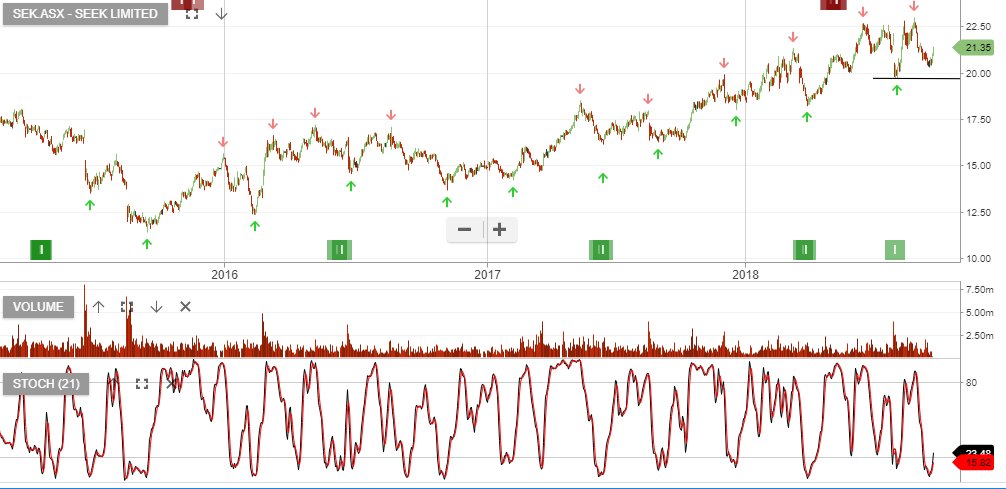

Seek – Price Support At $20.50

Our Algo Engine generated a buy signal in Seek at $19.70 back in July.

With the current share price finding support, (at a new higher low formation), we see this as a viable buy-write opportunity.

June $22.50 call option will generate an additional $0.75 per share of income. Seek goes ex-dividend $0.24 on the 26th of March.

Aristocrat Leisure

Aristocrat Leisure