While NVE is a niche semiconductor player rather than a massive chipmaker, it fits into the broader AI infrastructure landscape via:

Next-Gen Memory (MRAM): As AI workloads and edge computing demand faster, more energy-efficient non-volatile memory, MRAM technology is highly regarded for its low power consumption and high endurance.

High-Speed Data Isolation: Their spintronic couplers handle high-speed data transmission with high noise immunity, which is crucial in rugged Industrial IoT (IIoT) applications and server power supplies.

Full-Year FY 2026 Guidance: The company has reaffirmed full-year revenue guidance of $12.0 billion to $13.0 billion (with consensus currently sitting at $12.6 billion). This represents an incredible ~146% year-over-year growth rate compared to FY 2025 revenue of $5.13 billion.

Management secured over $20 billion of financing this year, with no material debt maturities before 2029 despite elevated leverage.

Ten customers have committed at least $1 billion each, while the financial services backlog alone has approached $10 billion.

The stock now trades near 3.5x FY2026 revenue despite consensus expecting revenue to nearly double to $25 billion next year.

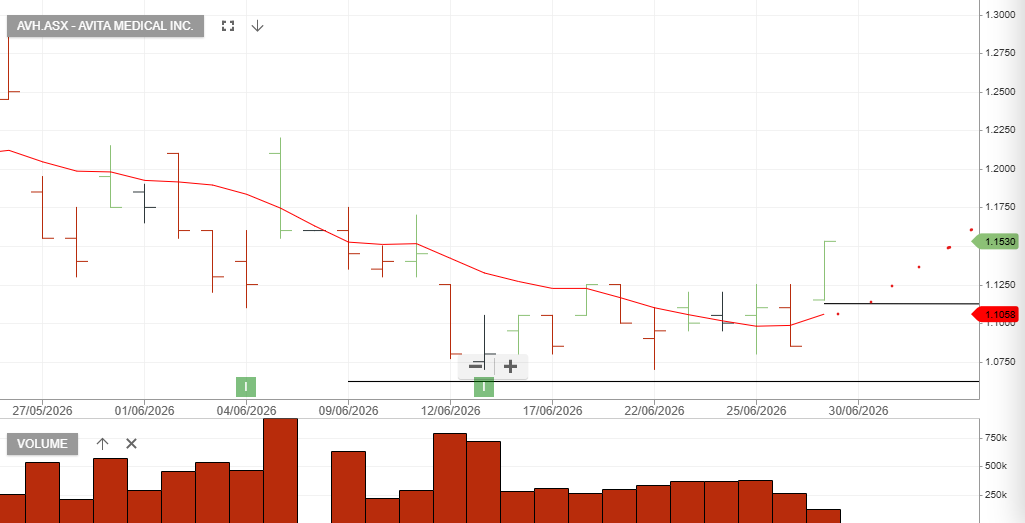

Avita Medical is a commercial-stage regenerative medicine company focused on acute wound care and therapeutic skin restoration.

Market Capitalization: ~AUD $170.81M – $174.95M

Earnings Per Share (EPS): -AUD $0.452 (unprofitable)

Performance (2026 YTD):+3.33% (though down roughly 27% over the past 12 months as the company works to scale and reduce cash burn).

Revenue Growth: Q1 2026 revenue reached $19.3 million USD, a 4% year-over-year increase and a 10% sequential increase from Q4 2025, showing gradual recovery following reimbursement and distribution disruptions in late 2025.

Iluka Resources earnings forecasts reduced due to the slower ramp-up profile.

First Rare Earths Offtake Agreement Secured

Iluka announced a four-year take-or-pay offtake agreement covering approximately 1,200 tonnes of Nd, Pr, Dy and Tb from CY28 onward.

The contract represents about 10% of planned rare earth production and validates demand for Eneabba’s future output.

Production Ramp-Up Appears Slower Than Expected

Contracted volumes imply a more gradual production ramp-up than previously forecast.

