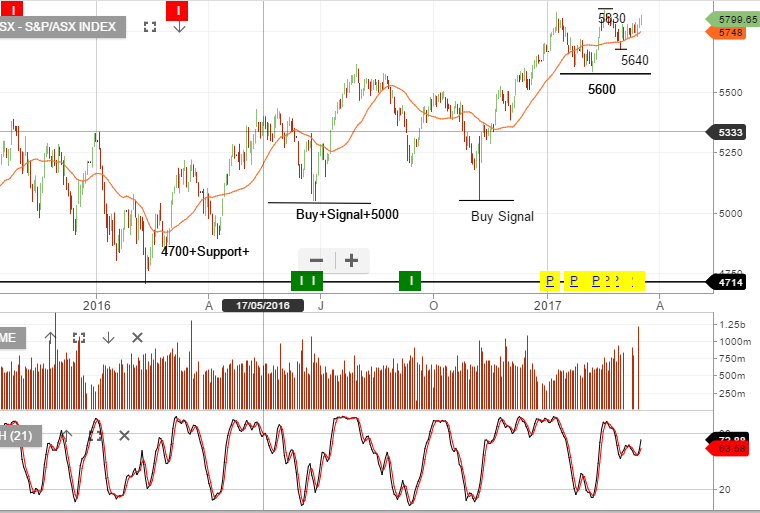

XJO – Chart Update

The XJO remains within the 5600 – 5830 consolidation range.

The XJO remains within the 5600 – 5830 consolidation range.

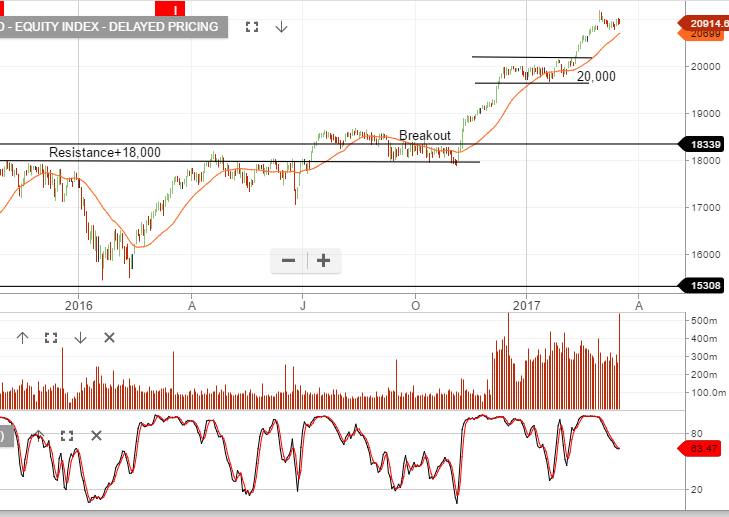

US Stock Indexes closed lower on Friday as option expiration and continued weakness in the financial sector offset gains in the industrial and utility names.

The Financial index finished the day over 1.5% lower with the major banks stocks: JP Morgan, Goldman Sachs, Citi Group and Bank of America all falling by more than 1% by the New York close.

With the SP 500 index now trading at 22 X earnings on a forward yield of just under 2.5%, the medium-term fundamentals don’t appear to support the high level consolidation at these prices.

Technically, the SP 500 index has not closed below the 30-day moving average in over 4 months.

We now see key price support at 2356.00. A break of this level would likely extend back to the February 13th low of 2310.00.

