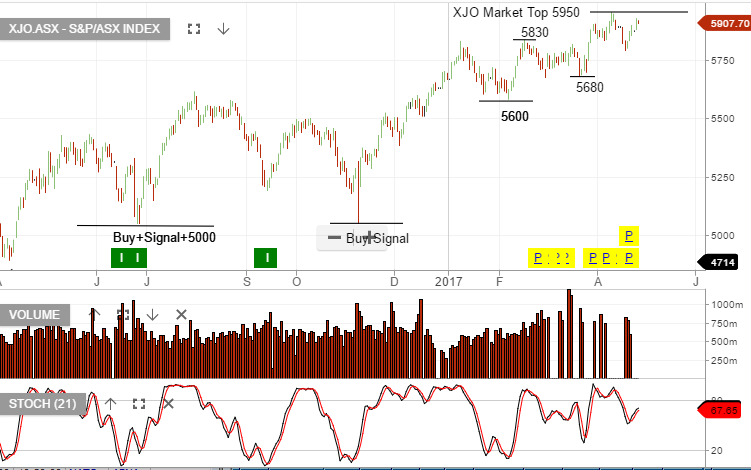

XJO – Chart Update

The XJO made a low on the 19th of April at 5790 and has since rallied to within 40 points of the trend high that began in Feb 2016.

The XJO made a low on the 19th of April at 5790 and has since rallied to within 40 points of the trend high that began in Feb 2016.

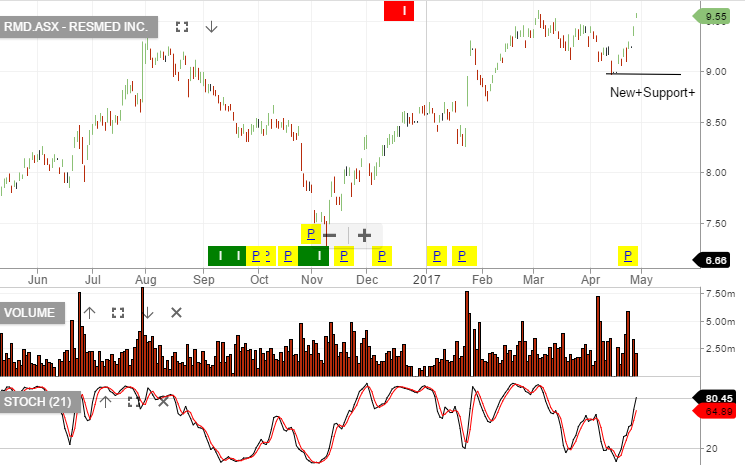

We hold CSL, RMD, RHC & SHL in our model portfolio. Over the next 10 years these remain a “buy on the dip” story and the Algo Engine will alert us to the next higher low formation for a discounted entry point into the stocks.

RMD reports tonight in US and we’re looking 15% EPS growth.

Inflation in Australia remains flat, and below the lower end of the 2% to 3% RBA target band.

Many analysts were expecting an uptick in the CPI inflation reading to 2.3%, which could prompt the RBA to shift its neutral-bias to a tighter posture.

As a result, the AUD/USD fell to a 3-month low of .7455 overnight. With the RBA meeting next week, any mention of a more benign inflation outlook would put more downside pressure on the Aussie.

Internal price indicators now point the the next support level at .7420 and a more significant target of .7365 over the near-term.

Over the last few weeks, we have been suggesting that investors look to buy the BetaShares YANK ETF to profit from a falling AUD/USD.

The YANK is an inverse ETF, with a 2.5% weighting. This means that YANK will gain 2.5% for every 1% drop in the AUD/USD.

IBM has approximately US$3.8 billion remaining on its current share buy-back plan. Over the last two years, the company has averaged about $4 billion per year in share repurchases .

IBM annual yield is now running at around 3.70% or equivalent to US$6.00, that’s well above US Treasuries.

Our Algo Engine generated a buy signal at around $155 back in September last year. Since then, the stock rallied to $183 before last week’s disappointing earnings result caused the stock to sell-off. The price structure looks like we may see a retest of the $150 support level in the near -term.

