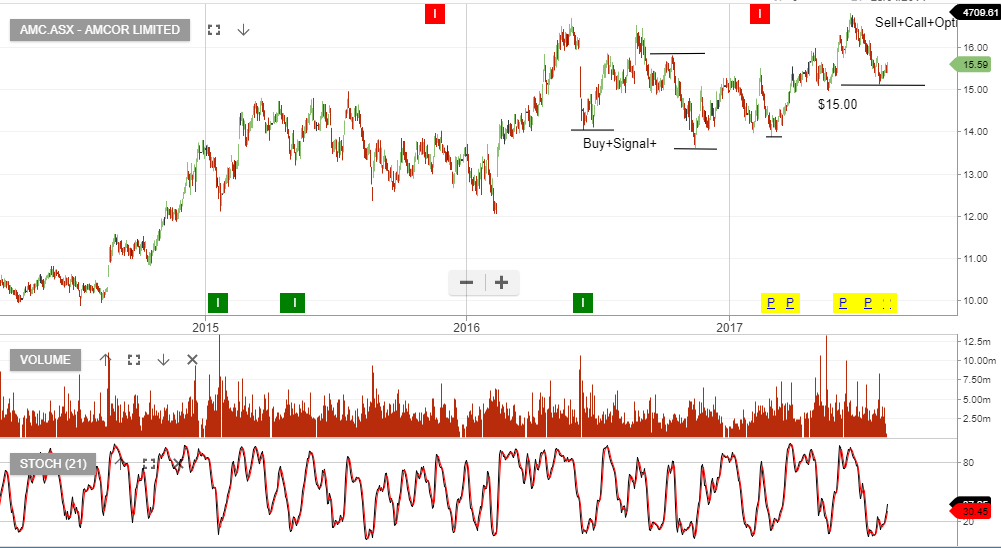

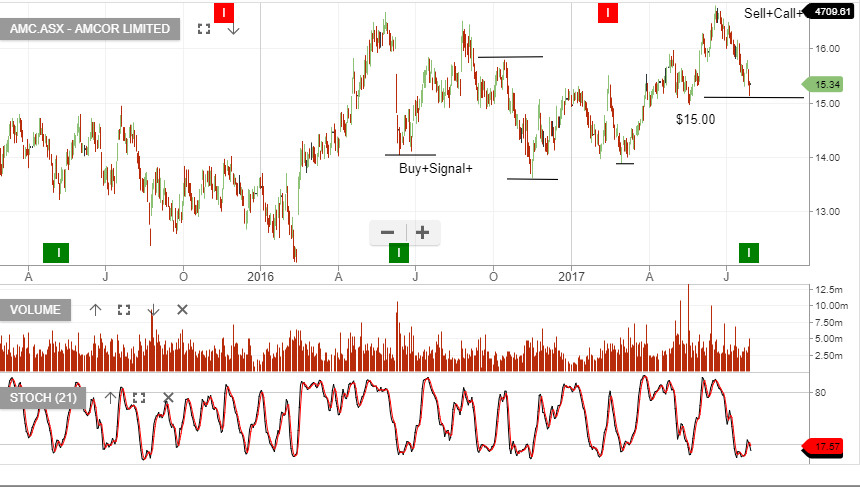

Amcor – Looking to Acquire Guala Closures Group

Amcor has been shortlisted to acquire the global leader in closures. Amcor identified closures as a new strategic segment at its investor sessions in June 2017.

If regulators approve the deal, Amcor may look to issue new equity.

We continue to view Amcor as a core holding and advise selling call options to enhance the return.

AMC trades on a forward yield of 4%.