We’ve been running a hedge on the Australian banks; CBA through an in-the-money European March option, NAB using an in-the-money American February option and WBC a longer-term call option. In ANZ our preference has been to exit the trade altogether.

On Friday, our domestic banks started to see some profit taking and the catalyst could’ve been selling ahead of the US banking results and/or the announcement of weaker export data out of China.

JP Morgan and BoA’s results , released last night, were adequate on the bottom line but both companies missed on the revenue front. Increased dividends and share-buybacks helped support what otherwise would’ve been viewed as weak results.

Bank profit announcements start in February with the following key dates worth noting.

SUN 9 February, BEN 13 February, CBA 15 February along with 1Q17 trading updates from ANZ and NAB in February.

Following the recent rally in bank shares, we see the current trading range as full value, therefore, placing the banks at risk of being buffeted by any increase in market volatility. Although net interest margins have improved, the prospects of earnings growth is modest with the outlook between 1% – 4% growth at both top and bottom-line.

We also remain concerned that the cycle for bad debts is likely to rise from the current historic low levels.

Currently, ASX leading Financials are being dragged higher as the US equity rally continues into the lead up to their fourth quarter earnings results. We’re somewhat sceptical of the valuation support and yesterday started hedging our banking exposure in client portfolios. This was done through using in-the-money European-style calls over CBA and slightly in the money February calls over NAB, as two examples.

In the case of CBA, we stay exposed to the February dividend and franking credit but have hedged a price pullback of up to 5% between now and March.

In NAB, we’ve hedged to a similar extend but without the need to protect the dividend. NAB’s next payment period is not until May

There is a saying in the financial markets that a “rising tide floats all boats” This old adage has been used recently to describe how the rally in US bank shares has lifted the share prices of Australian banks.

Since November 4th, shares of Citibank have gained 14%, shares of JP Morgan have gained 16%, shares of Bank of America have risen by 17% and Goldman Sachs shares have rallied by over 20%.

Over the same period of time, shares of ANZ have gained 6%, shares of Westpac have gained 8%, CBA shares have lifted by 8.5% and shares of the NAB have rallied by 11%.

Interest rates in the US began bottoming out in late September, which was positive news for most US financial names. In addition, the election of Donald Trump is being hailed as a “game changer” for the U.S. banking sector, as the Republican sweep of the White House and both houses of Congress appears to have shifted investor’s expectations about interest rates, regulation and the broader business environment.

With respect to the Australian banking names, these two key points aren’t applicable.

The RBA may have moved to a neutral bias on domestic interest rates, but there’s no realistic expectations for a rate hike anytime in the foreseeable future. And, if any regulatory changes are legislated in the Australian banking industry over the next 12 months, they are more likely to be restrictive, as opposed to accommodative.

With this in mind, we will use this recent rally in Australian banking names to implement our derivative overlay strategy and sell covered call options to enhance returns on bank share holdings.

Stay tuned to the Investor Signals daily blog for specific timing and price information.

