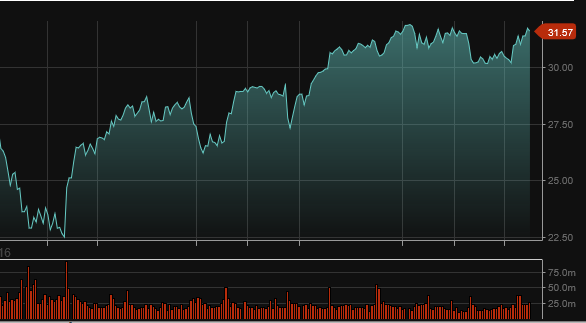

Despite reporting better-than-expected Q1 17 fiscal earnings, shares of Cisco systems have traded down to a 3-month low of $30.00 in late NY trade.

The tech giant announced Q1 EPS of 61 cents per share versus expectations of 59 cents per share on reported revenue of $12.4 billion, which beat the street’s expectation of $12.33 billion in revenue.

The share price has dropped due weaker forward guidance, as the company believes the current quarter revenue could drop 2% to 4% compared to the year-ago quarter. Analysts had forecasted a 2% rise in revenue over the same period. As a result, Cisco is expecting EPS to drop into the 55 to 57 cents per share range.

With the company expecting weaker growth, the share price could slip back to the $26.50 support level last traded in early May.

The USD has been a major beneficiary of the final result of the US Presidential election. Not only has US Dollar sentiment improved now that no protracted legal challenge will create market uncertainty, but it’s also getting a lift from the direction of current policy measures outlined by the FED and President-elect Donald Trump.

Long time readers will recall that our bullish case for the USD has been based on the theme of diverging monetary policy between the FED and the other G-7 central banks. However, now that Mr Trump is discussing some details about his economic plans, investors are now anticipating favorable fiscal policy measures which are bullish for US Stocks and the USD, as well.

During the Presidential campaign, both Trump and Clinton promised fiscal stimulus , but Trump’s plan offers more infrastructure spending and tax cuts and could top the $1 trillion mark (or 6% of GDP) by the time it’s fully implemented. At the same time, investors are growing more confident of a FED rate hike next month and the futures markets are beginning to price in a more aggressive FED. On the Friday before the election, market participants learned that US average hourly earnings rose by 2.8% on a year-on-year basis. This is the fastest pace in five years and consistent with rising core inflation pressures.

This policy mix of tighter monetary policy and expanding fiscal policy is the most bullish combination for a currency. The last time the US economy saw this this concurrent policy dynamic was after the 1980 election when the Reagan/Volcker mix sparked a 30% US Dollar rally into 1985; which was the impetus for the Plaza Accord. With little first tier Economic data scheduled in the US, we expect to see the firm tone in the USD and US asset prices continue this week.

