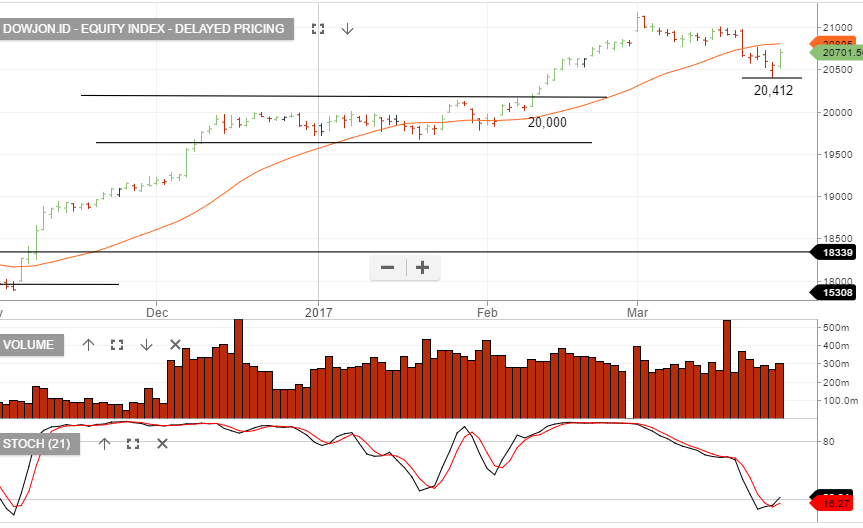

The Dow Jones has found short-term support in the higher low structure at 20,412. A break below this in the next day or two will be negative for US equities.

