Seek

Telstra

ASX:TLS

Woolworths

CSL

CSL appears to be approaching a profitability low point in FY26, with FY27 expected to mark a return to earnings growth. Management’s transformation initiatives, lower plasma collection costs, and the removal of excess immunoglobulin (Ig) inventory from the US market should support margin recovery and earnings improvement. While challenges remain from competitive pressures in Ig, albumin, KCentra and Vifor pricing, the company is positioned to deliver modest profit growth.

Key Bull Points

- FY27 earnings recovery expected: FY26 is likely the trough year, with FY27 benefiting from easier comparisons, including the removal of ~$300m of excess Ig inventory and ~$300m in transformation savings.

- Behring margins should improve: Lower plasma collection costs from nomogram collections are expected to drive a noticeable gross margin recovery, supported by around a 10% increase in plasma collected per donor at no extra cost.

- Transformation programme provides meaningful support: CSL expects approximately $300m of gross cost savings in FY27, equivalent to roughly 8% of FY26 NPATA guidance, helping offset industry pricing pressures.

- Impairments are largely irrelevant to cash flow: The estimated $5 billion impairment charge is non-cash, with the main benefit being lower future amortisation expenses, which could modestly support reported NPAT.

- Valuation remains attractive: Despite lowering the price target to $158/share (from $175), the stock trades at a significant discount to the broader market multiple, offering potential upside as earnings recover in FY27.

US Earnings

Wednesday, June 10: Oracl.

Thursday, June 11: Adobe.

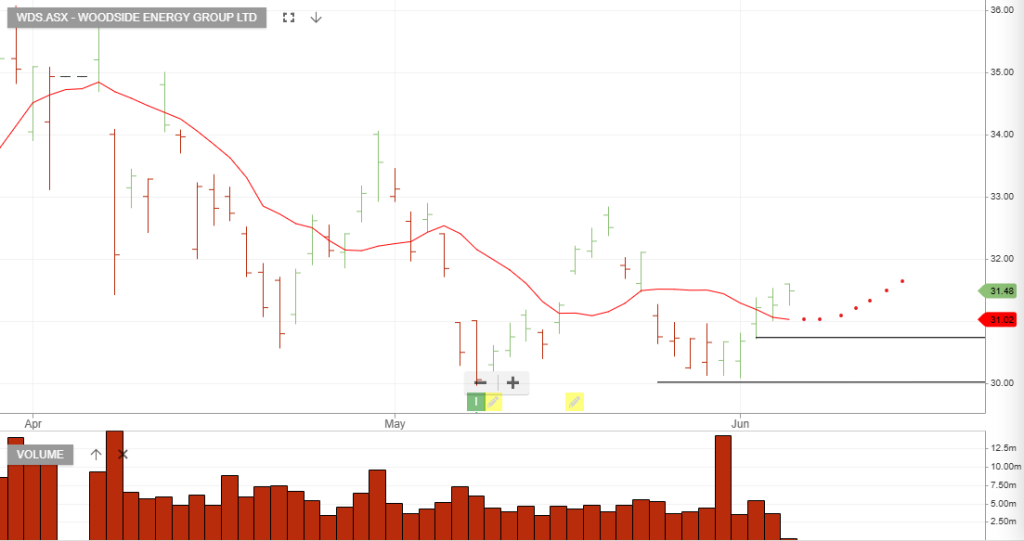

Woodside

Woodside Energy Group is rated a buy with the stop loss at $30.08

Woolworths

Woolworths Group lift stop loss to $34.26

Marvell Technology

Marvell Technology, Inc. – Common: Noted – Jensen Huang’s high-profile backing of the chipmaker at Computex.

Expected Revenue & Growth: Driven by accelerating AI data center and custom silicon demand, Marvell raised its growth guidance significantly during its last earnings call:

- Q2 FY2027 Revenue Guidance: Guided to $2.7 billion (±5%).

Year-over-Year (YoY) Growth: Represents ~35% YoY growth (beating previous consensus of $2.6 billion).

Sequential Growth: Represents ~12% sequential growth from Q1 FY2027.

- Full-Year FY2027 Revenue Outlook: Raised to ~$11.5 billion (up from prior guidance of ~$11.0 billion).

YoY Growth: Approximately 40% growth year-over-year.

- Full-Year FY2028 Revenue Outlook: Raised to ~$16.5 billion.

YoY Growth: Approximately 45% growth compared to

Medtronic

ASX:MDT releasing Q4 and full-year fiscal 2026 results, delivering its highest annual organic revenue growth in 10 years and boosting its cash dividend. Positive sentiment was also bolstered by key FDA regulatory submissions for its Hugo robotic-assisted surgery system.

Crowdstrike

CrowdStrike Holdings, Inc. – Class A Common delivered blowout Q1 results, posting revenue of $1.39 billion (up 26% YoY) and adjusted EPS of $1.10, beating Wall Street estimates. The cybersecurity firm raised its full-year guidance and announced a 4-for-1 forward stock split.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453