The Spot Iron Ore price continued to trade lower overnight, losing 4.6% to reach a 6-month low of $63.20 per dry tonne. This is a 33.5% drop from the high of $95.00 last traded on February 21st.

It’s worth noting that the sharp selloff is picking up pace just weeks away from the delivery of the Australian Federal Budget.

Since Iron Ore remains the country’s single biggest export, Federal revenue projections are highly sensitive to the outlook for Iron Ore prices.

Both RIO and BHP have traded lower on the open, reaching new 5-month lows of $57.60 and $23.30, respectively.

Unless Iron Ore stages a dramatic rebound, we look for the the next key support level in RIO at $56.20, and at $22.60 for BHP.

Shares of RIO Tinto have opened over 2% lower as both Iron Ore and Copper prices fell sharply in overnight trade.

Iron Ore prices seem to be in free fall, suffering an 8.5% drop to $68.00 per tonne. This is the largest overnight fall in over a year and extends the losses since February to over 28%.

Copper prices fell over 5% to $2.54 per pound in NY trade. This is a new 5-month low and technical indicators are pointing lower.

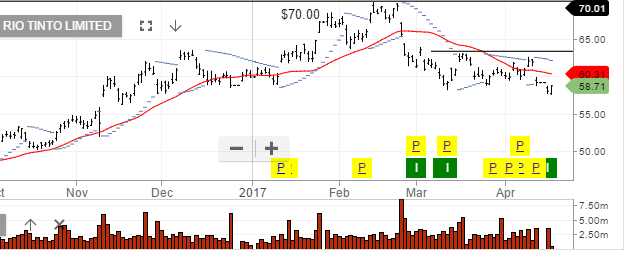

Rio shares are currently at $59.50. We see a key support area at $58.40, and would suggest a break of that level would extend materially to the downside.

Although many resource names have enjoyed a strong rally over the past 12 months, there’s reason to be cautious.

To protect capital we recommend investors holding resource names, run tight stop-losses below the recent lows.

Overall, investors should be reviewing their portfolio allocations, tilting to defensive names and ensuring access to effective portfolio hedging and shorting strategies are in place.

With the financial media focused primarily on the US missile strike in Syria, many investors didn’t notice the 7% drop in Iron Ore prices on Friday.

The spot price of Iron Ore fell $5.50 to $75.45 yesterday. This is over 20% lower than the February 21st closing price of $95.00.

Making matters worse, the September contract for Iron Ore on the Dalian exchange also closed 7% lower after trading down to its 8% limit for most of the session.

The sharp fall in Iron Ore will have its biggest impact on BHP, RIO and the Aussie Dollar.

The AUD/USD closed the New York session at a 1-month low of .7495. This is the first close below .7500 since early January and opens up the next support level at .7425.

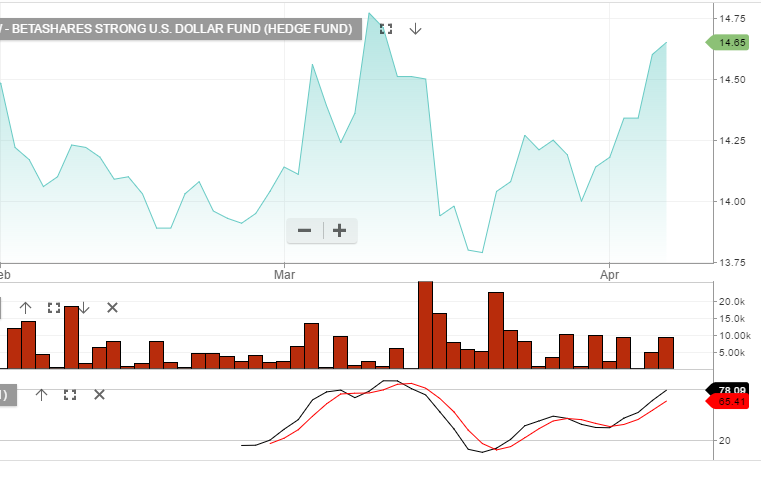

Investors who would like to profit from a lower AUD/USD can look at the BetaShare YANK Exchange traded Fund. This is an inverse fun which gains value as the AUD/USD falls.

