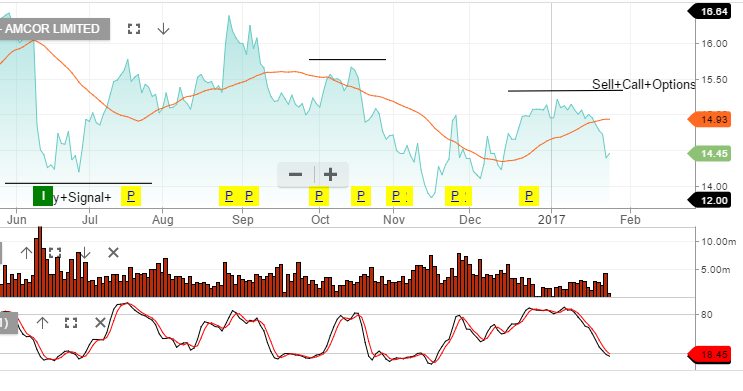

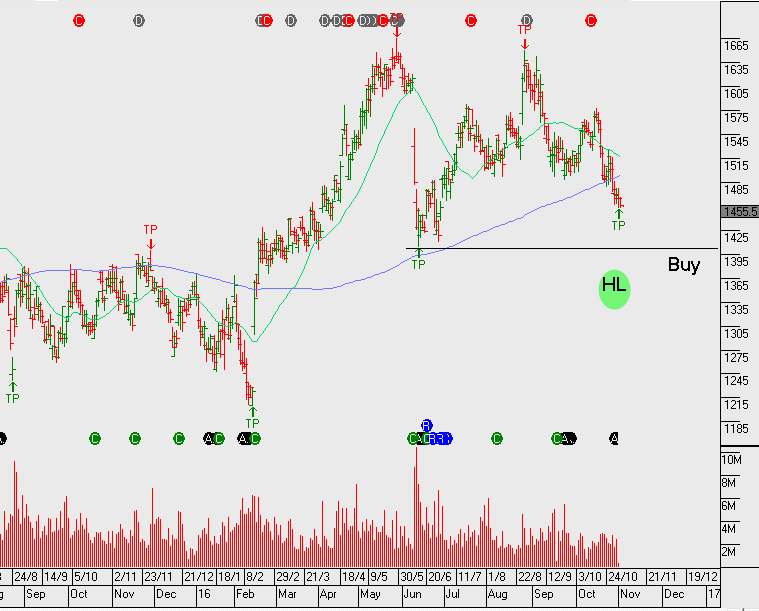

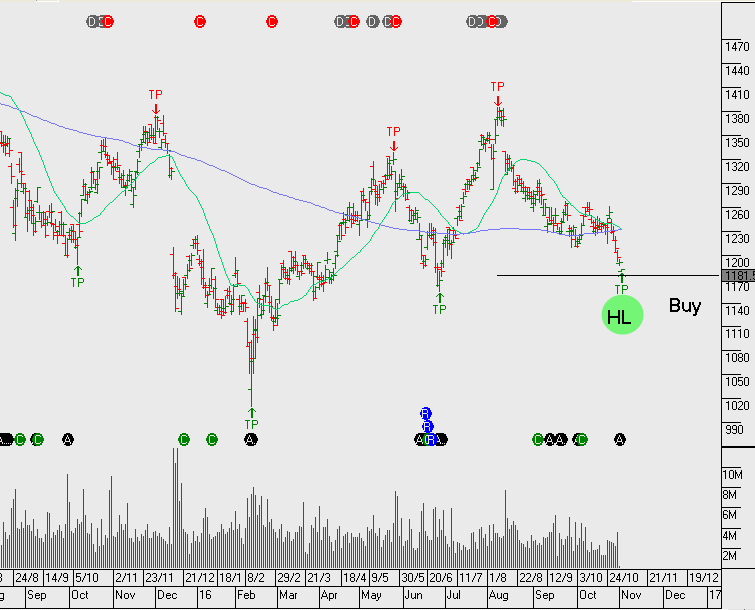

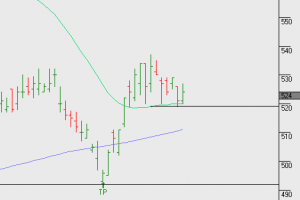

Amcor – Technical update

On February 13th, Amcor will report profits for the July – Dec 2016 period. We’re looking for the net profit to beat market consensus of $300m.

AMC trades on 17x PE and 4.2% forward yield.

We hold Amcor in our investor model and have been aggressive with selling the covered call strategy. Whilst we like the defensive qualities of the business, it’s at the top end of our valuation range.

Through adding the covered call option we’re generating 10% cash-flow from the dividend and option premium.