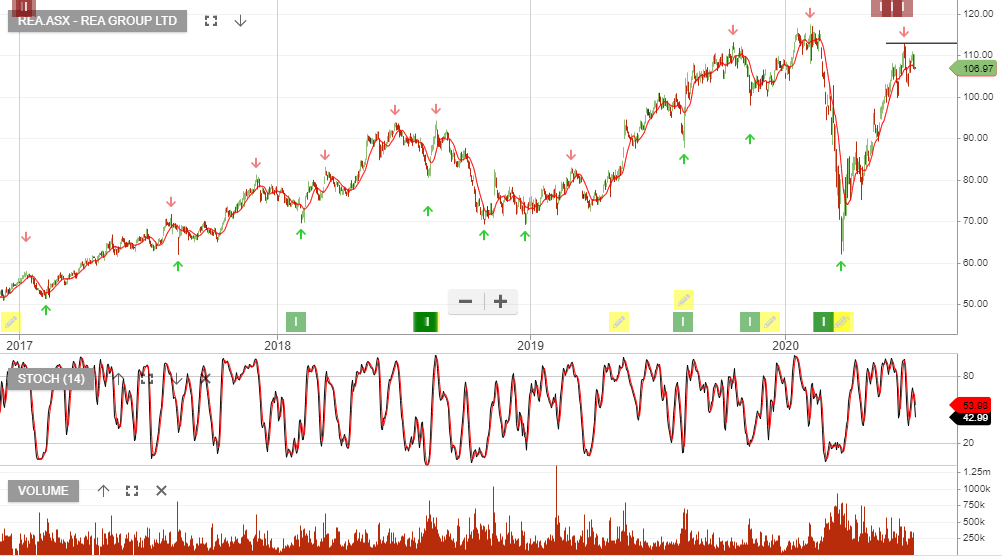

REA – Profit Taking

REA Group is under Algo Engine sell conditions. We expect selling pressure to increase at $109.

REA Group is under Algo Engine sell conditions. We expect selling pressure to increase at $109.

REA Group is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

The share price has corrected over 40% due to the impact of COVID-19. Earnings will decline over the coming months as restrictions impacting open homes and slower vendor listings bite in the short-term.

In the medium term, we see scope for a full recovery in the business and therefore, the current share price at 20x forward earnings looks attractive.

REA Group is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

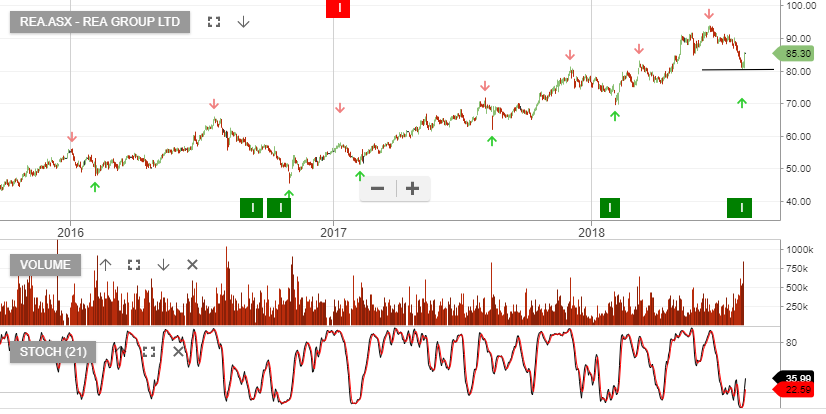

Add REA to your watchlist and look for support to develop within the $65 – $75 price range.

REA Group is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

We see buying support increasing at the $103 level.

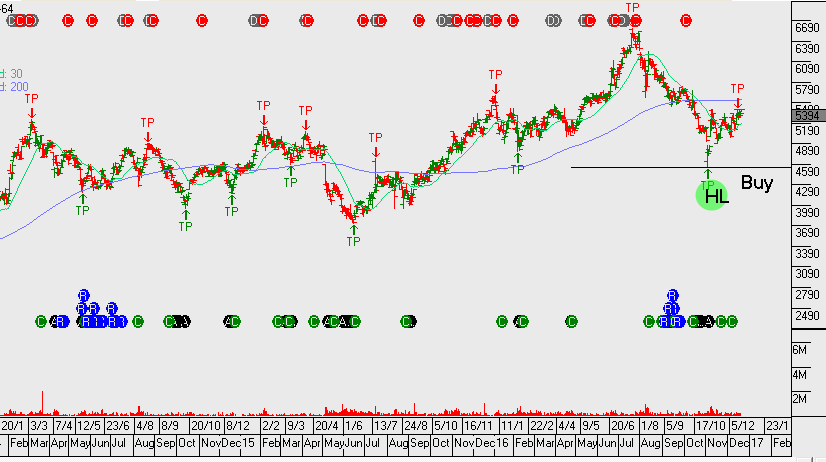

REA Group rallied 5.5% on Friday following a better than expected earnings result. Our Algo Engine triggered a buy signal Thursday after 3.30pm going into the market close.

The chart below shows the entry signal, along with the $87 support level where buying interest began to accelerate.

REA Group is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

REA Group announced that its results for the nine months ended 31 March 2019. Reported 3Q revenues up 7% and EBITDA up 6%. The result highlights the quality of the REA business, with solid growth despite a very challenging macro environment.

If we assume FY20 revenue of $990mn, EBIT $520mn and DPS of $1.50, it places REA on a forward yield of 1.8%.

Underlying earnings growth in FY20 is forecast to be up 12%.

Our Algo Engine generated a buy signal in REA last week at $80.50.

Since then the stock has rallied almost $5.00, following a solid FY18 earnings result which met consensus forecasts.

Revenues were reported at $808m, EBITDA $464m and NPAT from core operations $280m.

In FY19, the market is looking for 15% revenue growth, flowing through to similar underlying earnings growth. This places REA on an FY19 forecast yield of 1.8%.

Despite, risks in soft listings and developer pipeline, we recommend maintaining long exposure to REA and applying a stop-loss below the recent $80.50 low.

REA

REA Group has announced the sale of its European assets to Oakley Capital Private Equity for $190m. Profit on the sale is expected to be around $170m. REA Group should see earnings pickup into 2017 & 2018 with FY18 revenue likely to grow by 10% to $850m and EBIT by 15%+ to $420m.

FY17 DPS $0.90 and FY18 DPS $1.10, places the stock on a forward yield of 2.1%.

REA payout 50% of earnings and the dividend is fully franked. The recent algo buy signal at $46 provided a solid entry point. We recommend applying a stop-loss on a break below the November low of $45.50

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453