US Equity Markets

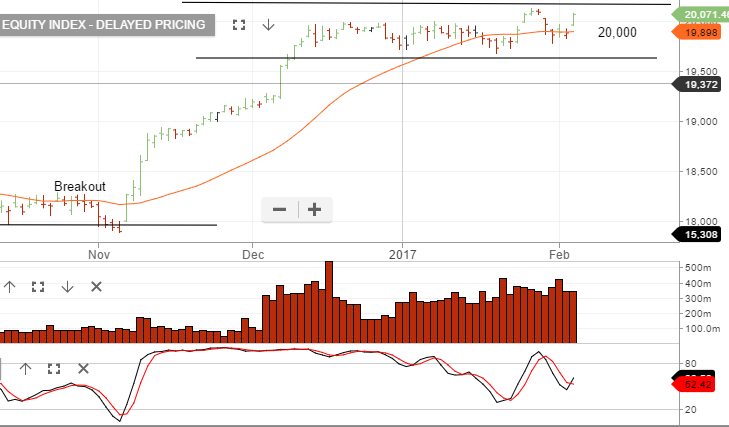

The DOW Jones 30 Index posted its 10th straight winning day in a row overnight. The fact that each one of those 10 winning days was a new record high has not been achieved since 1987.

This most recent leg higher in Dow started on November 8th, after the result of the US election. Since then, the DOW has gained 2,515 points, or 13.75%.

A widely held theme for the US equity rally has been the reflation of the US economy under a more business-friendly administration. This reflation theme was largely based on across the board tax cuts and a country-wide infrastructure construction plan.

The idea being that these new policy measures would stimulate growth and push inflation, interest rates and stock prices higher. Along these lines, the yield on the US 10-year note climbed over 83 basis points, or 6%, from mid-November to late December.

However, over the last several weeks, the US yields have stopped moving higher and the Treasury curve has stopped steepening. In fact, over the last 10 day rally in the DOW, yields on the 10-year notes have actually dropped from 2.48% to 2.37%.

In short, while the DOW has firmed to new highs over the last 10 sessions, the inflation part of the reflation trade is beginning to fade.

From a traditional value-metric point of view, if the recent move higher in US stocks were signalling a new leg higher in valuations, we would have expected the 10-year yields to have traded higher, not lower.