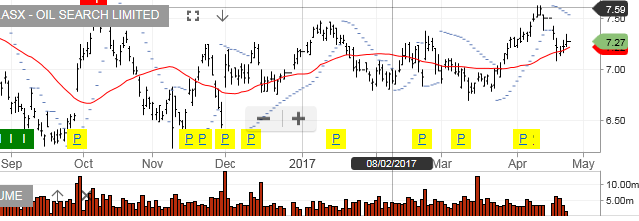

After falling over 7% last week, WTI Crude Oil dropped another 1% last night to trade at a four-week low of $49.05.

Concerns of oversupply in both Crude and Gasoline are dragging prices down as both products are now trading below their 30 and 50-day moving averages.

This weakness in both the technical and fundamental indicators will likely put downside pressure on the shares of Oil Search.

On April 19th, Oil Search announced a quarterly report which showed a 2% decline in total production for the March quarter, along with a 1% decline in total sales revenue.

Based on these data sets, we would expect OSH shares to trade back down to the initial support at $6.70 in the near term.

Oil Search

The benign result of the first round of the French elections has triggered a “risk on” relief rally in global financial markets.

As such, Gold opened the Asian session down $20.00 at $1265.00 and has steadily recovered as the reality of the election result settles into the market.

Technically, Gold is still in an uptrend with the 30-day moving average still below the market at $1256.00. We expect Gold to recover and re-test the April 17th high of $1295.00 in the near-term.

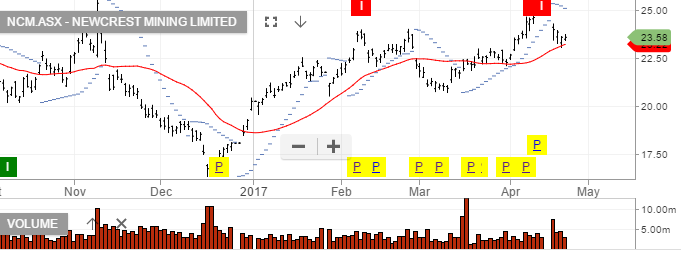

Over the last five trading days, shares of NCM have dropped close to $2.00.

The lower price of Gold combined with the closure of the Cadia mine has pushed the stock down into the buy zone of $23.20; still above the 30-day moving average at $23.00.

We expect both the price of Gold and shares of NCM to rebound and trade higher over the medium-term. Investors looking to profit from higher Gold prices can also look at the QAU BetaShares Gold ETF.

RMD will report their 3QFY17 results on 27th April. Early success of the AirFit 20 series should help to underpin year-on-year underlying earnings growth 15%+ to $US$520m.

FY18 we expect revenue of US$2.3b, EBIT US$580m, (from US$520in FY17), EPS US$3.10 and DPS US$1.45, placing the stock on a forward yeild of 2.1%

We like RMD’s growth outlook and therefore we’re encouraged to buy RMD ahead of the result and to add to the position on price retracements.

To help enhance the yield, we’re selling out-of-money call options, allowing for reasonable capital growth whilst at the same time increasing the cash flow from the dividend and call option income to over 10% p/a.

On 2nd May, ANZ will report their half-year earnings. The market is expecting a net profit of around $3.7b and DPS for the half year of $0.80.

4th May, NAB will report their half-year earnings. Net profit should be around $3.4b and DPS of $1.00.

5th May, Macquarie Bank reports. Net profit is expected to be similar to last year at $2.15b and DPS of $2.52

8th May, WBC report their half-year result. Net profit should be $4b and DPS $0.95

On average, the market is looking for approximately 3% underlying EPS growth among the banks and dividends to remain steady, or the same as the previous 12 months.

CCL downgraded its outlook for 1H17 due to weakness in the Australian beverage performance.

CCL expects underlying NPAT will decline in 1H17 and expects FY17 NPAT to be in line with FY16 at around $420m

If we assume no earnings growth into FY18 and a continuation of the $0.45 cent per year dividend, it places the stock on a forward yield of 4.6%.

FY18 revenue $5.2b, EBIT $680m & EPS $0.54.

The XJO is now in the early stages of a new minor low structure.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453