Chart below of Dow Jones Index and S&P500

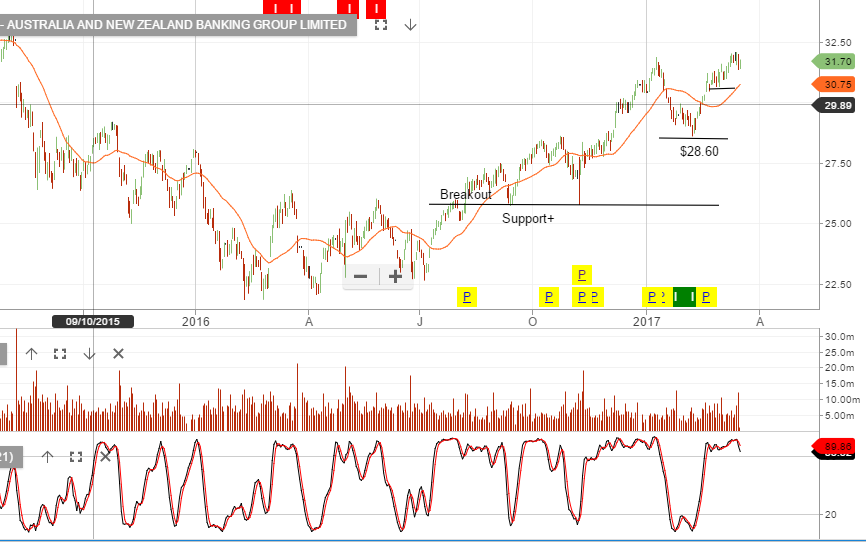

Looking at the recent run up in ANZ, NAB & WBC, it would appear that the stocks are fully valued at these levels.

Either taking profits or selling at-the-money call options to enhance the income, (whilst staying exposed to the May dividend), is a reasonably prudent approach at this time.

Chart – ANZ

Chart – ANZ

Chart – NAB

Amcor looks like it is finding support at $14.25 and could trade up to $15.00.

With the stock on a 4% forward yield and earnings likely to grow at 4 – 8% p/a we think this makes a AMC a good buy-write strategy.

The August dividend plus the call option income is generating over 10% annualised cash flow, whilst still allowing 5% capital growth over the next 6 months.

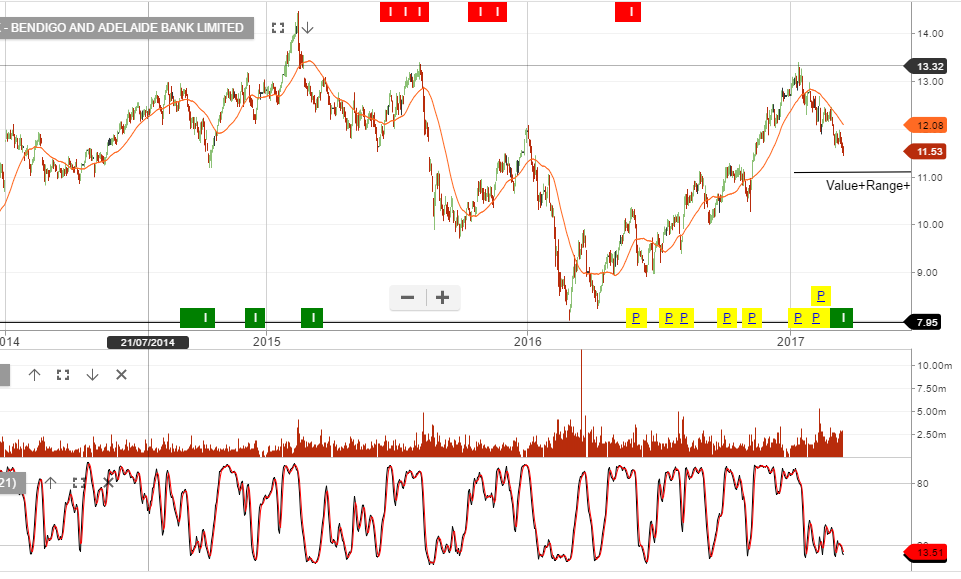

Our Algo Engine is flagging BEN with a technical buy signal.

We’re mindful of the downward pressure on the banking sector following today’s weak employment data.

Therefore, we’re not buyers at present, but we’ll be watching BEN and looking for the short term indicators to turn positive at or near the $11.00 support level.

