Brambles – Buy

Brambles is under Algo Engine buy conditions and the stock has now been added to our ASX 100 model portfolio.

The share price will gain support from the share buyback, plus the $300mn capital return.

Buy BXB

Brambles is under Algo Engine buy conditions and the stock has now been added to our ASX 100 model portfolio.

The share price will gain support from the share buyback, plus the $300mn capital return.

Buy BXB

Rio Tinto is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

We expect to see buying interest pick up near the current $93 price level.

Amcor reaffirmed their guidance for 5 – 10% EPS growth and US$160mn in cost synergies over the next 3 years from the Bemis acquisition.

Half of the forecast EPS growth is being achieved through cost savings, so the underlying business remains at low single-digit growth. The Q1 update removes medium-term downside risks and with the stock offering a 4.8% yield, we expect support to build at $14.50.

Saracen Minerals has agreed to buy a 32% stake in the Super Pit gold mine in Kalgoorlie and is raising $796 million to fund the acquisition. New shares were being offered at $2.95 each.

The raising was split into a $369 million placement and $427 million rights issue.

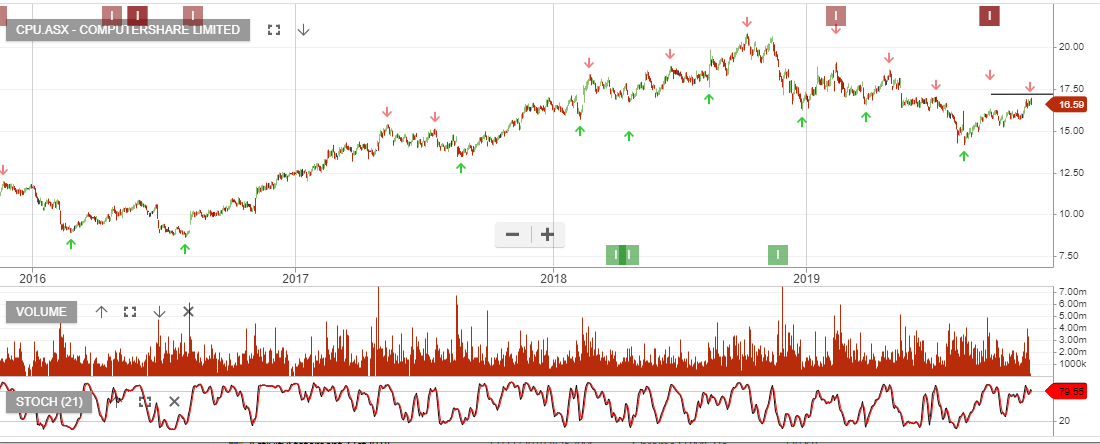

Computershare is under Algo Engine sell conditions and has been forming a series of lower high patterns since topping at $20.50 in September last year.

We continue to view the market’s assessment of the future earnings growth picture, as misguided. The factors that have lead to the recovery in earnings are transitory and the 20X PE and 2.5% yield, makes CPU too rich for our liking.

Short CPU $17.00

Scentre is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

SCG is likely to generate low levels of earnings growth, however, the weak backdrop for global bond yields and the share buyback program that Scentre Group is running, are catalysts to support our “buy” rating.

BHP Group is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

BHP outlined earlier this week its outlook for the Petroleum business, which includes an increase in capital spending and plans to double production by 2025.

FY21 revenue remains flat, EBIT the same as FY20 at $19bn, which supports DPS of $1.55 per share placing the stock on a forward yield of 5%.

The market is negative on the outlook for Iron Ore prices, with extra supply hitting the market in 2021, however, if spot prices stay where they are analysts will have to upgrade the earnings outlook. 10 to 20% upgrade in earnings will support BHP trading back over $40 per share.

Coca-Cola Amatil has hit our $10.75 price target and investors can look to lock-in the 7.5% profit or sell covered call options to enhance the cash flow return.

Altium is a buy recommendation expressed on the blog and the stock has now rallied from $31 to $34 in the past few weeks.

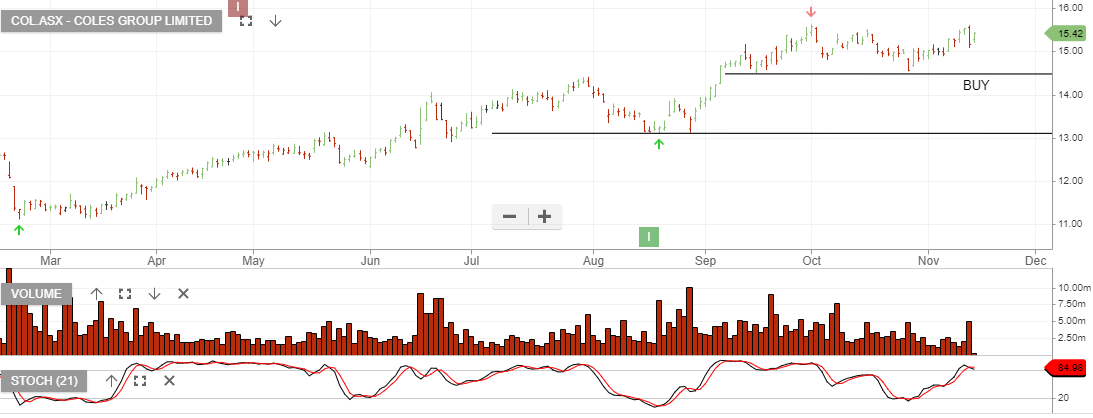

Coles Group is under Algo Engine buy conditions and is a current holding in the ASX 100 model portfolio.

1Q sales results are tracking in line with guidance and we continue to see a relatively flat revenue and profit growth outlook for the Coles business.

FY20 revenue $39bn, EBIT $1.2bn and reported profit forecast is around $830mn. This places the stock on a forward yield of 3.2%, which looks like full value.

Adding an out-of-the-money covered call will help boost the cash flow returns to almost 10% per annum. For more detail on the strategy, please call our office on 1300 614 002.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453

Or start a free thirty day trial for our full service, which includes our ASX Research.