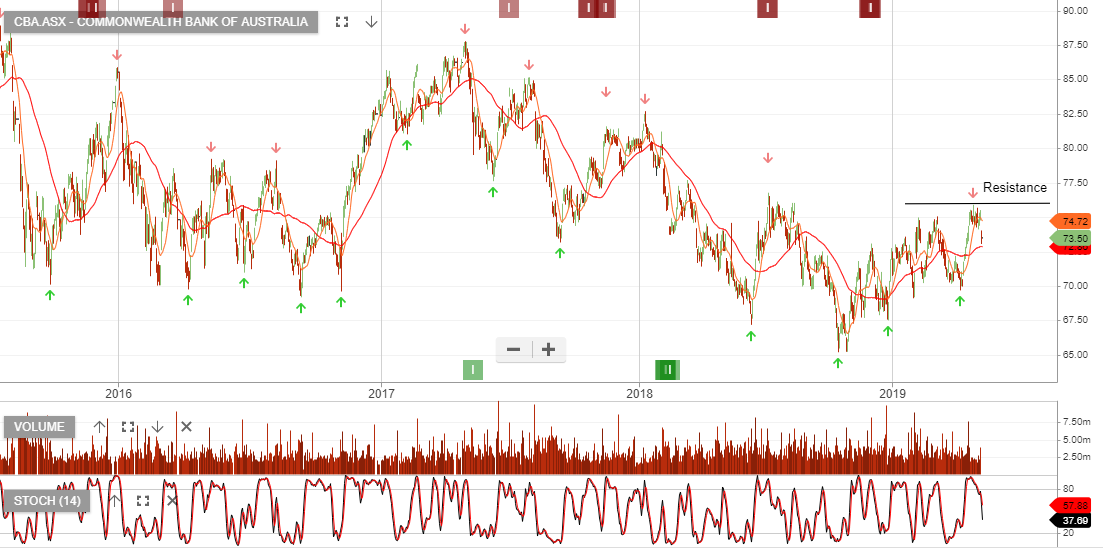

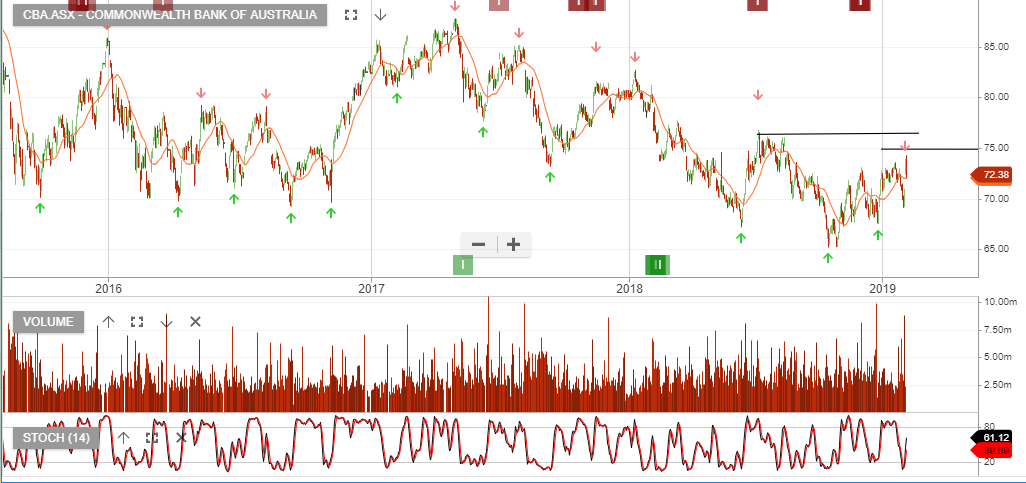

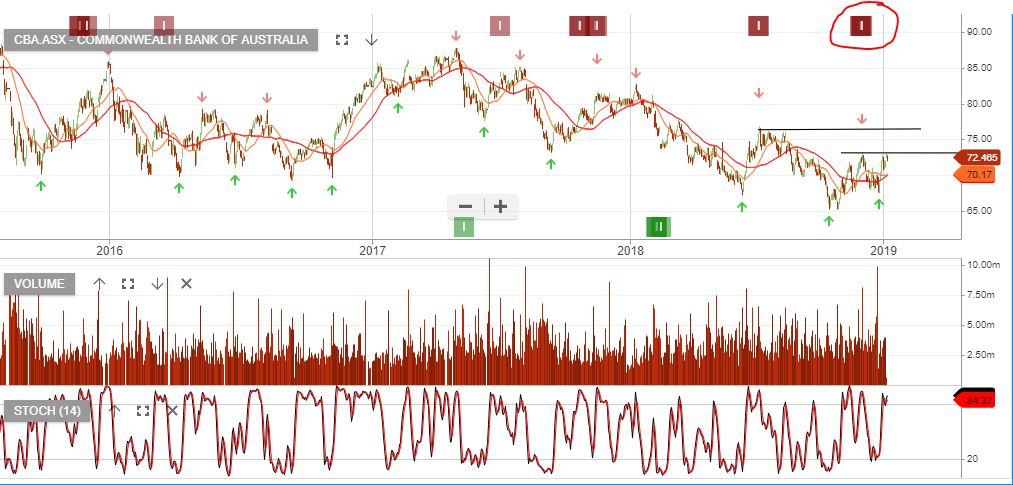

CBA – Earnings Report 12th Feb

Commonwealth Bank is priced for a strong result on February 12, so the potential for disappointment is high. The stock remains under Algo Engine sell conditions and despite the prospect of a $2.5bn on market share buy-back, we remain on the short side of the stock.

CBA has re-rated to a P/E multiple of 17x and a dividend yield of 5%.