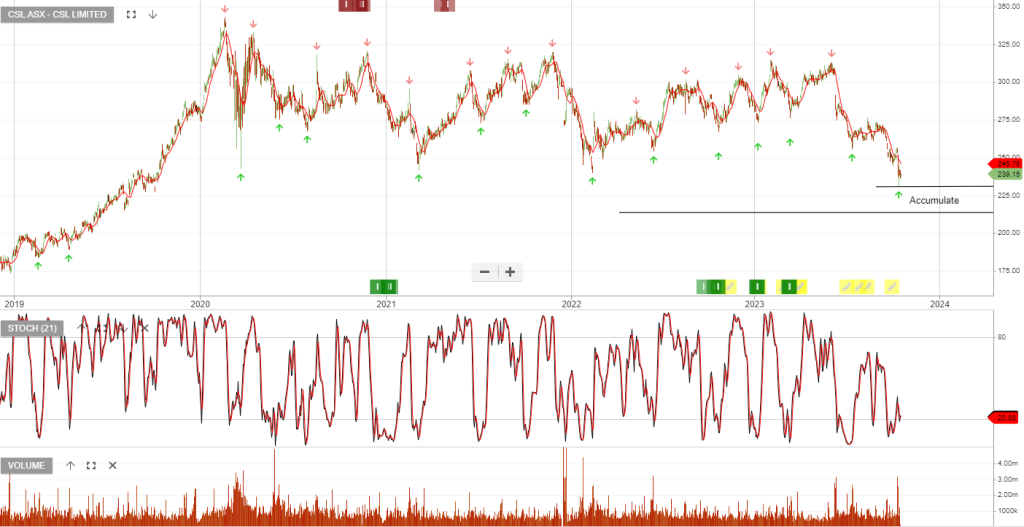

CSL

CSL is under Algo Engine buy conditions.

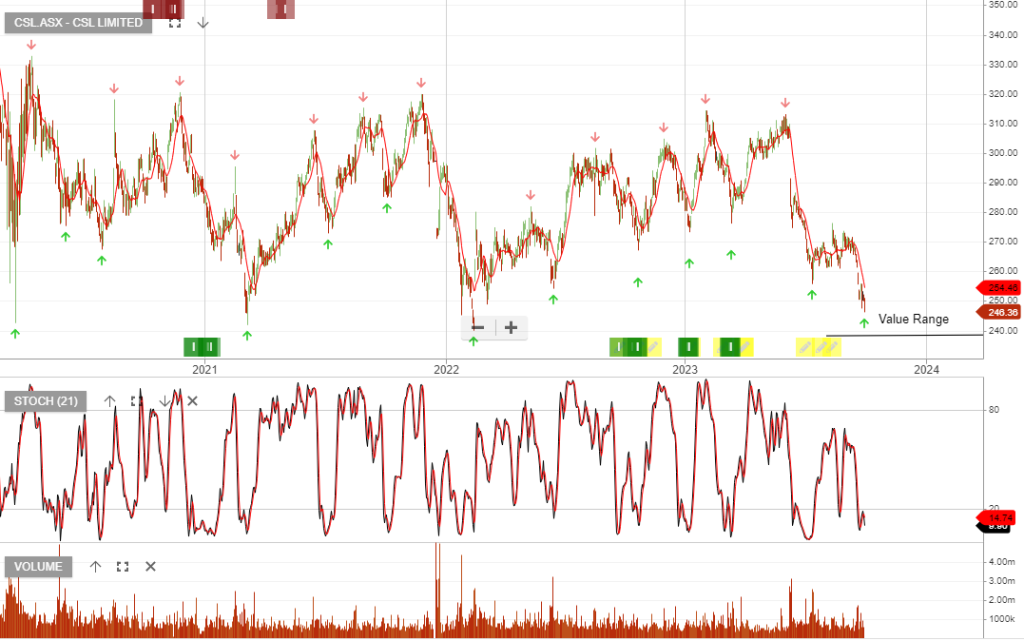

CSL

CSL is under Algo Engine buy conditions.

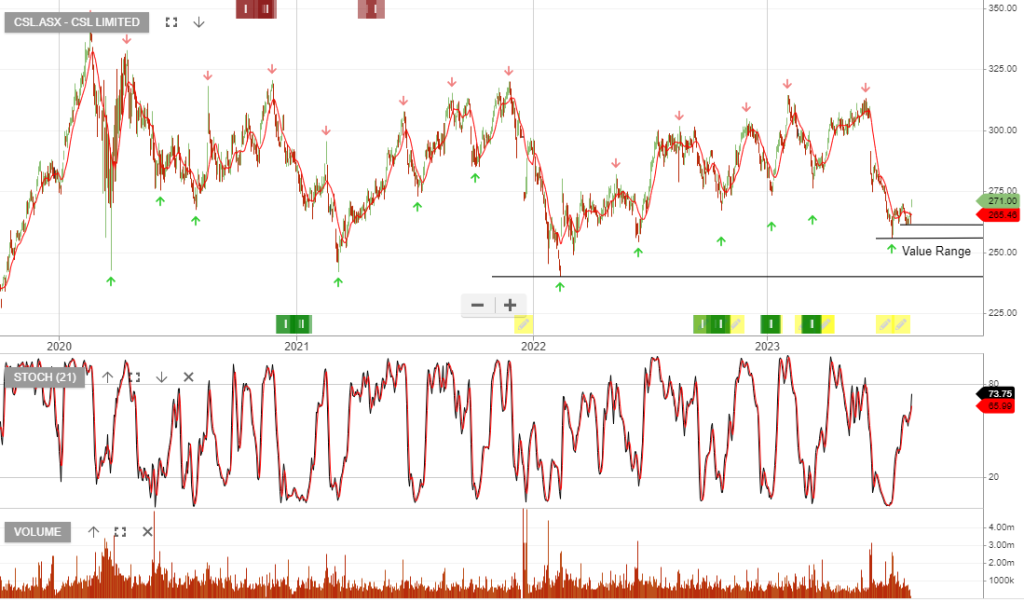

CSL

CSL is under Algo Engine buy conditions.

CSL: Buy

CSL is under Algo Engine buy conditions and we are looking to add to the portfolio holding within the $200 – $240 range.

CSL

CSL

CSL

CSL FY23 revenue $13.31bn, up 31% on FY22 and NPAT of $2.19bn, down 3%. FY24, revenue growth is anticipated to be 10% with NPAT of approximately $3.0bn, representing 12% growth.

CSL

CSL

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453