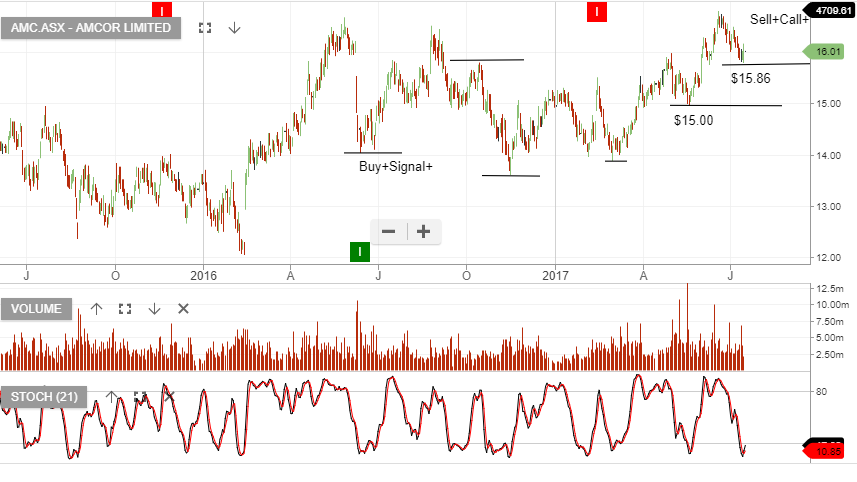

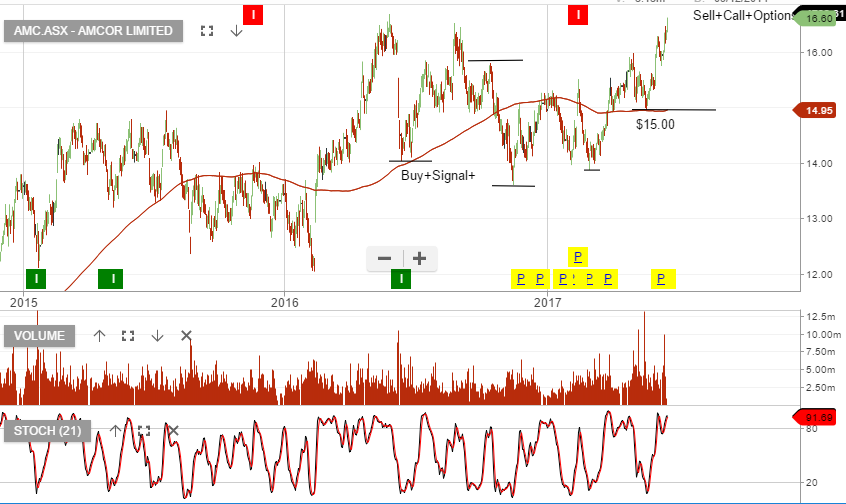

Amcor is trading on a high multiple of 19x forward earnings and a 3.8% dividend yield. However, the earnings are relatively defensive and we’re expecting 8% underlying EPS growth.

The stock should find support at or near $16 and is an appropriate consideration as a buy-write for client portfolios.

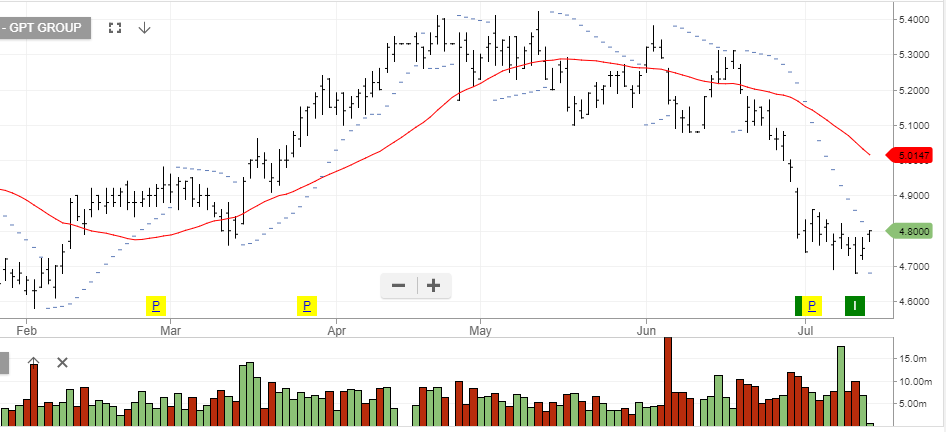

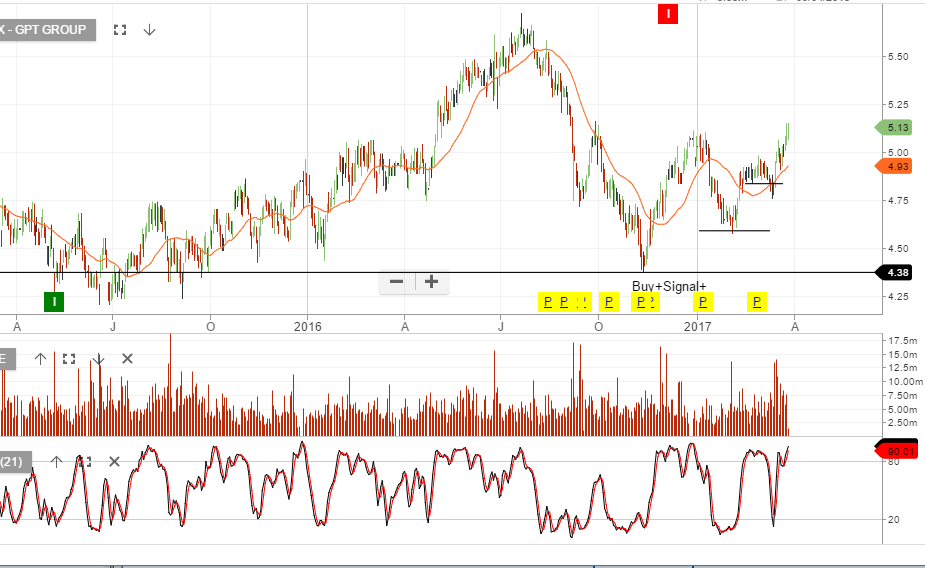

Over the last two weeks, yield sensitive names like SYD, TCL and GPT have all dropped over 10% from recent highs.

