Our Algo Engine triggered a short signal in AMP on the 9th of January when the stock was trading $5.30. The current chart pattern suggests the bounce off the recent low could be running out of steam and selling pressure may resume again.

US stocks pulled back from Wednesday’s records while the dollar strengthened on positive US data and growing expectations the Federal Reserve will soon raise interest rates.

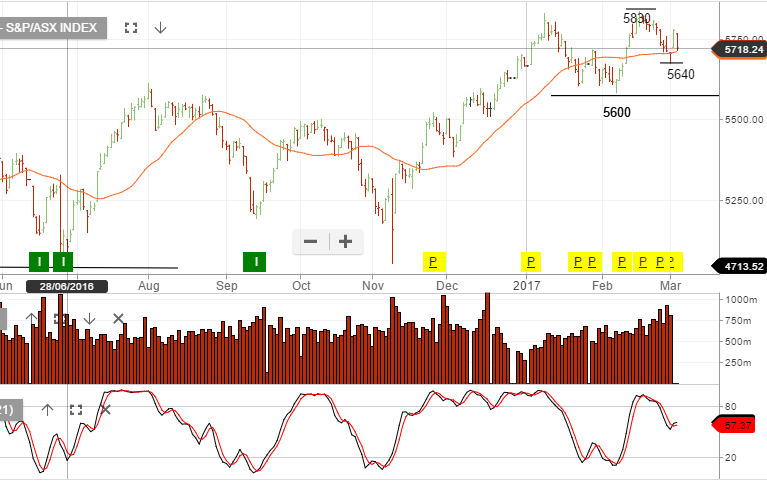

XJO is under pressure from both resources and banking stocks.

Our Algo Engine triggered a buy signal on ANN a few months back when the stock was last on the $21 support level.

With the stock retesting this level and increased buying interest occurring, we again are willing to look at ANN with a tight stop-loss under the $21 support.

In July last year, we highlighted one of our preferred US equity short signals on the blog. Target was triggered by the Algo Engine as a short signal on the 26/07/2016 at $77.

Target is now trading $57.

Chart – Target

Walmart has recently been triggered as a short from $72.80.

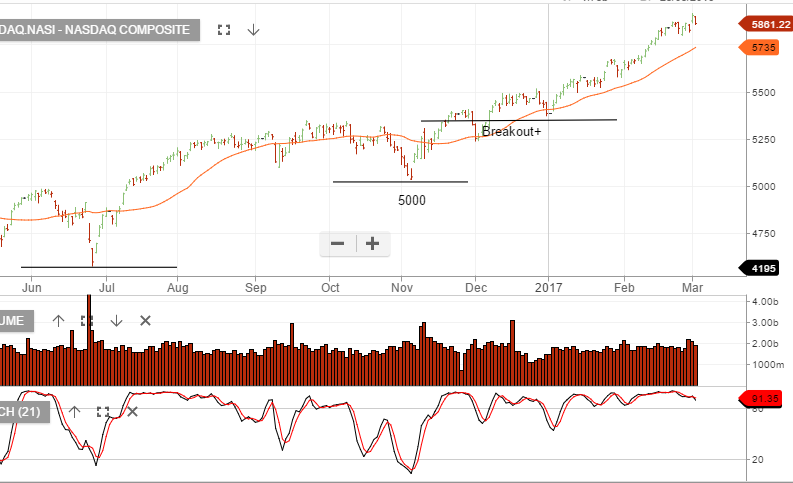

After consolidating from mid-December to mid-February, we’re now seeing US financials breakout again to the upside.

Using Goldman Sachs as a leading indicator to US financials, we form a view that it’s best to stay with the upside momentum until we see a downturn in price which takes-out the recent minor higher low at $245.

Whilst we struggle to see the EPS support for US equity valuations, momentum remains very strong. March quarter earnings to be announced in 4 weeks may provide a reason for investor’s buying enthusiasm to pause.

Chart — Goldman SachsChart – JP MorganChart – Citi Group

On the 8/2/17 our Algo Engine generated a short signal in NCM at $23.95. The stock is now trading $21.50 and the short term momentum indicators continue to track lower.

Following the sell-off in both AMC and BXB , we now are looking for buying support at or near the current levels. Our short-term momentum indicators have not yet turned positive but we’re likely getting close to valuation support, where increased buying will occur.

We see value in AMC at $14.00.

Chart – AMC

We see value in BXB at $9.25

Chart – BXB

Sophisticated Investor?

We have special opportunities available for Sophisticated Investors. If you're interested, and qualify, please provide your details below.