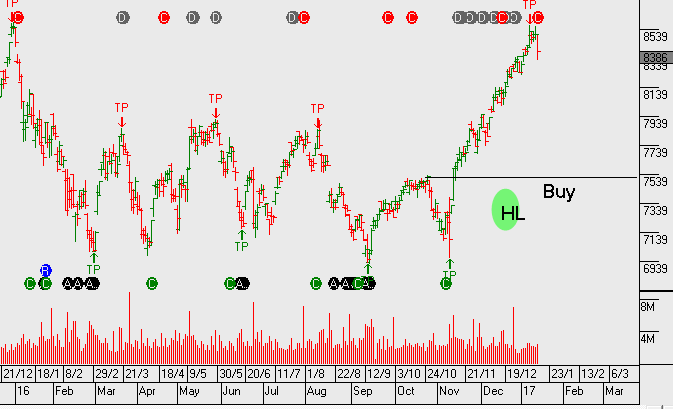

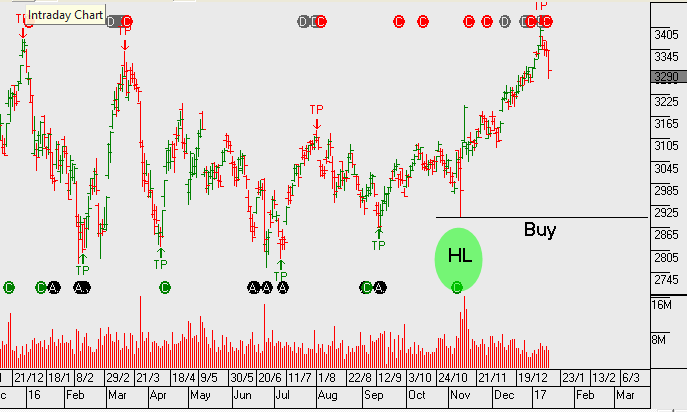

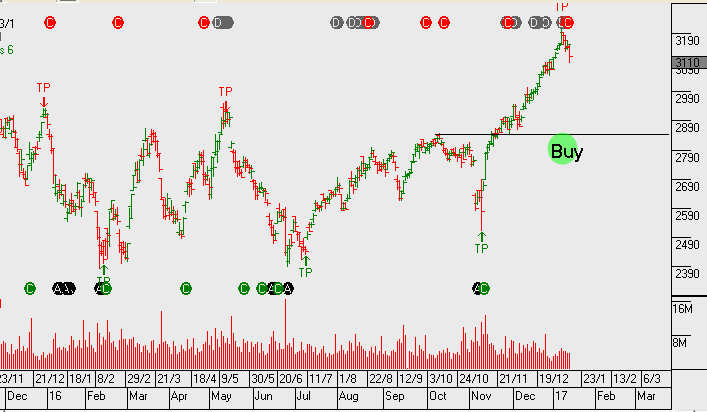

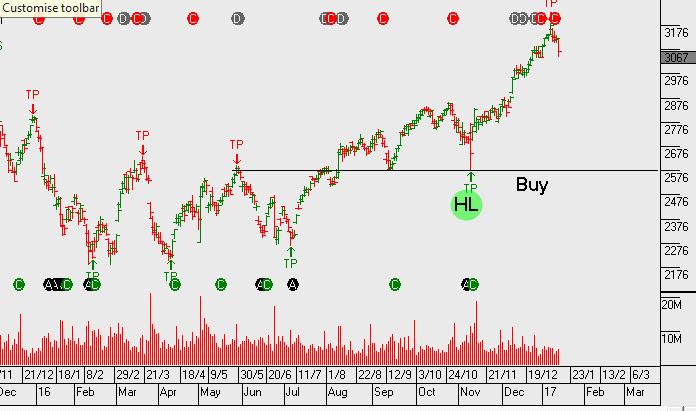

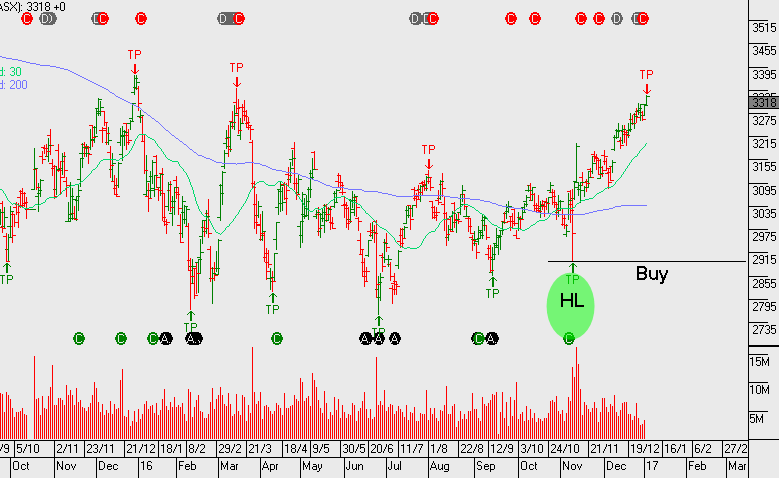

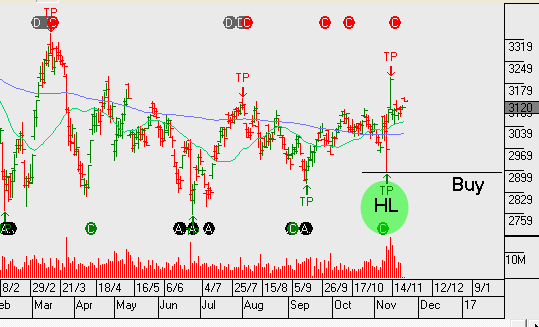

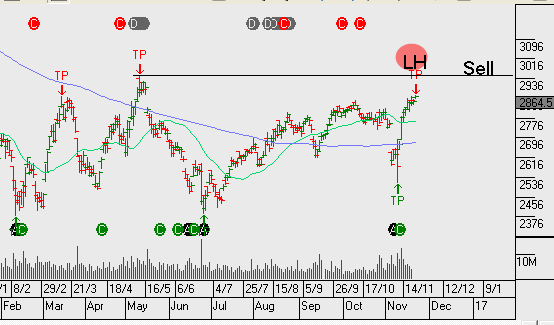

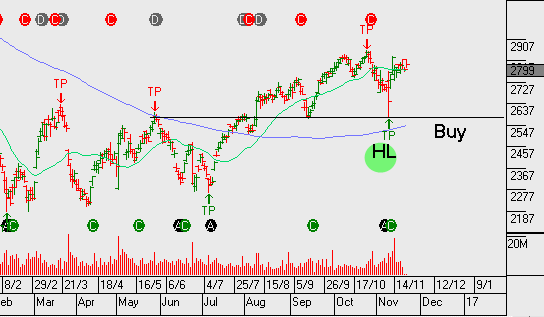

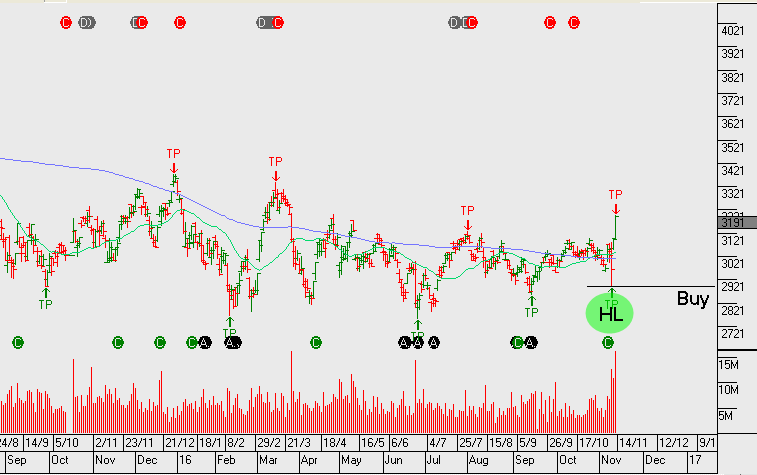

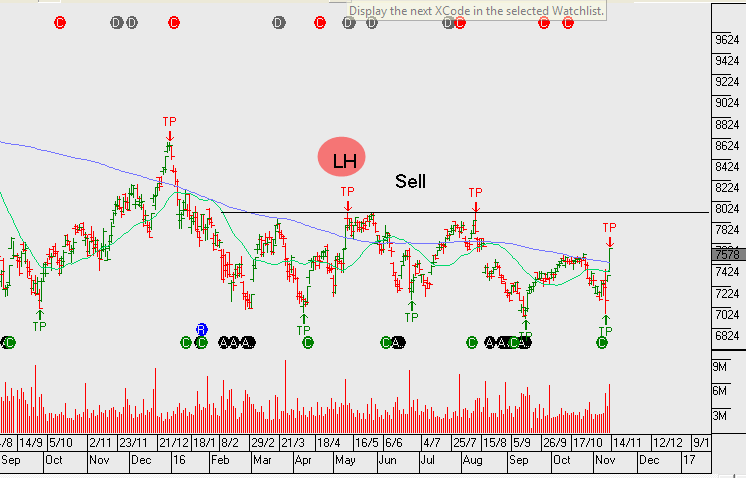

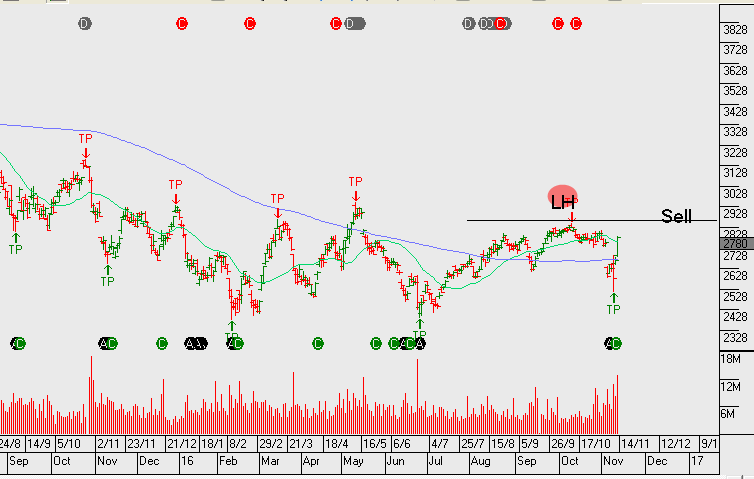

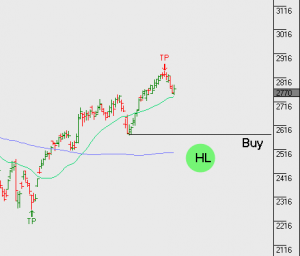

We now have ANZ and WBC creating a higher low formation. However, CBA and NAB still remain below the recent highs within the downtrend that’s been in place since May 2015.

Back in August, ANZ was the first to break the downtrend and now WBC has followed. Within the regional banks, between BOQ and BEN, it’s Bendigo that’s displaying a more bullish price pattern.

Although the breakout in financials is strong at present, we don’t see too much further upside. As reflected in the recent earnings results, the banks are having difficulties growing top line revenue. Our largest bank exposure in client portfolios is Westpac. We’ve left this name uncovered at present, however, it’s likely we’ll identify a point this week to add covered calls to enhance the yield.