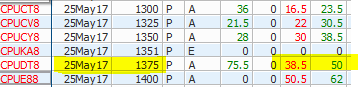

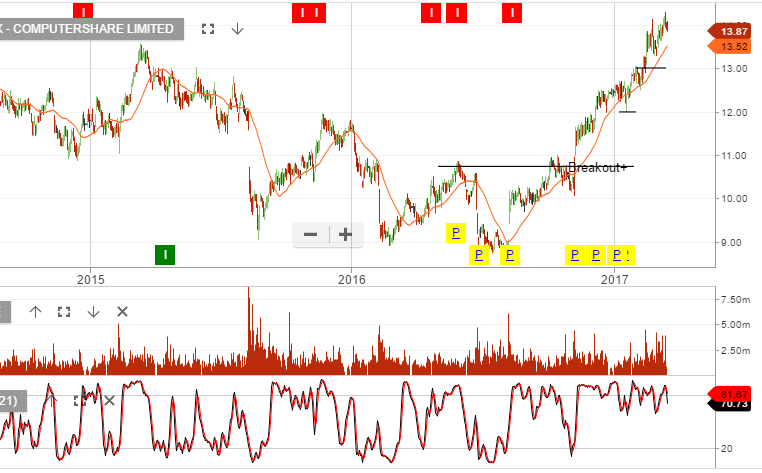

Computershare looks expensive.

We generally don’t participate on the buy-side when it comes to options on individual stocks. However, we do buy index options to hedge portfolios or to make profits on short-term corrections.

In the current environment, when some stocks look overvalued, it makes sense to buy put options on a stock specific basis.

Let’s track these over the weeks ahead as a strategy to profit from a pull-back in the share price of CPU.

We buy the $13.75 May Put options for $0.45.

The Chinese government suggests there’ll be no hard landing. China’s financial system is generally stable and there are no systemic risks. Adding, that the government has enough policy tools to handle any risks.

China’s fiscal revenue and expenditure saw faster growth in the first two months of 2017, driven by an improved economy and higher spending on social welfare, official data showed yesterday.

Fiscal revenue rose 14.9% Y/Y to 3.15 trillion yuan (US$456 billion) in January and February, accelerating from 4.5% in 2016, according to data from the Ministry of Finance.

The ministry attributed the revenue pickup to positive trends in the Chinese economy, citing improvement in industrial activity, company profits, foreign trade and resident consumption.

The government is increasing policies to curb property price inflation within major cities and stem broader capital outflows from the Chinese economy. We continue to see these two issues as risks that may yet be underappreciated by the markets.

S&P ASX Index Rebalance – March Quarter

There were two changes in the ASX50 with Aristocrat (ALL) and Fortescue Metals (FMG) added and Coca Cola (CCL) and Seek (SEK) removed.

Macquarie Atlas (MQA) & Evolution Mining (EVN) added to the ASX100 with Sirtex (SRX) and Blackmores (BKL) removed.

There were no changes in the ASX200.

Washington H Soul Pattinson (SOL) added to the ASX300.

The following group of stocks have recently been flagged by our Algo Engine.

Algo buy signals include; BHP, RIO, FMG, S32 & QBE;

Algo sell signals include; NCM & OSH.

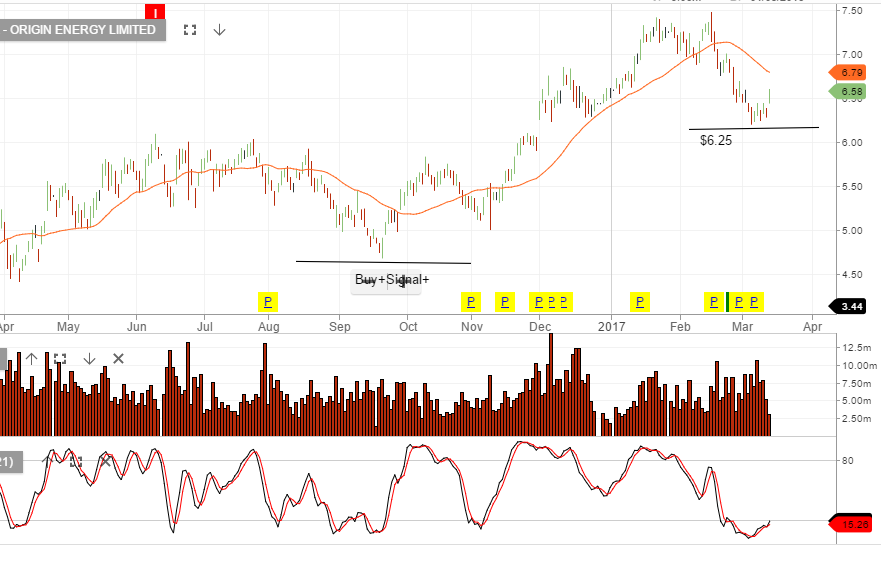

Origin continues to look well supported as the price bounces from the recent “higher low” formation at or near $6.20

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453