Call in for more details about YANK and the other ETFs that we cover.

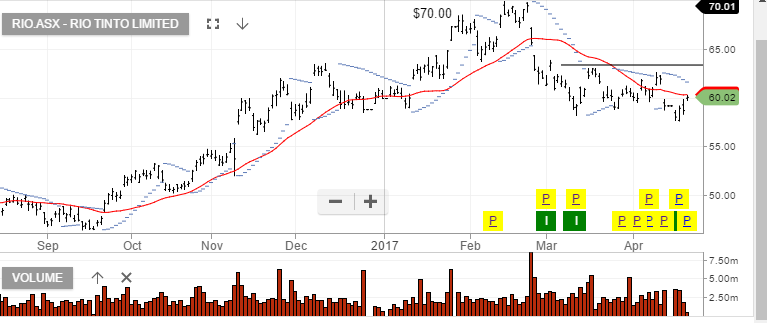

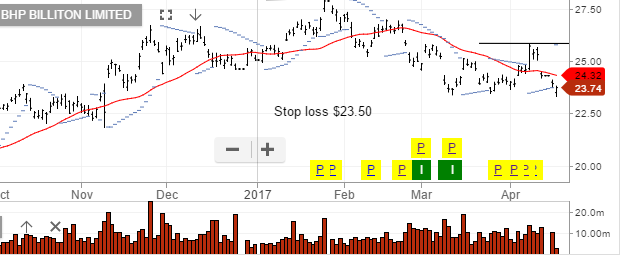

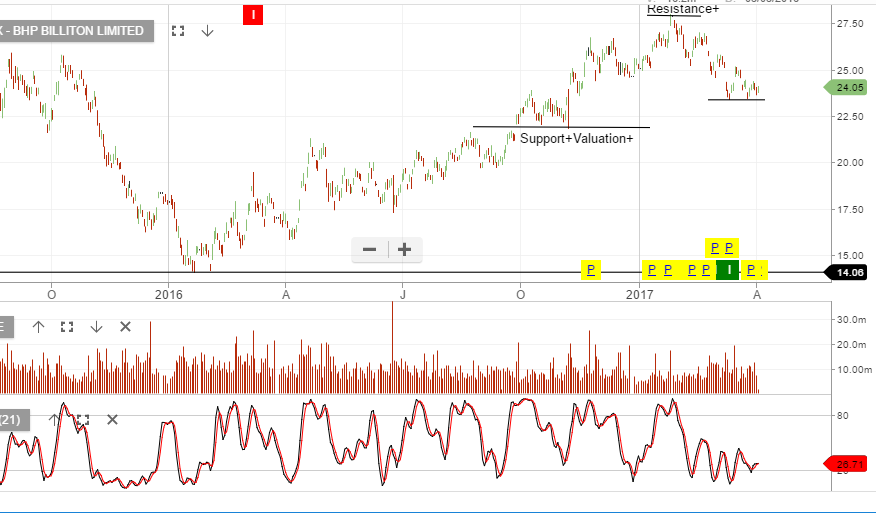

The share prices of RIO and BHP are both approaching key support levels which could create investment opportunities.

The are both trading below their 30-day moving averages but are close to support $58.80 and $23.50, respectfully.

The attached charts show that these support line have held and became good buying levels for a move higher over the last six months.

However, we are mindful of the importance of exports to China for both of these companies. Overnight, China’s five largest banks reported earnings which showed steady results but increases in the percentage of non-performing loans tied to real estate.

It’s worth noting that Chins’a top five banks are considered the largest in the world in terms of assets. A sharp contraction in any of those five could trigger weakness in RIO and BHP

Our Algo Engine has triggered multiple buy signals across the major resource names, both in metals and in energy.

With the peak to trough sell-off among the sector extending between 13% – 20% it’s likely we find some value investors stepping back in to the market.