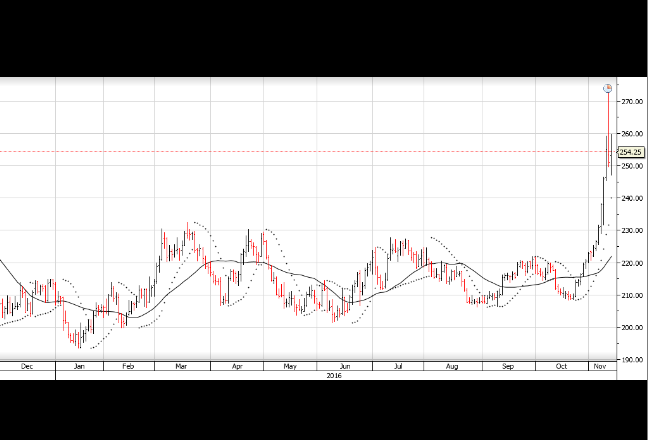

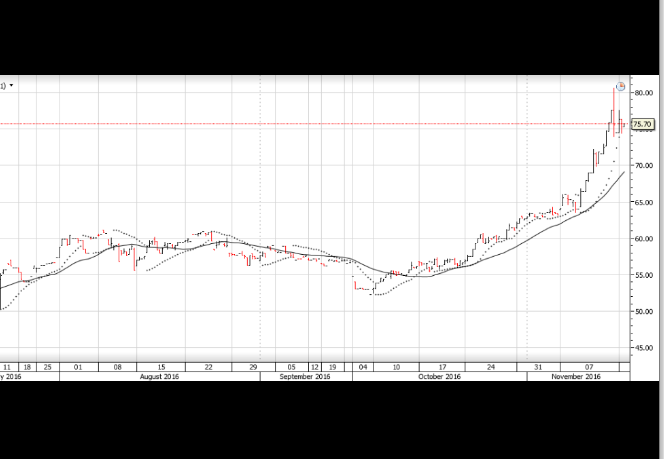

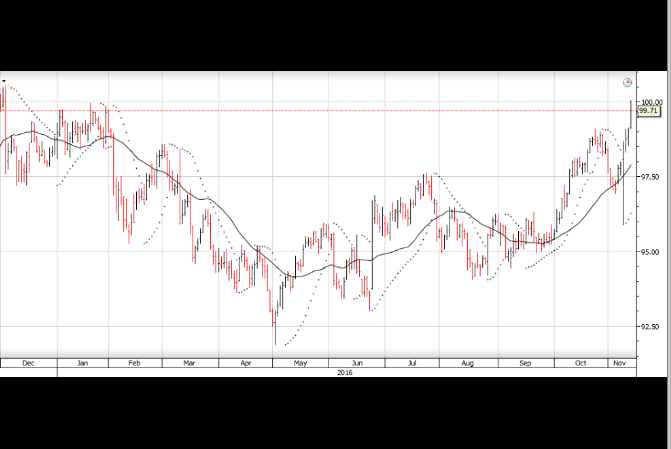

Since the Global Financial Crisis in 2008, one of the most consistently followed market correlations has been …. how the value of the US Dollar influences the price of base metals and industrial minerals including Coal, Copper and Iron Ore.

Over the last eight years, from a basic “cause and effect” standpoint, as the US Dollar appreciated against the basket of G-7 currencies, the price of Coal, Copper and Iron Ore declined; and vice versa.

However, over the last 45 days, this correlation has soften materially. During this period, the price of Comex Copper has rallied from $2.10 per pound to $2.60 per pound; a gain of over 23%. Similarly, over the same timeframe, the price of Iron Ore has risen from $63.00 per ton to $76.00 per ton for a 20% gain, and the price of Coal has lifted over 11% from $41.00 per ton to $45.50 per ton.

This has all occurred while the USD Index has traded just over 4% higher from 95.50 to 99.50.

Following Mr Trump winning the election and Mrs Clinton accepting the result, bedlam broke out in the financial markets midway through the Asian timeframe: the USD was sold off across the board, Gold rallied $60.00 to $1,335.00, the SP 500 fell limit down to 2030, bond yields plunged 15 basis points and the Mexican Peso made a new all-time low at 20.75.

However, just as the London dealers were rolling up their sleeves, calculating potential margin calls and preparing for a financial blood bath, the market dynamic changed. The catalyst of the market stabilization and subsequent rally appears to be two-fold: 1) Mrs Clinton called Mr Trump to concede defeat (which meant no chance of a protracted legal challenge) and 2) the market started pricing in the reflationary aspects of some of Mr Trumps campaign promises.

The cornerstone of his general economic plan has been the initiation of a massive infrastructure package. However, the market was caught off-guard by the announcement that part of the package would be funded by a tax concession to US corporations holding US Dollars off shore.

It’s estimated that up to $2.9 Trillion of corporate profits are being held off-shore by US companies unwilling to take the 35% profit tax charge to repatriate the money. These multi-national companies include General Electric, Apple, Microsoft and Intel……all of which have more than $100 billion parked overseas.

As the news of this proposed tax reform/amnesty plan circulated through the market, infrastructure names, heavy construction companies and stocks of military defence contractors all rallied higher. Whether or not this grand plan ever makes its way into the US economy will be determined on another day.

But as the US market heads into the three-day Veteran’s Day holiday, the USD Index is back over 98.50, US 10-yr yields are over 2.15% and the SP 500 is poised for its strongest weekly gain in over two years.

Next week the market will focus on data from the EU and Japan, but for now, global risk assets are satisfied that the transition of Presidential power will transfer smoothly and that Mr Trump is going focus on the economy first.

Yield sensitive names remain under pressure as the bond sell-off in the US continues. As bond prices trade lower, the yield is increasing. Higher yields, make interest rate sensitive names like infrastructure and property trusts less appealing.

The sell-off in domestic names such as APA, GMG, GPT, SGP, TLS, TCL, SYD, WFD & SCG has been significant. With many of these names now trading on yields within 4.5 to 6.5% range.

There’s a case to be made for the above stocks to find support as the outlook for interest rates begin to stabilise.

We’ve remained bullish equities and our base case has been that US stocks would hold support following a satisfactory 3Q earnings result. Our resolve was tested in the last 24 hours with US markets down sharply as the election result and Trump Presidency looked possible. However, by the time the Presidential acceptance speech began, the market losses on US indices were cut in half and by the close of US trading markets were up on average by 2%.

