The recent market rotation towards growth assets and in particular, materials and financials, has resulted in selling utilities and property trusts. In many cases, these names have seen 10 to 20% correction.

The following post takes a quick look at some of the relevant chart patterns.

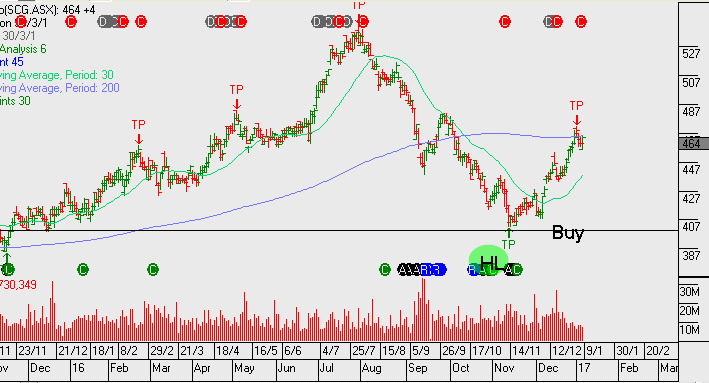

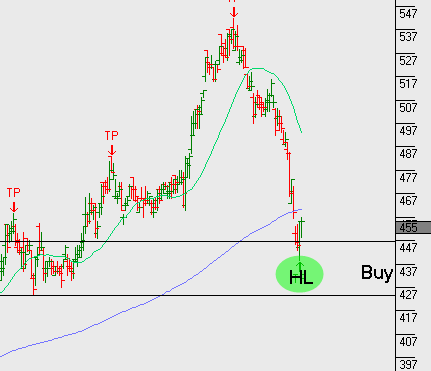

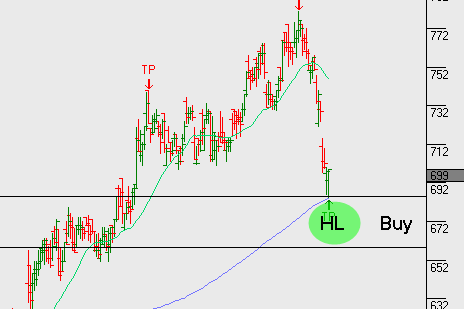

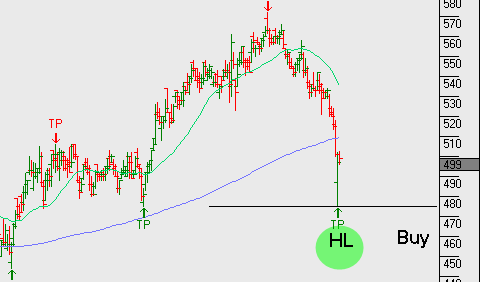

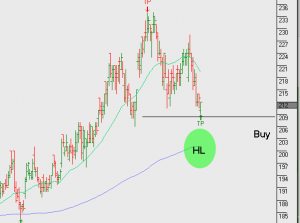

SCG.ASX (forward yield 4.9%)

SGP.ASX (forward yield 5.5%)

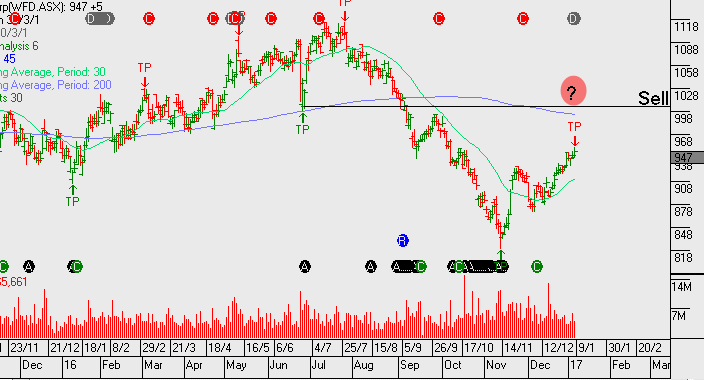

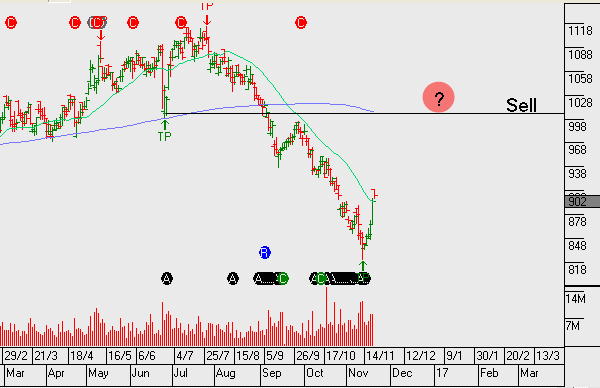

WFD.ASX (forward yield 3.5%)

DXS.ASX (forward yield 5.2%)

