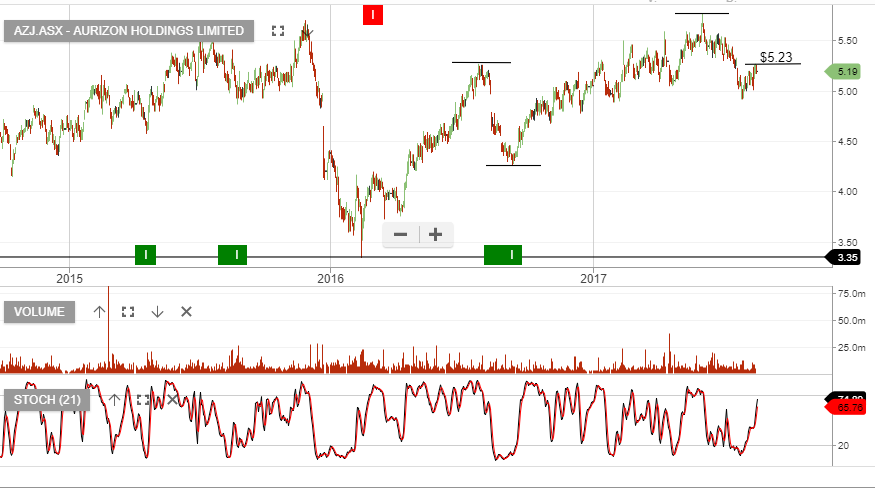

ALGO Buy Signal For AZJ

Our ALGO engine triggered a buy signal for Aurizon Holdings on Tuesday at $4.24.

This “higher low” chart pattern is referenced to the low of $4.10 posted on June 13th.

AZJ’s FY2018 results, which were released last week, showed a modest 1% decrease in revenue from last year, but the underlying EBIT of $940 million was up 6% from 2017.

With a total dividend of 27 cents, the stock has an effective yield of 6% at current prices.

We expect the initial price target of $4.60 to be reached over the medium term.

AZJ