Transurban Group 1Q17 Traffic Growth

Overall the traffic results for TCL.ASX were in line with expectation. New projects over the next 2 – 3 years help to underpin the valuation, along with the rising dividend.

We expect to see the traffic growth rate steadying, which then requires a favourable back drop in bonds, i.e slow gradual interest rate rises in the US, to allow TCL to track sideways.

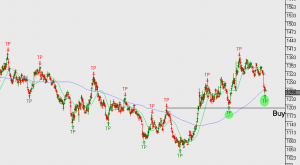

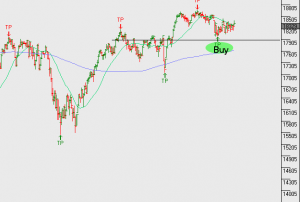

We’ve been buyers on the recent dip and we see TCL as a sell back above $11.75. For portfolio investors it will pay to cover TCL with an $11.75 call into next year with a view towards collecting the $0.25 December dividend plus the call premium.

Fy17 revenue of$2.2b, on EBITDA of $1.65b, DPS $0.50 places the stock on a forward yield of 4.7%. Fy18 DPS should increase by a further $0.05 to $0.55 per share.

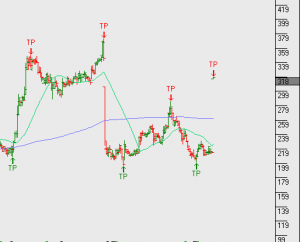

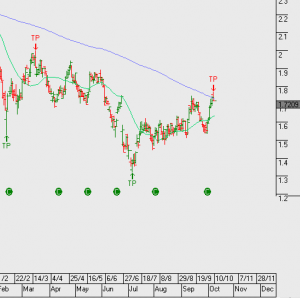

TCL.ASX