We’re comfortable with select exposure in BHP, RIO, S32, WPL, OSH, ORG but caution investors that stop-losses below the recent lows will be a prudent way of managing risks.

It seems unlikely that any buying interest from this level will carry the above names to new near-term highs. We’re of the view that a corrective bounce will top out at 5 – 7% above recent lows

We see the recent volatility in oil and iron ore, being primarily driven by US Dollar swings rather than related to any fundamental factors and remain cautious of negative news flow from China’s unsustainable debt problem within their shadow banking industry.

RIO has delivered a solid CY16 earnings result of US$5.1b. A highlight of the result was the increased shareholder returns, with RIO announcing a final dividend of US$1.25ps

Revenue of US$35b, EBIT of US$7.8b and DPS of US$1.70 placing the stock on 3.3% yield.

Looking out over 2017, we expect a relatively flat market for iron-ore prices which will translate into only moderate EPS gains for RIO (5-10%). We assume revenue of US$38b and EBIT at US$9.5b, EPS $3.20, DPS US$2.50, which will place the stock on a forward yield of 4%.

Share buy backs and capital returns will help underpin the story here with RIO.

We see both RIO and BHP fully valued at current prices. With short term volatility likely ahead for Iron-ore prices, we recommend taking profits or selling covered calls to enhance the yield.

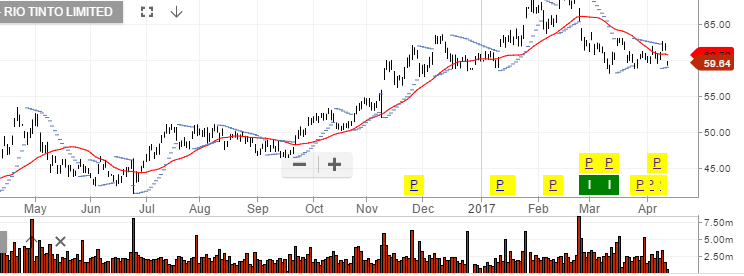

Chart – RIO

Sophisticated Investor?

We have special opportunities available for Sophisticated Investors. If you're interested, and qualify, please provide your details below.

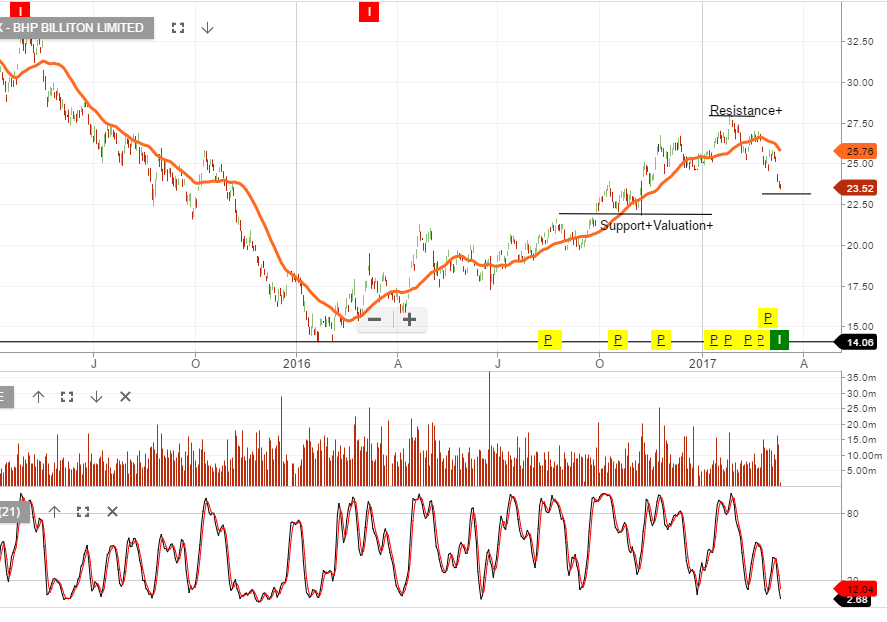

Chart – BHP

Chart – BHP