ASX – Algo Buy Signal

ASX is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

We see price support for ASX at $78.00

ASX is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

We see price support for ASX at $78.00

InvoCare is under Algo Engine buy conditions and the short-term indicators are now turning positive.

We see buying support building near $12.50

FY20 EPS growth should be 6%+ and we have the stock on a forward yield of 3.2%.

Treasury Wine Estates is under Algo Engine sell conditions and we highlight the recent softness in US sales data as a concern.

Sales within Asia continue to offset the US related weakness, however, we expect the TWE share price to remain under pressure.

Based on FY20 & FY21 EPS growth remaining in the 10 – 15% range, we have TWE EBIT growing from $660mn in FY19 to $850mn in FY21. This supports a forward yield of 3%.

We’re not holding TWE in our portfolio at present and we prepared today’s post on TWE as a reminder of the opportunity that lies ahead when the stock switches to buy conditions. We expect to see this in the first quarter of the New Year.

Downside target $15.50 – $16.50

REA Group is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

We see buying support increasing at the $103 level.

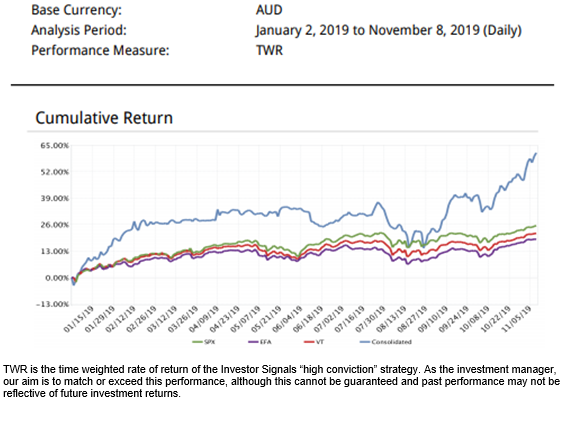

For our next Live Webinar, I will review high conviction ASX buy and sell opportunities from the recent algo engine and model portfolio signals. This webinar is exclusive to our members.

Learn the strategies and stock holdings that allowed us to generate 63% return in our new Interactive Brokers account model.

Boral is under Algo Engine sell conditions.

Boral disclosed that financial irregularities in its NAM Windows business will result in a US$20-30m EBITDA hit to its FY20 earnings. The announcement will weigh on Boral’s share price and we expect resistance to build at $5.00.

is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

The short-term momentum indicators have turned positive and we see buying support increasing within the $11.50 – $12.00 price range.

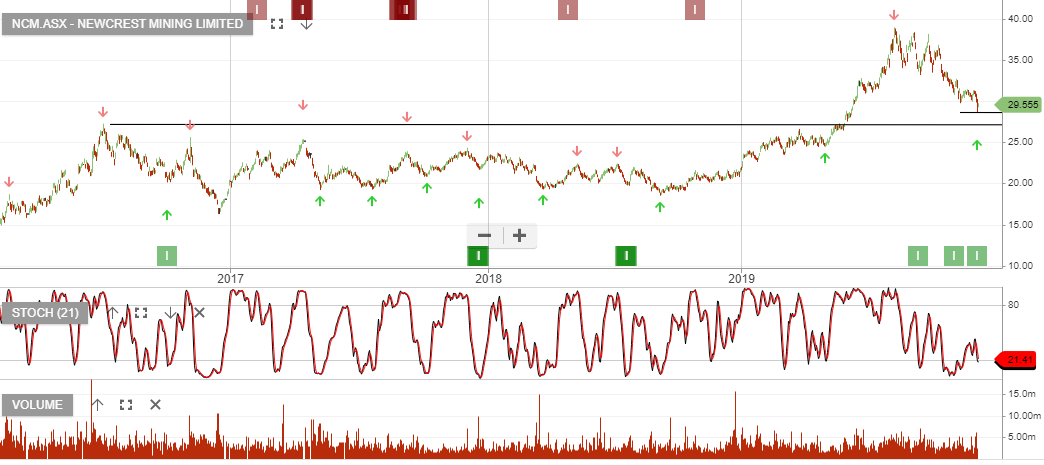

Newcrest Mining is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

We see buying support building at the current price level of around $29.50

Domino’s Pizza Enterprises is under Algo Engine sell conditions and is a current “high conviction” short.

A combination of underperforming international stores and an eroding position within technological leadership across fast food means we struggle with the 30x PE multiple and low 2.5% yield.

Within 2 – 5 years we forecast the business trades at 14x earnings and 4% yield, meaning the fair value is closer to $20, not the current price of $52.

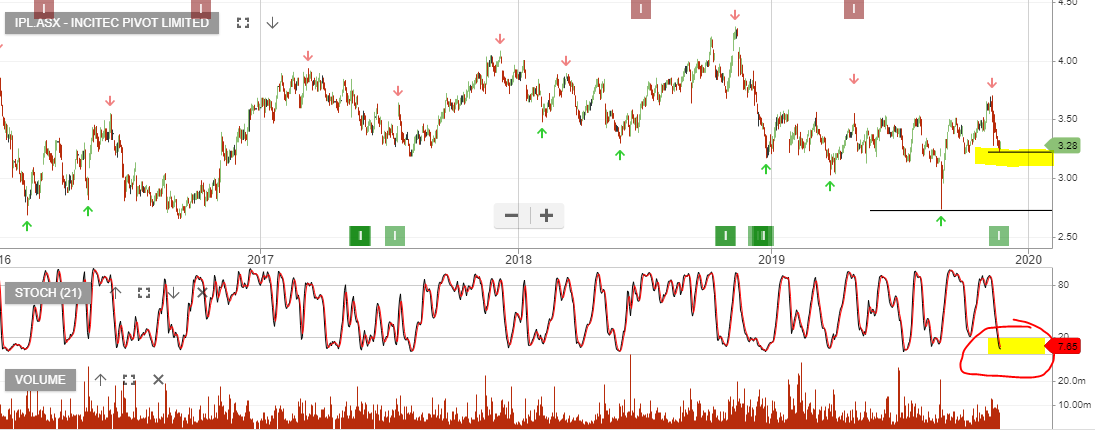

Incitec Pivot was triggered as an Algo Engine buy signal on Thursday 21st November. With an improving outlook for earnings in FY20 & 21 we’re willing to take a closer look at the upside potential.

The short-term technical indicators are about to turn positive and we’re likely to see buying interest pick-up near the $3.20 support level.

We’ll revisit this opportunity as the entry conditions playout next week.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453