We keep our long bias towards equities and turn our focus back to the reality that 3Q S&P500 average earnings per shares growth is tracking at only 3.5% up on the same time last year. Considering the magnitude of share buybacks, we don’t consider the underlying earnings growth to be that encouraging. Chinese export data remains weak, reflecting the slow growth in the global economy and bond yields continue to push higher in the US with the 10year bonds now trading up from 1.3 to 2.05% over the last 3 months.

As stated in the monthly strategy review video, we caution portfolio investors on a blanket buy and hold strategy. We encourage you to establish contact with us, so we can discuss the advantage of adding a call option strategy to your holdings, as well implementing well timed trading ideas around the fringe of your portfolio to help deliver better outright returns.

Alibaba beat expectations in its latest report by posting adjusted earnings of 79 cents per share on $5.12 billion in revenue. Analysts were expecting 69 cents per share and $5.03 billion in revenue. In last year’s September quarter, the online retailer posted $3.28 billion in revenue and adjusted earnings of 53 cents per share.

The company announced core commerce revenue grew 41% to $4.3 billion, while cloud computing revenue increased 130% to $224 million. The adjusted EBITDA margin was 46%, compared to 50% during the same period last year.

Digital media grew by 302% to $541 million. The company also announced they had 450 million active users in September, marking a 23 million increase from June.

Shares of Alibaba rose in early NY trading, climbing as high as 104.75 before drifting back to 98.50 at the close. The share price has almost doubled since the February low of $60.50 and the next key level of support will be found at the August breakout price of $85.00

Shares of Facebook are down close to 8% in after-market trading to $117.00 even though the social media giant reported quarterly earnings that beat analysts expectations.

The company announced adjusted earnings of $1.09 per share on revenue of $7.01 billion, up from the comparable year-ago figures of 57 cents per share, adjusted, on $4.5 billion in revenue. Analysts were expecting 97 cents per share on revenue of $6.92 billion.

Advertising revenue was announced at $6.82 billion, above the $6.71 billion consensus estimate. Monthly active users rose to 1.79 billion and signalled the first time more than 1 billion users were active on their phones in a month.

However, share prices fell sharply after CFO David Wehner said the “ad load”, or number of ads on the website, could come down meaningfully after mid-2017 which could impact revenue growth in Q4 2017.

The next support level in the share price will be found at the double bottom price at 108.50 last traded in April and June.

Over the last six months, an overarching theme driving G-10 financial markets has been the divergence in interest rate policy trajectory between the US Federal Reserve and the rest of the group. From a “cause and effect” point of view, US economic data has been viewed through a prism of how it could influence policy decisions from the FOMC, which has then impacted the way G-10 assets respond relative to US assets.

In short, key fundamental data points which print better than expected have been bullish for the USD and bond yields, and economic reports which reflect weakness in the US have been bearish for the USD and bullish for US stocks. However, last Friday’s trading session illustrated how these correlations will likely be suspended until after the US Presidential election on November 8th.

Friday’s NY trading session began with the release of the highest Advanced GDP report in two years. As expected, the USD Index rallied to a 9-month high just under 99.00 and the EUR/USD slipped to the low end of the range near 1.0850. At around 1:00 PM, NY time, news hit the wire that the FBI said it would reopen its investigation into Hillary Clinton’s private e-mail server after new evidence was discovered on other electronic devices in an unrelated case. The market acted swiftly as the EUR/USD jumped 90 points, bond yields fell and the SP 500 dropped 20 handles from 2140 to 2120 before recovering.

We won’t discuss the validity of the FBI’s decision. However, from a market participants point of view, the important thing to note is that anytime there’s an opening for Don Trump to close the polling gap it means more uncertainty on the horizon and less chance of a rate adjustment this December from the FOMC. As such, we will offer to explain some of the dynamics we could be up against over the next several trading sessions.

It seems the market’s fear of a Trump victory is focused on his proposed tax cuts leading to higher deficits and a steeper yield curve. Some other analysts believe his trade policies could trigger a sell-off in equities and a flight to quality into the long-end of US Treasuries.

Using the “Brexit” vote as a point of reference, a Trump win could trigger a sharp rise in volatility in bonds, FX and equities. And while the spike in asset volatility was short-lived as the VIX moved back to pre-Brexit levels by early July, the impact on the yield curve lasted much longer. The UK referendum was on June 23rd, and it took until mid-September for the UK 10-year Gilt yields to rise above their pre-Brexit levels. There is a similar fear in the US Treasury market if Don trump wins.

In this respect, it’s our view that this week’s fundamental news (which includes 3 Central bank meetings and European PMI’s) will take a back seat to the re-pricing of last week’s forgone conclusion that Hillary Clinton will win the US election.

