Our Algo Engine has triggered buy signals in Sonic Healthcare, Resmed and CSL over the past few trading sessions.

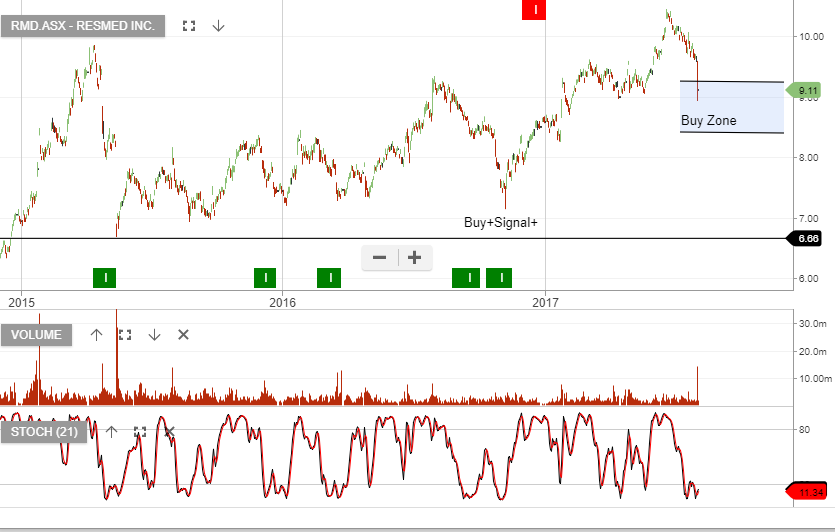

RMD has experienced its first sell-off since rallying from $10 last year to $16 only a few weeks ago.

The ALGO engine is now flagging the new “higher low” at $14 and we suggest buying a 1/2 size allocation here and then waiting to see if we get another ALGO signal to add to the position.

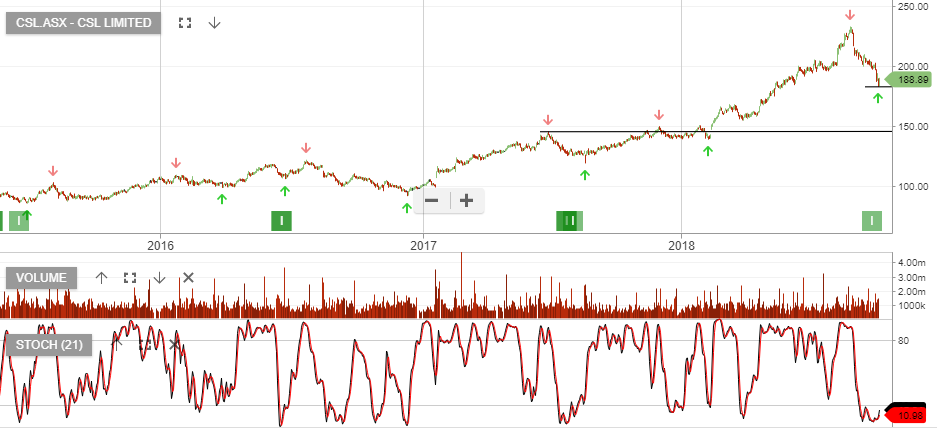

CSL provides good long-term fundamentals. The PE is still expensive, however, 10 – 20% EPS growth is attractive! Accumulate at $180

SHL looks to be good value at $23. We see resistance is $25, so look to sell call options to enhance the return.

Global mask sales were weaker than expectations, but we see F18 device and mask growth rebounding.

FY18 revenue is forecast to grow by of 5%+ and underlying EPS growth in the high single digits.

RMD is trading at 24x F18 EPS and we see the current sell-off as a buying opportunity.

We need to give this name a wide range to find support and the buying zone is between $8.50 and $9.25. 1, 2 & 3 years out, the stock will be trading at higher prices. Keep an eye out for the next Algo buy signal in RMD!

