Softer US Yields Could Lift Local Names

The recent move higher in longer-dated US Treasuries has created a headwind for some of the yield sensitive names listed on the ASX.

Over the last 10 days, the US 10-year notes have risen from 2.28% to just under 2.50%.

This 10% move has also lifted the 2yr to 30yr spread from 85 basis points to a full 100 basis points.

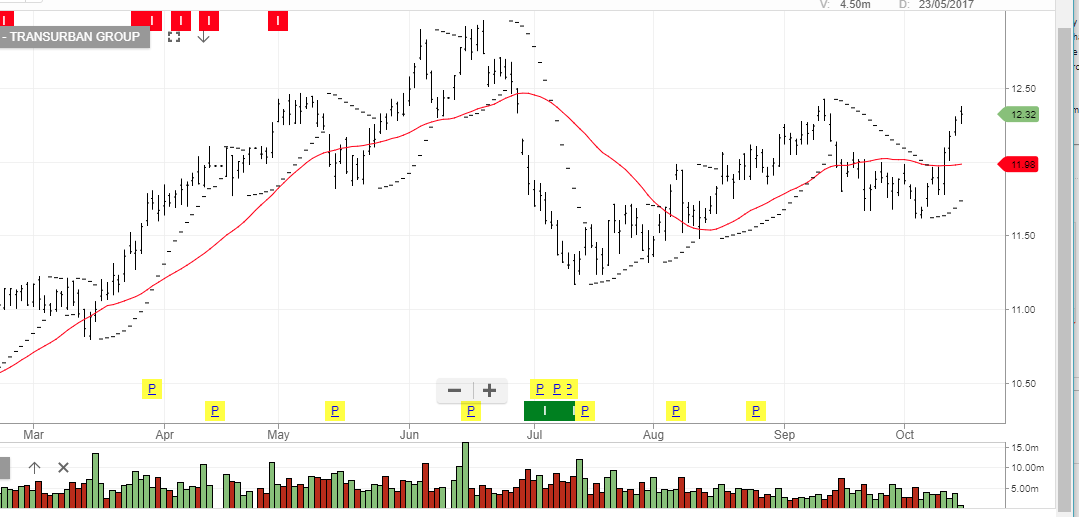

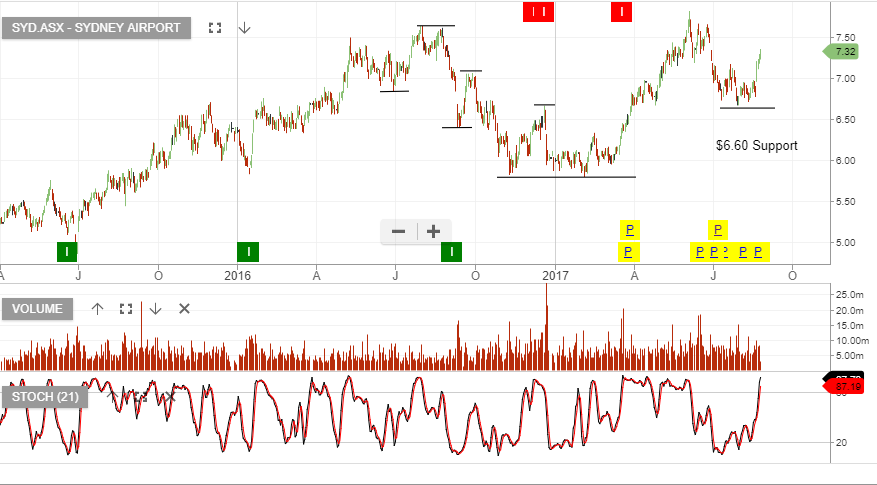

The impact on local shares has been a 4.5% drop in TCL and a 3.3% fall in SYD.

Looking forward, it’s reasonable to expect the US yields to soften and the yield curve to flatten.

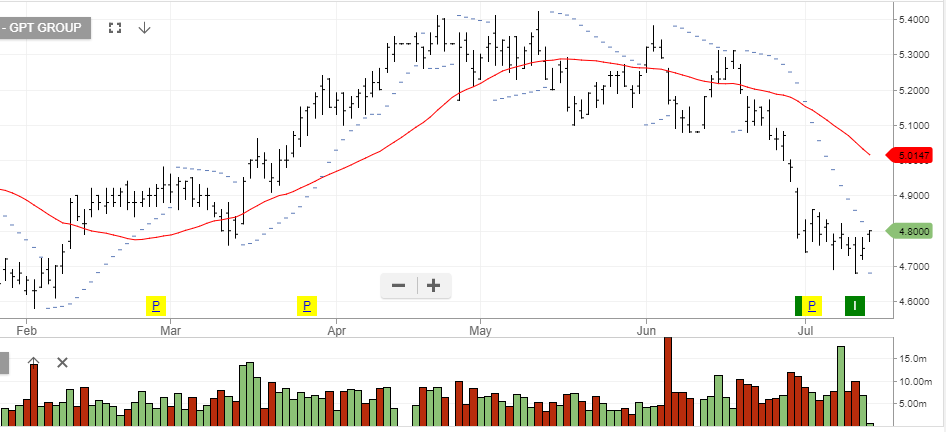

Given the current correlation to the local shares, we see the US flattening trade as potential positive for the local names such as TCL, SYD, WFD and GPT

US 2yr versus 30yr spread