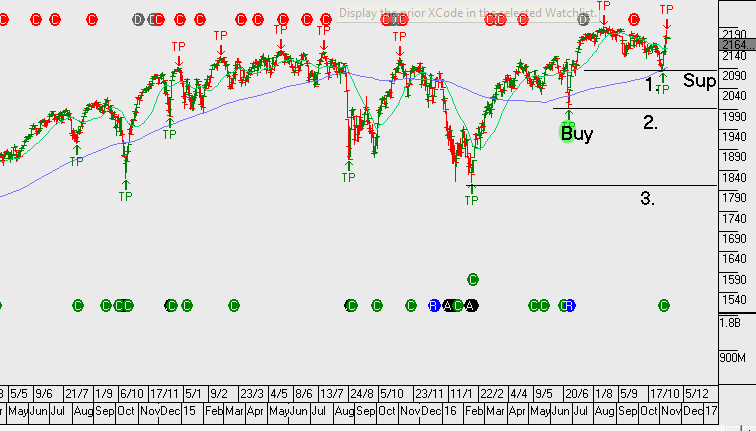

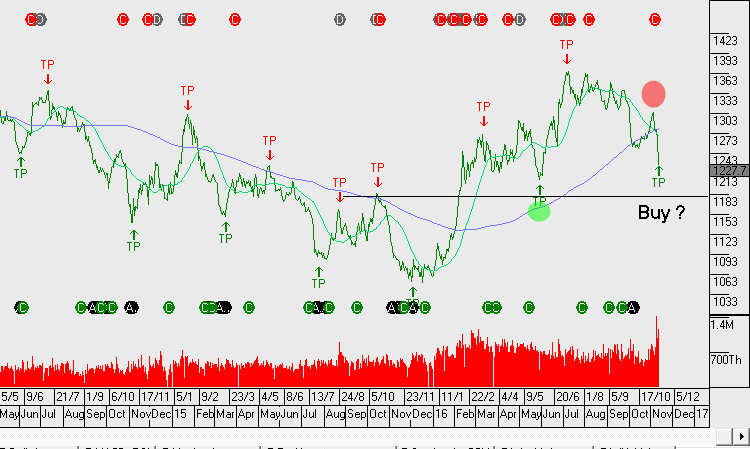

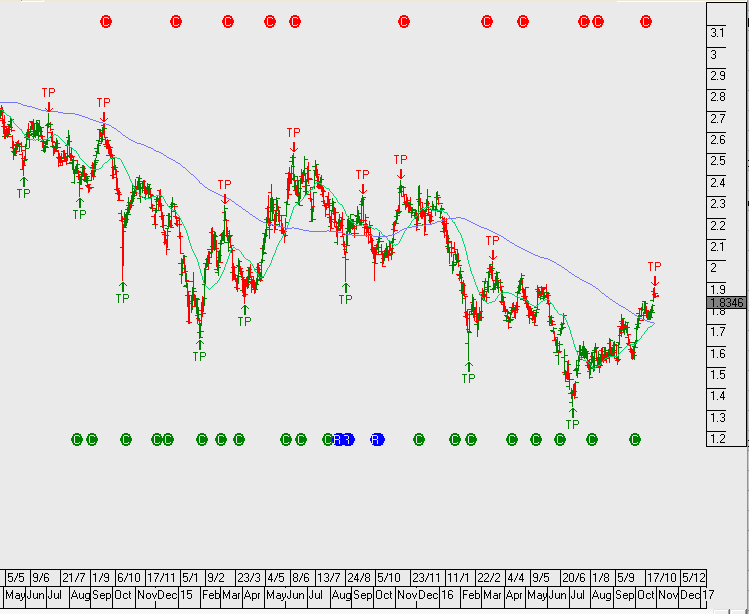

AMP 3Q16 update produced further losses and write downs in life insurance with significant deterioration in Contemporary Wealth Protection.

Going forward, the market is likely to place a greater focus on AMP’s more important wealth management business. AMP is trading on 13x FY17 earnings and now offers a 6% dividend yield.

FY17 net profit should be around $920m on EPS of $0.34 and DPS of $0.28

We’ve been cautious of AMP despite the bullish analyst forecasts over recent time. In last month’s strategy piece we highlighted the relative underperformance to other financial names. This was enough of a warning sign for us not to allocate funds, however, following the sell-off on Friday, we now think value exists in the range of $4.20 to $4.50.

Due to the elevated volatility, we prefer using a spread option strategy to capture the upside whilst quantifying or protecting our downside risk.

Chart – AMP

Sophisticated Investor?

We have special opportunities available for Sophisticated Investors. If you're interested, and qualify, please provide your details below.