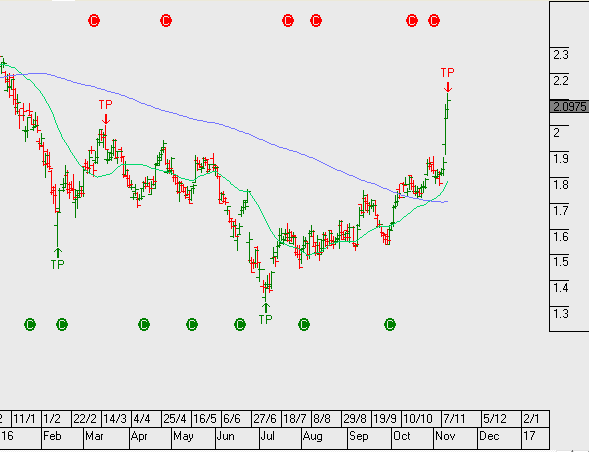

GMG.ASX (forward yield 3.7%)

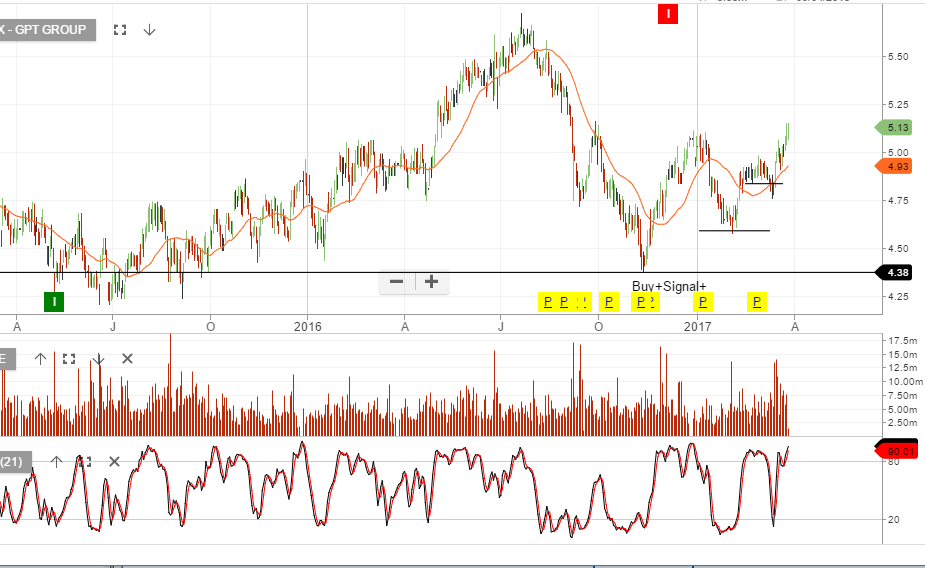

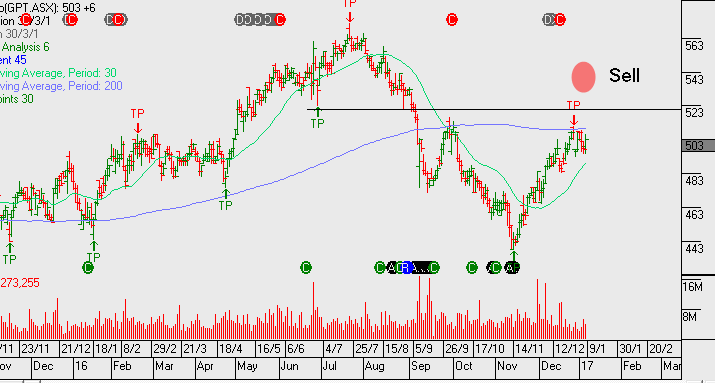

GPT.ASX (forward yield 5%)

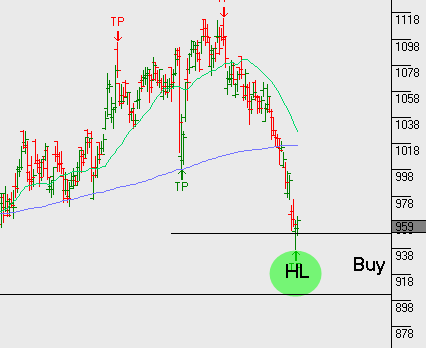

MGR.ASX

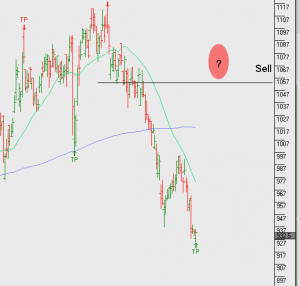

On the utilities, we think that both Sydney Airports and Transurban should be back on the radar and maybe looking oversold.

SYD.ASX (forward yield 5%)

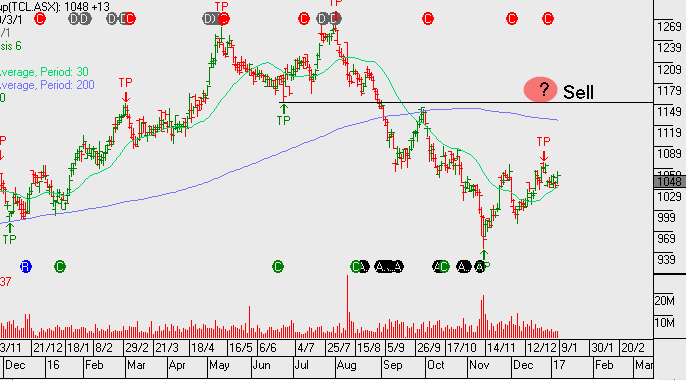

TCL.ASX (forward yield 4.8%)