One of the main drivers has been the change in interest rate expectations from G-7 central bankers and the subsequent rise in short-term paper.

Moving forward, we see more likelihood of G-7 rates reverting lower within the year’s range and providing upside potential in the stocks above.

Other stocks we like on the basis of lower local rates are: AMC, WOW and MPL.

We see reasonable upside potential in the names and will employ the derivative overlay strategy (selling covered calls) to enhance the portfolios returns.

Amcor has remained one of our preferred portfolio holdings. We see 8% EPS growth over the next 12 months and the stock trades on a forward yield of 3.8%.

The current price is beginning to approach full value and we recommend selling the $17 call options into December to enhance the return.

Recent price action in the local ASX market suggests we’ve entered a period of heightened volatility and potential for downside risk. Since posting the high for-the-year at 5945.00, the index for Australian shares has dropped almost 4%.

Looking across the spectrum of ASX top 100 stocks, we have found several names which can offer defensive value in a broadly sideways to lower share market.

These include: IPL, MPL, WOW, CTX, QBE, SHL, SYD, TCL, AMC, and IAG.

We consider these stocks to have the potential for moderate capital growth and, combined with a buy/write strategy, will offer 10 to 12% cash flow on an annualized basis.

We continue to see Amcor as a solid contributor to portfolio returns, especially when complimented with a slightly out-of-the-money call option into November or December.

A combination of the dividend and call option premium produces 10 – 12% annualised cash-flow.

FY18 forecast revenue US$9.6b, EBITDA US$1.5b, Net Profit US$790m, EPS US$0.66 and DPS US$0.49 places the stock on a forward yield of 4%.

Following the sell-off in both AMC and BXB , we now are looking for buying support at or near the current levels. Our short-term momentum indicators have not yet turned positive but we’re likely getting close to valuation support, where increased buying will occur.

SCG and WFD went ex-dividend yesterday at $0.105 and $0.125, respectively. With both names we’ve added tight covered calls to boost the cash flow to 10 – 12% on an annualised basis.

Ansell is a relatively new addition to portfolios and yesterday’s earnings result was slightly disappointing. Again, we’ve been aggressive with the covered calls so we’re not looking for too much on the upside with ANN and we collected between $0.80 to $1.20 for the covered calls. We will look to exit on a rally back towards $23 by April/May.

Amcor reported a terrific earnings result with underlying growth running ahead of market expectations at 5%. This could accelerate up to 8 – 10% in the second half. This supports our $15.50 price target.

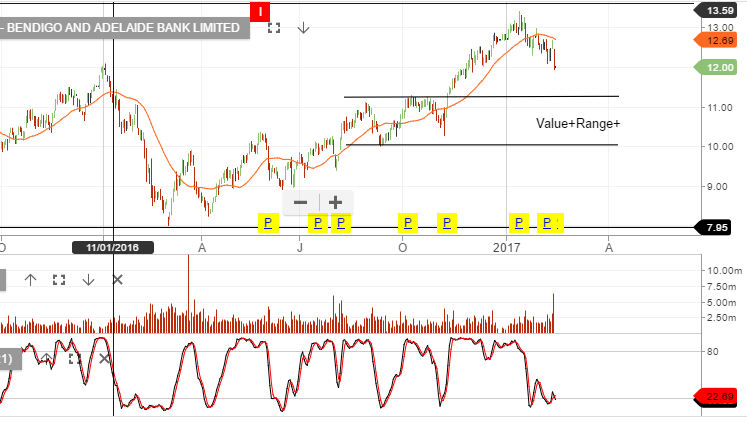

CBA’s earnings result tomorrow will be key for the banks. Thus far NAB and BEN have failed to deliver growth on the revenue and profit lines. We shorted BEN from $13.00 and we’ve been aggressive with selling call options over the top 4 banking names.

AZJ reported earnings in-line with market expectations. We remain cautious of the group’s high payout ratio with almost 100% of earnings being paid in dividends. This looks unsustainable in the medium term.

Tomorrow we will be focused on the earnings results for BLD, CBA, CPU, CSL, SHL and WES.

Shares of AMCOR are trading over 4% higher, to one-month high of $15.22, as the company reported a 3.8% rise in underlying net profit to USD 308 million.

The street had been expecting an underlying profit of USD 290 million.

Revenue rose 1.8% to USD 4.5 billion. AMCOR declared an interim dividend of USD 19.5 cents per share, compared to a USD 19 cent dividend during the same period last year.

AMCOR shares are up over 11% since trading as low as 13.65 in mid-November. Technical resistance will now be found in the $15.50 area.

We’re allocating funds to defensive names with moderate earnings growth. By adding tight covered call options we’re boosting the cash flow and generating our return on investment (ROI) through a lower risk, lower volatility investment process.

We’re holding small levels of hedging through inverse ETF’s and are mindful of the increasing number of stocks within the ASX 100 and the US S&P100 that are showing fading momentum. High valuations in many names combined with relatively low revenue and profit growth is likely to weigh on share price performance.

The following names we’re currently buying. AMC, CTX, SYD, TCL & TLS