Brambles – Opportunity Approaches

Brambles FY20 earnings were in-line with market expectations and the relatively defensive income mix is appealing.

Buy BXB on weakness, $10.50 is support.

Brambles FY20 earnings were in-line with market expectations and the relatively defensive income mix is appealing.

Buy BXB on weakness, $10.50 is support.

Brambles remains under Algo Engine buy conditions.

FY20 earnings were in-line with market consensus with EBIT flat on the same time last year. On a constant currency basis, EBIT increased 4%, which was in-line with management guidance for 3 – 5% growth.

BXB generates a large percentage of its revenue from consumer

staples and grocery supply chains, making it a relatively safe harbor for investors. At 22X forward earnings and a 2.2% yield, there’s not much upside in the share price on a 12-month outlook.

We suggest investors add a covered call option to enhance the income return.

Brambles is now under Algo Engine buy conditions and has been added into our ASX 20, 50 & 100 model portfolios.

Brambles Our recent buy advice on BXB is playing out favourably. The stock is now up 5 percent + from our entry-level.

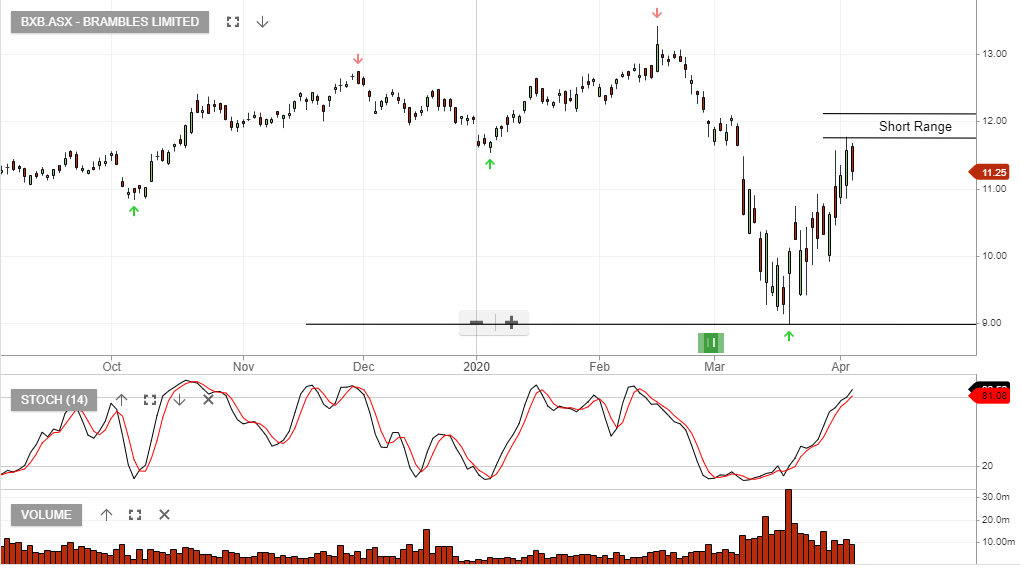

The chart below displays the technical support.

Look for the short-term momentum indicators to roll over and selling resistance to build within the range indicated below.

Since the above post, BXB ran into selling pressure at $12.25. At $10.50 BXB is back in a range where buying is likely to rebuild.

Brambles is under Algo Engine buy conditions and the stock has now been added to our ASX 100 model portfolio.

The share price will gain support from the share buyback, plus the $300mn capital return.

Buy BXB

Brambles is under Algo Engine sell conditions and we’ll review the FY19 earnings result with interest when announced on the 21st of August.

Earnings are likely to come in below the “moderate growth” expectations. We think the number will be flat to negative. Downside risks to the share price are underpinned by the share buyback which will recommence, post the earnings result.

Based on FY20 earnings we have BXB trading on a forward yield of 2.5%.

Brambles has announced the sale of its IFCO business to Triton & Luxinva for US$2.51bn. The proceeds will be used to:-

$300m return of cash through a $0.29 special unfranked dividend and up to $1.65bn on-market buy-back. The balance will go towards reducing debt.

Our key concern with BXB is the recent earnings result showed underlying EPS growth of 2% and with the stock trading 22x earnings, it looks expensive.

Brambles BXB reported 1H19 earnings which showed solid revenue growth but only a modest 2% profit growth.

EBIT from 1H19 continuing operations of US$504m.

We expect FY19 underlying profit growth to show low single digit improvement on the same time last year.

The stock looks slightly expensive at 19x and 3% yield. We’re looking for a pullback to sub $10.50 before reconsidering.

The IFCO separation remains on track for completion this year and will help underpin the share price.

Brambles is under Algo Engine buy conditions and is a current holding in ASX 100 model portfolio.

We see value at $11.60

Level 17 Chifley Tower

2 Chifley Square

Sydney, NSW 2000

1300 614 002

Investor Signals Pty Ltd

ABN 44 143 555 453