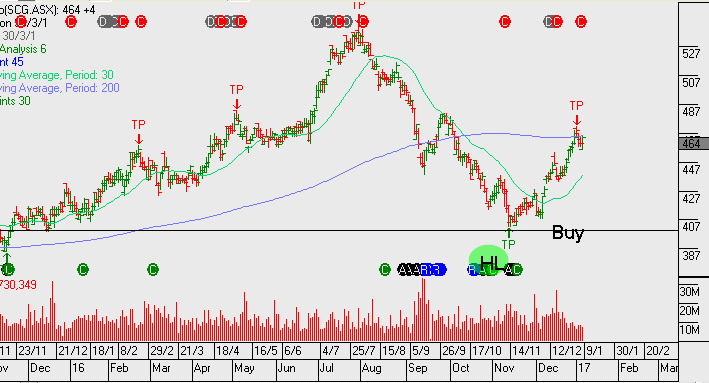

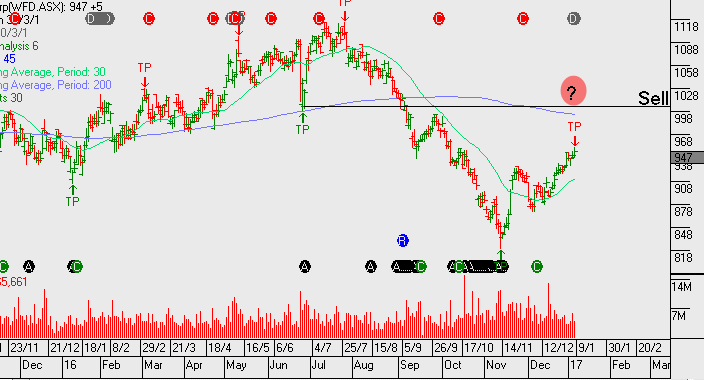

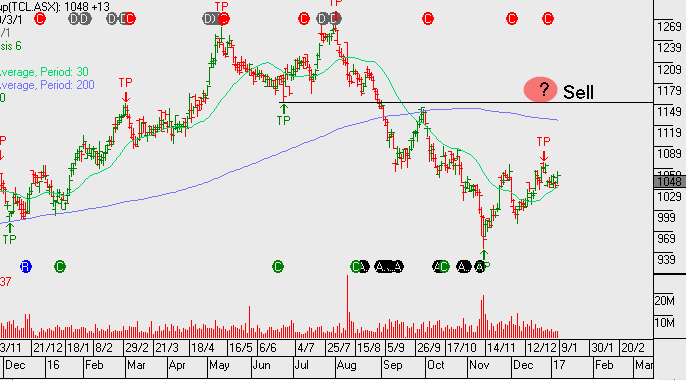

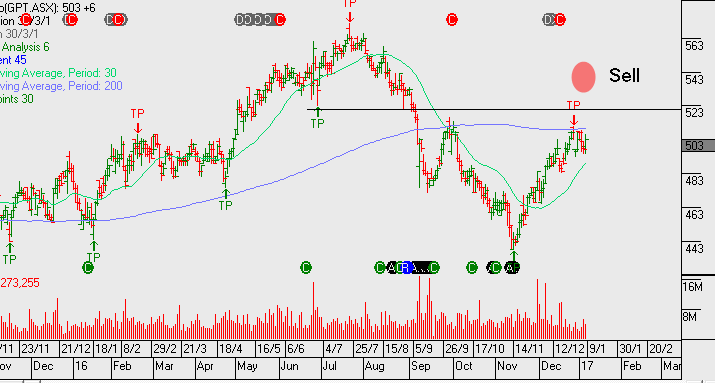

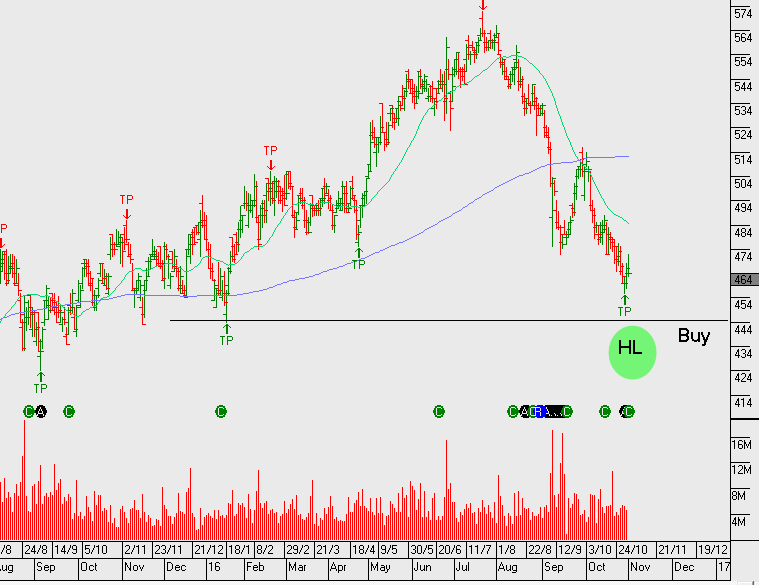

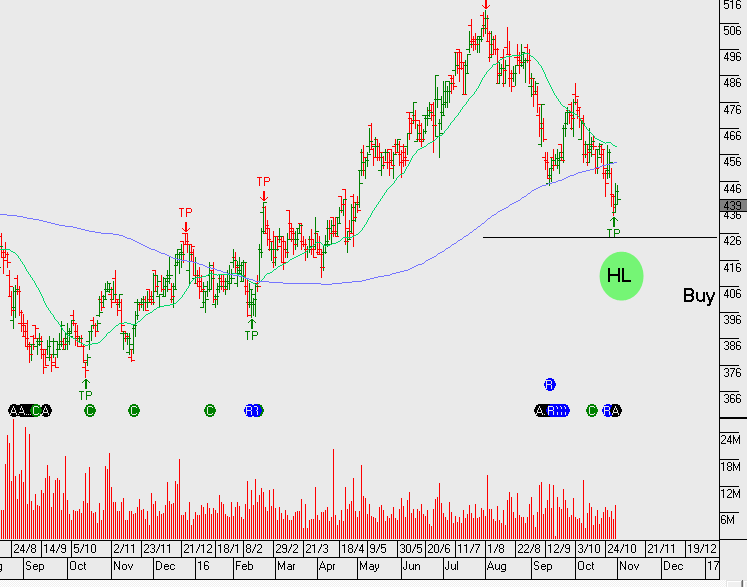

AMC, CTX, SYD, TCL & TLS

We’re allocating funds to defensive names with moderate earnings growth. By adding tight covered call options we’re boosting the cash flow and generating our return on investment (ROI) through a lower risk, lower volatility investment process.

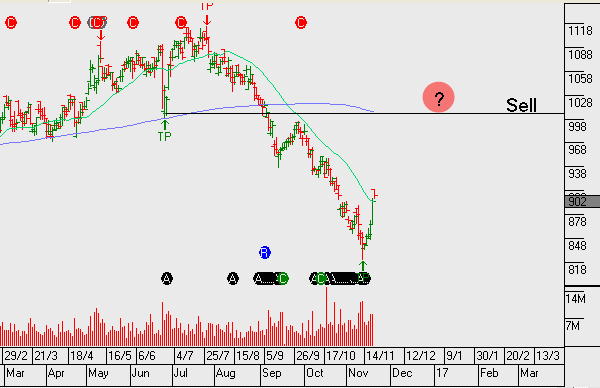

We’re holding small levels of hedging through inverse ETF’s and are mindful of the increasing number of stocks within the ASX 100 and the US S&P100 that are showing fading momentum. High valuations in many names combined with relatively low revenue and profit growth is likely to weigh on share price performance.

The following names we’re currently buying. AMC, CTX, SYD, TCL & TLS