Origin Energy 1Q21 Production

Nat Gas prices continue to rebound from the historic lows reached mid this year.

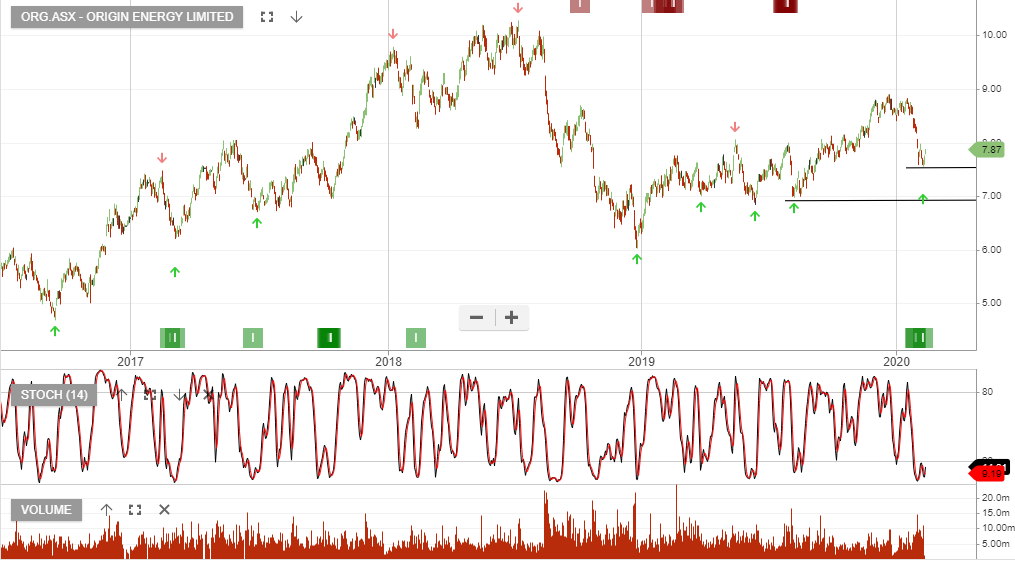

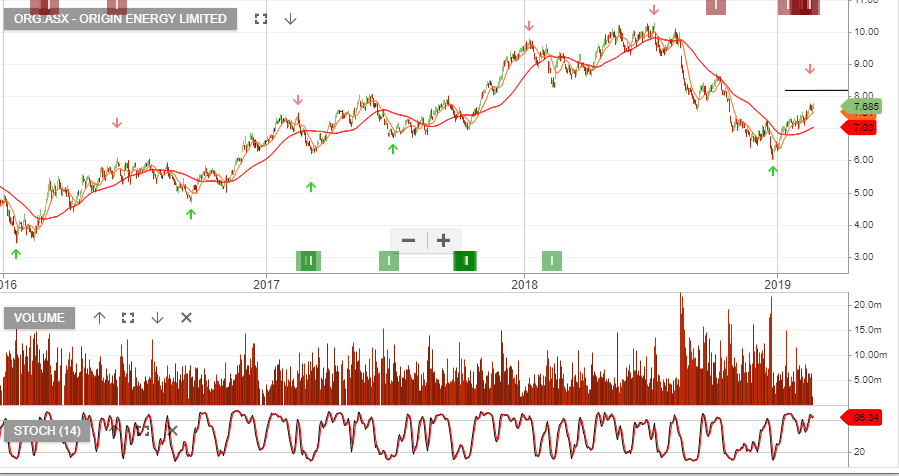

Origin share price remains under selling pressure but is likely to soon find buying support.

Origin’s September quarter revenue of A$374m was down 39% from the prior quarter. Lower prices were in part offset by higher production volumes.