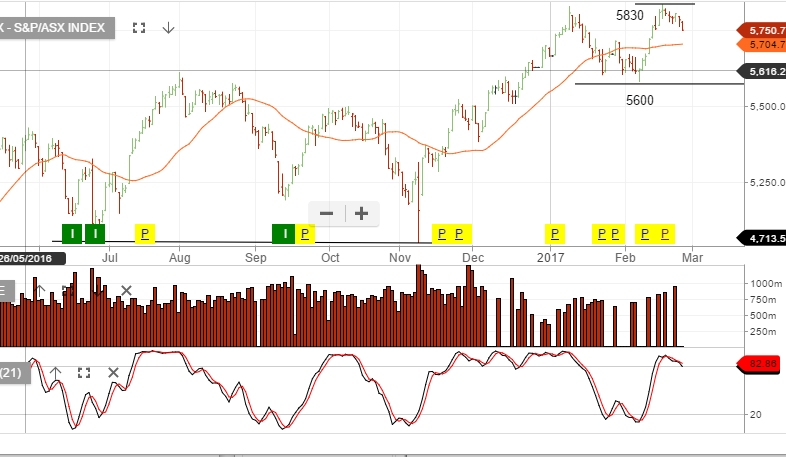

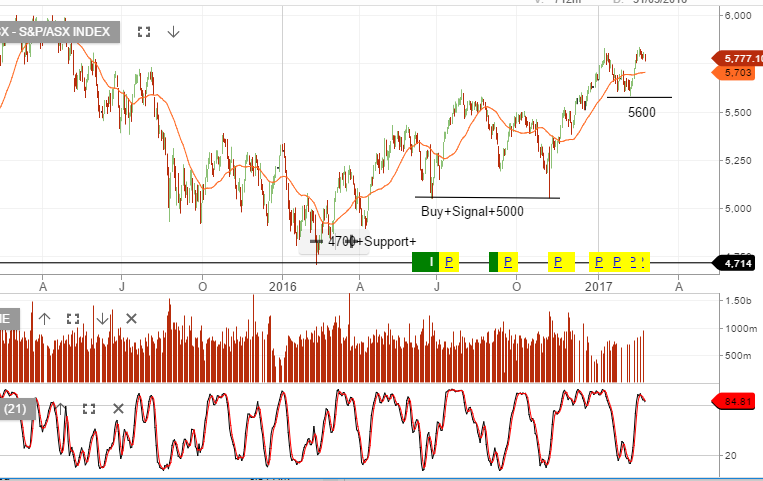

XJO – Chart Update

The XJO is now off 158 points from the 16/02/17 high of 5833. The resource sector has been the main drag, in particular, BHP and RIO.

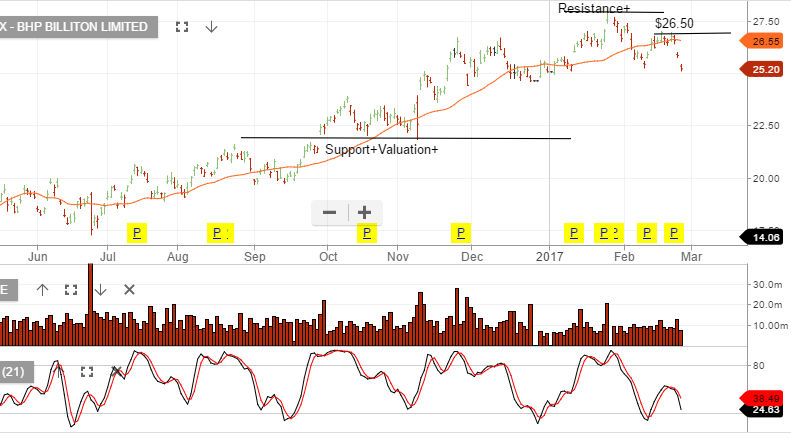

Chart – BHP

The XJO is now off 158 points from the 16/02/17 high of 5833. The resource sector has been the main drag, in particular, BHP and RIO.

Chart – BHP

Origin Energy looks like it will find buying support in the $6.25 to $6.50 range.

Woolworths trading back to $25.50 looks like reasonable value. We’re buyers on a dip in the share price at or $25.50. We see scope for 5% underlying EPS growth and when complimented with a covered call option, we’re generating 10%+ in annualized cash flow from the dividend and the call option income.

CCL is another name that we’ve been buying the stock at or near $10.00 and selling tight covered call options to generate 10 – 12% annualized cash flow .

We’ve been buying MPL and selling at-the-money covered call options to deliver an annualized cash flow of 10%+

There’s limited revenue growth, limited profit growth and a 4% dividend yield. However, we see the stock as a defensive income contributor to client portfolios.

In addition to the 10% cash flow from the dividend and option income, we’re allowing for a small capital gain over the next 4 months.

Domestic yield sensitive stocks are looking well supported as global yields in G7 economies retreat from recent highs. The bond market seems to be losing some of the optimism in the”reflation” trade.

Evidence of the retreat in yields can be seen in the US 10-YR treasuries where the yields are now trading down from 2.61% to 2.31%.

The impact of this is: money is now flowing back to REIT’s, infrastructure, consumer staples and telecommunication stocks.

We’ve been promoting the selling of resources and buying of defensive yield names, for the past few weeks. We continue to see defensive yield names complimented with tight covered call options as the best way to deliver 10-12% cash flow whilst protecting capital.

Chart – SCG

Our Algo Engine generated a short signal in AMP at or near the January high of $5.37. The stock is now trading down 10% at $4.83

A quick roll through the charts of the Dow Jones and the top 30 stocks that make up the index.

This is a great way to see the investment trends of some of the world’s largest companies.

We’ve sold $27 call options over BHP into April and quit all other metals exposure. Our preference for BHP over other resource names is based on our assumption that energy prices will remain supported in the near term.

Three factors will likely support energy prices short term: The Trump administration’s policy will likely be bullish for energy, OPEC and Saudi production cuts and the Saudi Aramco IPO early next year (biggest IPO in history). The IPO will be better received in a supportive energy environment.

For this reason we’ve kept BHP, and sold at the money call options to boost cash flow to 10 – 12%.

We’re not overweight the stock since we see risks building for the market, in general, and Iron Ore prices, specifically.

Chart – BHP

We’ve been cautious of the resource names rolling over from the recent highs and the potential negative impact on the overall XJO index. It appears that the broader Australian market may be in the early stages of a price correction.

Also, the Australian banks appear fully valued given the low revenue and profit growth outlook across the next 12 to 18 months.

The XJO remains near recent resistance as more than 50% of top 200 companies have reported their earnings. Average reported revenue is up 3.4% on the same time last year and underlying average profits are up 6%.

The Dow Jones chart shows the index breaking to the upside of the recent 20,000 consolidation range.

We remain cautious of the extended share price valuations and moderate underlying earnings growth.

For this reason we continue to tilt client portfolio’s towards defensive assets. We prefer reducing exposure to resource and banking stocks across the next quarter and increasing exposure to healthcare and consumer staples.

Our tight covered call overlay is boosting cash flow to 10 – 12% per year.

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453