Our Algo Engine has triggered buy signals in Sonic Healthcare, Resmed and CSL over the past few trading sessions.

RMD has experienced its first sell-off since rallying from $10 last year to $16 only a few weeks ago.

The ALGO engine is now flagging the new “higher low” at $14 and we suggest buying a 1/2 size allocation here and then waiting to see if we get another ALGO signal to add to the position.

CSL provides good long-term fundamentals. The PE is still expensive, however, 10 – 20% EPS growth is attractive! Accumulate at $180

SHL looks to be good value at $23. We see resistance is $25, so look to sell call options to enhance the return.

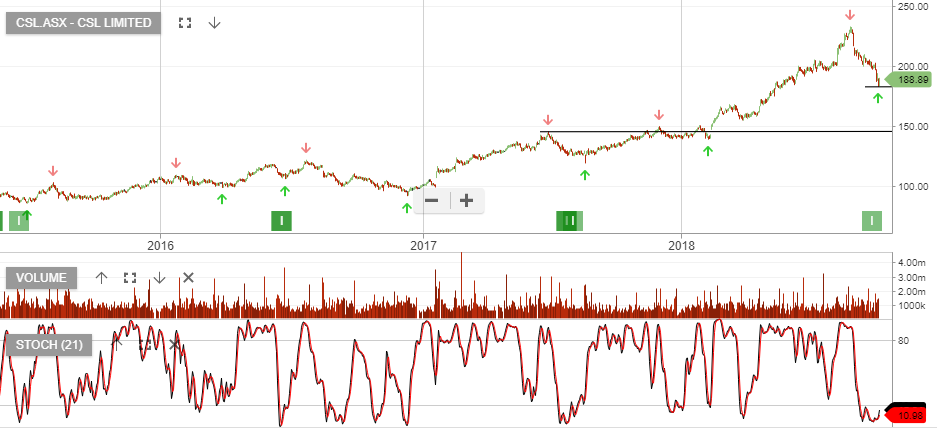

Lendlease, ASX, CSL and Aristocrat are names that we covered in Monday’s Opportunities in Review webinar.

Again, we draw your attention to these high quality businesses that have seen a recent correction in their share price.

We believe these names are close to finding support and should be the focus of establishing entry conditions. Watch the short-term momentum indicators for a reversal higher.

Shares of CSL are 1% higher at $185.00 in early trade as the company announced stronger profit guidance for FY 2018.

The updated guidance has been lifted from the previous USD 1.55 to 1.6 billion range to a USD 1.68 to 1.710 billion target.

Better than expected sales of several of their cornerstone pharmaceutical brands have supported this profit upgrade.

Despite trading near all-time highs, recent research notes have raised their medium-term price target to $190.00.

CSL is the best performing stock in our ASX Top 20 portfolio. It was first placed in the model on January 5th, 2015 at $90.00 and has gained over 105% since then.

CSL’s FY17 NPAT guidance implies US$1.38b net profit after tax.

The company has purchased 1.4m shares during 2HFY17, of the $500 million share buy-back program.

With the stock price now trading 28x FY18 earnings, much of the good news is priced in. FY18 revenue $7.2b, EBIT $2.2b, forecast net profit up 20% to $1.7b, EPS US$3.60, DPS US$1.75 places the stock on a forward yield of 1.8%.

We remain attracted CSL and look for the next Algo Engine buy signal to provide a discounted entry point.

FY18 revenue to grow 5% to US$7b, EBIT +18% to US$2.2b, EPS US$3.60 & DPS US$1.70.

This places CSL on a forward yield of 1.8% into FY18.

We own CSL and recommend a covered call into the $130 range to enhance the yield.

Chart-CSL

Cochlear was recently triggered by the Algo Engine as a buy signal and we update our 12-month share price target to $138 based on a PE of ~27.5x. and a forward yield of 2%.

Risks remain associated with COH reimbursement changes, regulatory intervention and adverse currency movements. However, momentum favors the stock at present.

The share price of CSL jumped almost 14% to $115.90 this week after surprising the market with a big earnings upgrade.

After posting a first-half profit of about USD 800 million, CSL expects net profits for the year ending June 30th to grow between 18 to 20% on a constant currency basis. This forecast included a USD 20 million headwind from unfavorable currency conversions in the AUD/USD.

However, as positive as the headline and resultant share price rally appear, we suggest that this earnings news needs to be considered within a broader context.

18 months ago the F17 NPAT expectation was $ USD 1.7 billion, 6 months ago it was USD 1.5 billion and the first estimate 2 months ago was USD 1.28 billion.

In essence, this week’s news that the profit outlook has been raised to USD 1.33 billion is considerably lower than the earnings figures that CSL was expecting just 6 months ago…….yet the share price has moved from $90.00 to $114.00.

Based on industry assessments about potential pockets of competition within the immunoglobulins area, the forward earnings trajectory could be revised again over the next few months.

As such, we consider CSL in the $114.00 to 120.00 price range to be full-valued.

Our Algo Engine triggered a buy signal at or near the recent lows of $92.

Chart – CSL

Sophisticated Investor?

We have special opportunities available for Sophisticated Investors. If you're interested, and qualify, please provide your details below.