ANZ goes ex-dividend $0.80 on Monday & WBC also goes ex-dividend $1.00 on Monday.

The following group of stocks are in either established uptrends or, in recent months they’ve broken downtrends to begin building the early stages of a bullish “higher low” formation.

Many of these names have been mentioned previously in the blog and/or the monthly strategy video report. It’s worth loading these codes into your watch list and considering rebalancing your portfolio to include allocations towards some, or all of these names:

With the lower growth names within the above basket, such as WOW & CCL, we compliment the position now with tight covered calls to enhance the yield to 10%+ per annum. With some of the other names, we give a little more breathing space as we expect 5 to 10% price appreciation before selling the call option overlay.

The upcoming bank results will likely demonstrate that revenue and profit growth estimates may be too high.

We are expecting cost control to become an increasing focus for investors analysing bank results. Pressure continues to build on Boards to reconsider their dividend positions. Payout ratios at 80% appear too high given the added capital requirement banks face in the next 18 months.

WBC and NAB are likely to modestly reduce dividends. Out of the 4 majors, ANZ is the only bank with positive a technical structure.

ANZ.ASX ANZ’s 3Q16 update – earnings trends looked a little soft with a pickup in NPAT growth required in 4Q16 to reach consensus forecasts.

Asset quality trends also looked a little disappointing. FY17 forecast EPS growth 2% which places the stock on a forward yield of 6%.

From a technical perspective it’s worth noting the banks have now taken out the most recent highs of the long established down trend that has been in place since May 2015.

The next round of buy signals in the banks will be worth closer consideration.

Sophisticated Investor?

We have special opportunities available for Sophisticated Investors. If you're interested, and qualify, please provide your details below.