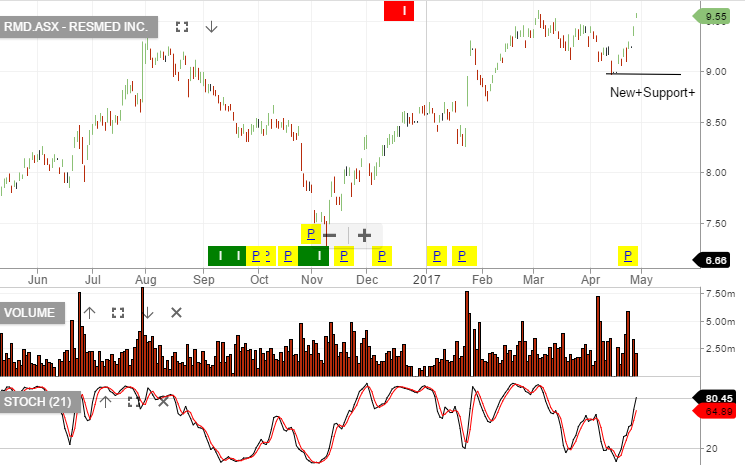

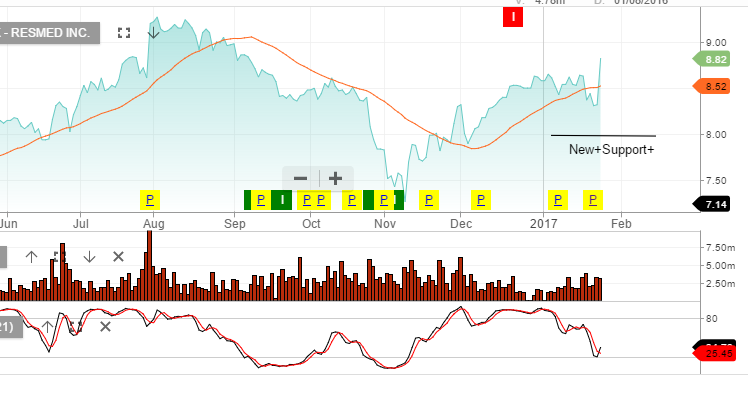

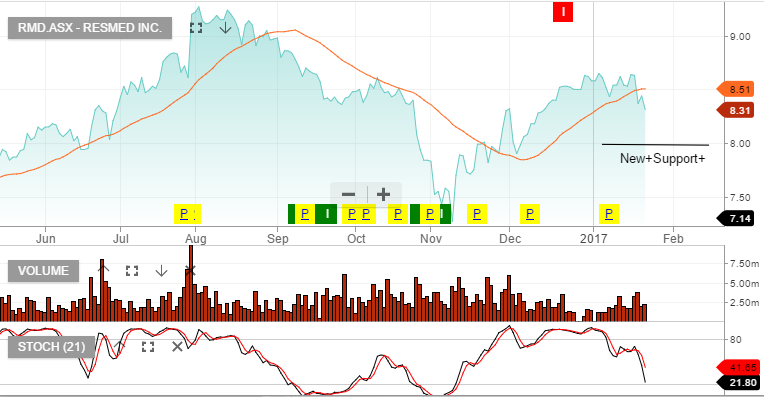

We like Resmed as a portfolio holding. Our Algo Engine triggered a buy signal in November 2016 when RMD was trading at $7.50. With the recent higher low formation at $9.00, we believe the price can extend higher to $10.00 before reaching resistance.

We hold CSL, RMD, RHC & SHL in our model portfolio. Over the next 10 years these remain a “buy on the dip” story and the Algo Engine will alert us to the next higher low formation for a discounted entry point into the stocks.

RMD reports tonight in US and we’re looking 15% EPS growth.

RMD will report their 3QFY17 results on 27th April. Early success of the AirFit 20 series should help to underpin year-on-year underlying earnings growth 15%+ to $US$520m.

FY18 we expect revenue of US$2.3b, EBIT US$580m, (from US$520in FY17), EPS US$3.10 and DPS US$1.45, placing the stock on a forward yeild of 2.1%

We like RMD’s growth outlook and therefore we’re encouraged to buy RMD ahead of the result and to add to the position on price retracements.

To help enhance the yield, we’re selling out-of-money call options, allowing for reasonable capital growth whilst at the same time increasing the cash flow from the dividend and call option income to over 10% p/a.

ResMed beat expectations by reporting Q4 earnings of 73 cents per share on quarterly of revenue of $530.40 million. During the same period last year, the firm earned 69 cents per share. This represents a 16.7% increase in revenue from the same period last year.

The street had estimated earnings of 70 cents a share on quarterly revenue of $518.60 million.

These earnings and revenue figures represent a return on equity of 23.10% and a net margin of 17.87%

We started buying ResMed last week, ahead of the earnings release. We’re now up 6% from our entry level and will look at add covered call options to further enhance the return.

Here is a list of the first group of companies reporting where we’ll be reviewing the earnings results and keeping you informed….

Resmed 24th Jan – Expecting better numbers following distributor de-stocking in the September quarter. New mask release should boost sales.

Tabcorp 2 Feb – Too early for any benefit from the Tatts acquisition, however, we’re looking for commentary on forecasts and cost savings.

James Hardie 2 Feb – US building cycle remains strong but we’re now cautious on James Hardie based on valuation concerns. Need to see EPS growth of 15%+

Transurban 7 Feb – We’re expecting strong free cash flow and minor dividend upgrades.

CIMIC 8 Feb – Expecting solid growth numbers and commentary on the integration outlook of UGL following the recent take-over

RIO 8 Feb – Good production numbers and we expect earnings to meet consensus forecast.

AGL 9 Feb – We’re concerned the market is too optimistic here and we will be looking at this result closely.

AMP 9 Feb – After the downgrades from the under-performing life insurance, we question what the future earnings look like. AMP as an asset manager is a very attractive business, we just need to re-establish the expected EPS growth rate.

Amcor 13 Feb – Looking for confirmation of 8% EPS growth

Ansell 13 Feb – FX impact could be a minor negative but the underlying business is improving. We’re looking for detail and timing on the pending corporate restructure strategy.

Chart – RMD

Sophisticated Investor?

We have special opportunities available for Sophisticated Investors. If you're interested, and qualify, please provide your details below.

Resmed

Resmed