Eneabba Refinery Funding and Construction De-Risked

Export Finance Australia confirmed access to the full A$1.65bn non-recourse government loan.

The refinery is over 50% complete, capital cost remains A$1.7–1.8bn, and commissioning is targeted for mid-2027.

The offtake agreement is a strategic positive that validates Eneabba’s rare earth project, but the market may need to temper expectations around the speed of production ramp-up. Macquarie remains constructive on the longer-term rare earths opportunity.

NAS: SMCI said it plans to raise $7 billion in equity-related sales to cover the costs of hardware component purchases. The company also said it’s received $39 billion in artificial intelligence server orders in recent weeks.

CSL appears to be approaching a profitability low point in FY26, with FY27 expected to mark a return to earnings growth. Management’s transformation initiatives, lower plasma collection costs, and the removal of excess immunoglobulin (Ig) inventory from the US market should support margin recovery and earnings improvement. While challenges remain from competitive pressures in Ig, albumin, KCentra and Vifor pricing, the company is positioned to deliver modest profit growth.

Key Bull Points

FY27 earnings recovery expected: FY26 is likely the trough year, with FY27 benefiting from easier comparisons, including the removal of ~$300m of excess Ig inventory and ~$300m in transformation savings.

Behring margins should improve: Lower plasma collection costs from nomogram collections are expected to drive a noticeable gross margin recovery, supported by around a 10% increase in plasma collected per donor at no extra cost.

Transformation programme provides meaningful support: CSL expects approximately $300m of gross cost savings in FY27, equivalent to roughly 8% of FY26 NPATA guidance, helping offset industry pricing pressures.

Impairments are largely irrelevant to cash flow: The estimated $5 billion impairment charge is non-cash, with the main benefit being lower future amortisation expenses, which could modestly support reported NPAT.

Valuation remains attractive: Despite lowering the price target to $158/share (from $175), the stock trades at a significant discount to the broader market multiple, offering potential upside as earnings recover in FY27.

Expected Revenue & Growth: Driven by accelerating AI data center and custom silicon demand, Marvell raised its growth guidance significantly during its last earnings call:

Q2 FY2027 Revenue Guidance: Guided to $2.7 billion (±5%).

Nvidia CEO Jensen Huang, speaking onstage at Computex in Taipei, called the chipmaker the “next trillion-dollar company,” highlighting Marvell’s critical role in high-speed data center connectivity.

Next Earnings Date: Expected Date: August 20, 2026 (to August 27, 2026)

Following stellar bookings and AI demand, Marvell’s management has significantly upgraded its near-term and long-term revenue projections:

Upcoming Quarter (Q2 FY2027) Guidance: Expected Revenue: $2.70 billion (with a range of +/- 5%). Growth Rate: Represents ~35% Year-over-Year (YoY) growth

Full-Year FY2027 Guidance: Expected Growth: Projected to grow ~40% YoY to nearly $11.5 billion (strongly upgraded from the previous 30% growth guidance).

FY2028 Guidance: Expected Revenue: Upgraded to $16.5 billion (up from its prior guidance of $15.0 billion).

Expected Profit (EPS) Growth: Profit margins and earnings per share are scaling upward alongside high-margin datacenter optical and custom ASIC programs: Upcoming Quarter (Q2 FY2027) Guidance: Growth Rate: Represents an estimated ~35.8% YoY growth compared to the prior-year period.

Key Growth Drivers

AI Interconnect Business: Expected to grow over 70% YoY in FY2027, driven by skyrocketing demand for optical PAM4 DSPs as data centers transition from 800G to 1.6T speeds.

Custom ASIC Silicon: Marvell holds custom silicon partnerships with all five major U.S. hyperscalers (e.g., Microsoft’s Maia chip, Amazon, Google TPUs). This custom compute segment is expected to more than double in FY2028 and is targeted to reach over $10 billion by FY2029.

Sophisticated Investor?

We have special opportunities available for Sophisticated Investors. If you're interested, and qualify, please provide your details below.