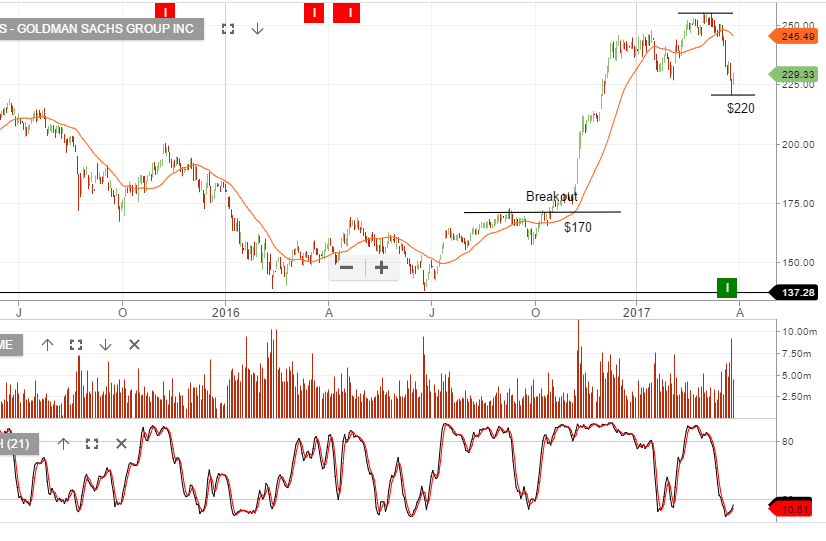

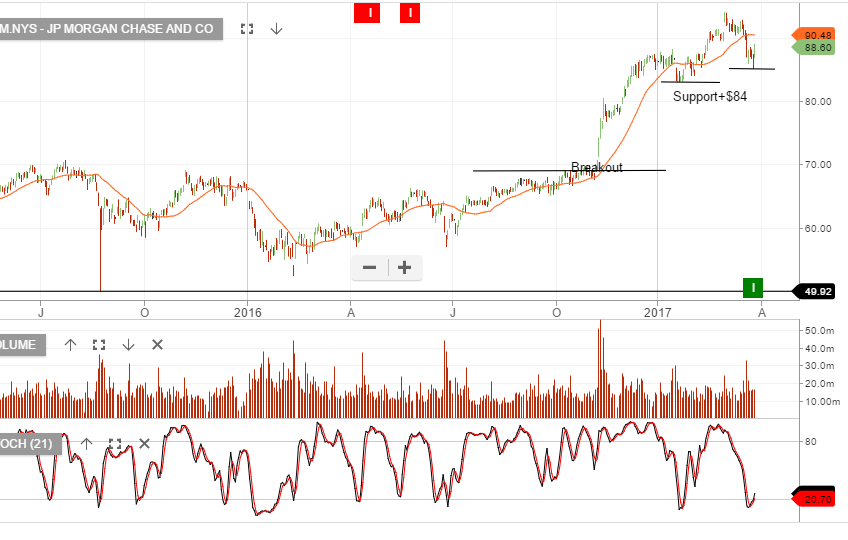

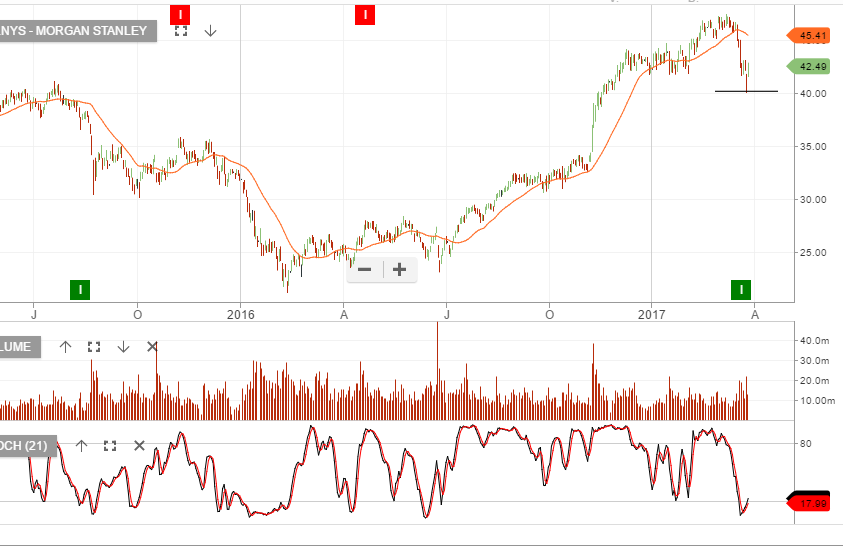

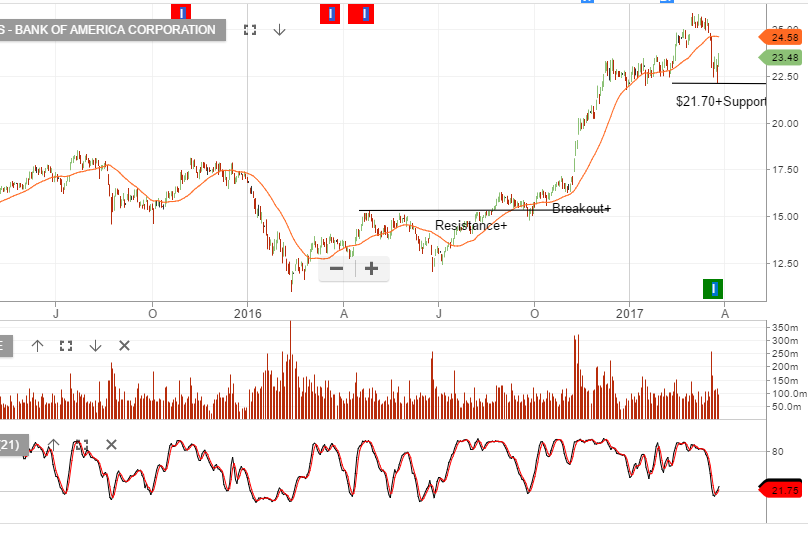

For the time being, we’re seeing buy signals from the Algo Engine in some of the beaten-down key US financials, Goldman Sachs, JP Morgan, Morgan Stanley & and Bank of America.

Chart – Dow JonesChart – Goldman SachsChart – JP MorganChart – Morgan StanleyChart – Bank of America

Our Algo Engine has triggered multiple buy signals across the major resource names, both in metals and in energy.

With the peak to trough sell-off among the sector extending between 13% – 20% it’s likely we find some value investors stepping back in to the market.

We’re comfortable with select exposure in BHP, RIO, S32, WPL, OSH, ORG but caution investors that stop-losses below the recent lows will be a prudent way of managing risks.

It seems unlikely that any buying interest from this level will carry the above names to new near-term highs. We’re of the view that a corrective bounce will top out at 5 – 7% above recent lows

We see the recent volatility in oil and iron ore, being primarily driven by US Dollar swings rather than related to any fundamental factors and remain cautious of negative news flow from China’s unsustainable debt problem within their shadow banking industry.

QAN has enjoyed strong share price performance since the release of its 1H17 results on 23 Feb 17. This has been partly supported by by the share buy-back program which at the current rates will end in the next week or two.

FY18 revenue is forecast to be $16b, EBIT flat at 1.6b, EPS $0.56 and DPS $0.26, placing the stock on a forward yield of 6%.

We’ll watch for the next Algo Engine buy signal on the structural higher low formation.

FY18 revenue to grow 5% to US$7b, EBIT +18% to US$2.2b, EPS US$3.60 & DPS US$1.70.

This places CSL on a forward yield of 1.8% into FY18.

We own CSL and recommend a covered call into the $130 range to enhance the yield.

Chart-CSL

Cochlear was recently triggered by the Algo Engine as a buy signal and we update our 12-month share price target to $138 based on a PE of ~27.5x. and a forward yield of 2%.

Risks remain associated with COH reimbursement changes, regulatory intervention and adverse currency movements. However, momentum favors the stock at present.

Over the past month, we’ve been long TCL and SYD , as we felt US interest rates would not push beyond levels already priced in by the market, therefore creating value in yield sensitive names.

Out of the potential basket of yield sensitive names to consider, our preference was TCL and SYD coming into their June dividends.

With the above stocks now trading up 15%+ and 10%+, (respectively), from their recent lows and the yields now compressing below 5%, we feel potential capital gains from here are limited and it’s time to sell covered calls to enhance the return.

With the recent sell-off in US equities, we’re now seeing a number of Algo long signals appear in the US financial names.

We’re mindful of the “peak optimism” that is priced in regarding tax cuts, deregulation & US economic pickup and approach these buy signals with caution.

We’ll be tracking the short term momentum indicators in Goldman Sachs and Bank of America as a leading indicator to market sentiment.

The Algo Engine flagged SYD as a short signal yesterday. At this stage, we’re thinking SYD trades sideways, (rather than lower), and consolidates heading into the June dividend.

With the stock at or near $6.50, it places SYD on a 5% yield and when complimented with a tight covered call, we’re able to generate 12% annualized cash flow. If price breakdowns below $6.25, we’ll reassess the strategy.

Utilities & REIT’s, (SYD & TCL), are benefiting from US yields retreating from recent highs.

Chart – SYDChart – TCL

Sophisticated Investor?

We have special opportunities available for Sophisticated Investors. If you're interested, and qualify, please provide your details below.