applications more than quadrupled to $4.63 billion in sales.