Lend Lease Is Nearing The Buy Zone

Our ALGO engine triggered a buy signal for LLC last Friday at $18.70.

We mentioned in our commentary that investor support should emerge near the $18.00 support level; the low for today has been $18.02

From a technical perspective, internal momentum indicators have reached an extremely oversold level and a price reversion higher looks likely from here.

We see the first level on upside resistance near the October 2nd high of $19.60.

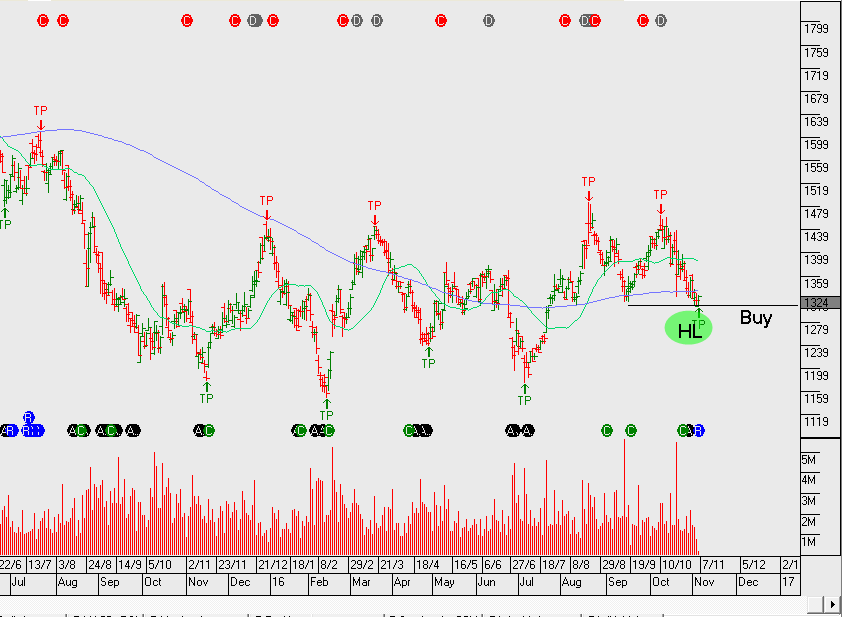

Lend Lease

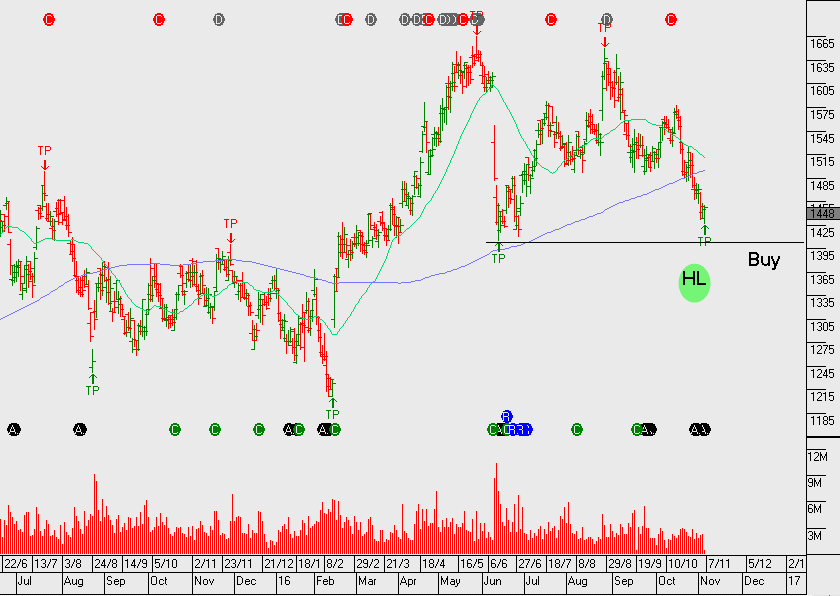

Lend Lease

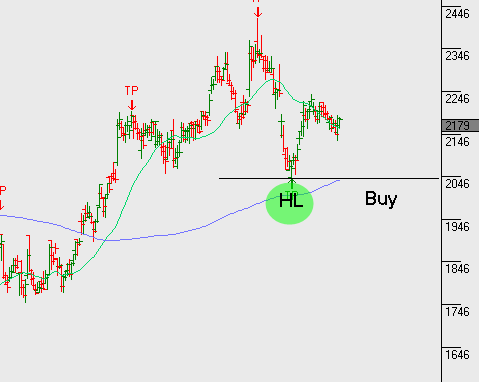

Lend Lease

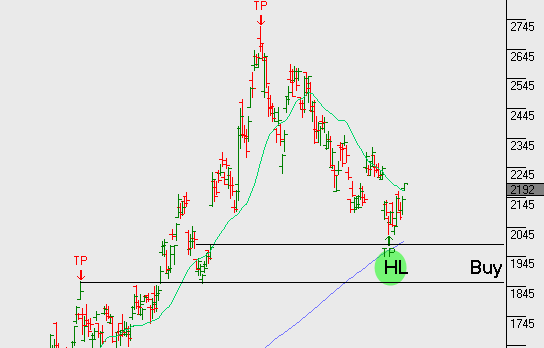

Lend Lease

Lend Lease