BHP

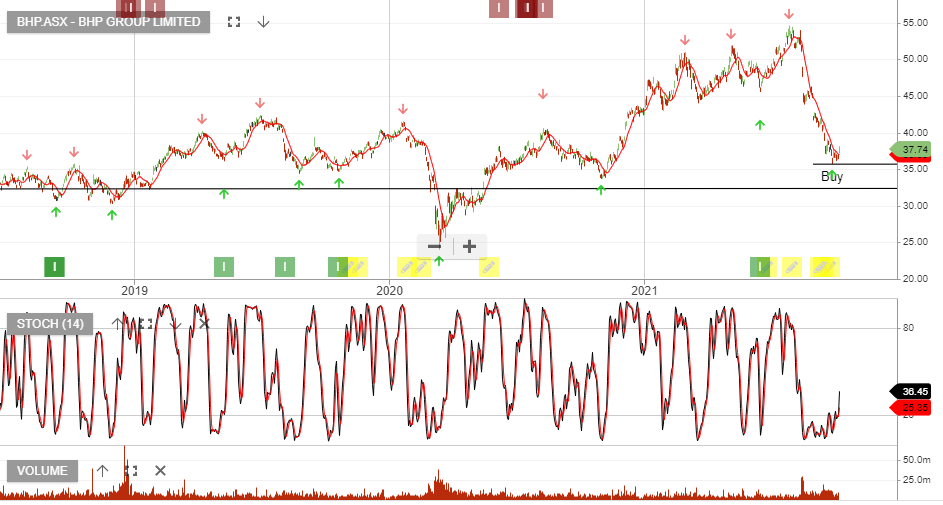

BHP Group has formed a FTFF level of support at $45.

BHP Group has formed a FTFF level of support at $45.

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

Sorry, but this content is restricted to our members.

Please login with your account or register for a free trial. If your trial has expired, then you may renew it here.

If you are having an issue with your account, then please get in touch with us.

BHP Group is under Algo Engine sell conditions. 1HFY22 result was strong with headline earnings above consensus and impressive cash flow supporting a higher dividend, Iron-ore being the dominant contributor.

First-half net profit US$10.68bn.

BHP Group is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

BHP Group is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

BHP Group is under Algo Engine buy conditions and is a current holding in our ASX 100 model portfolio.

Iron ore +5.4% to $US123.38 a tonne

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453