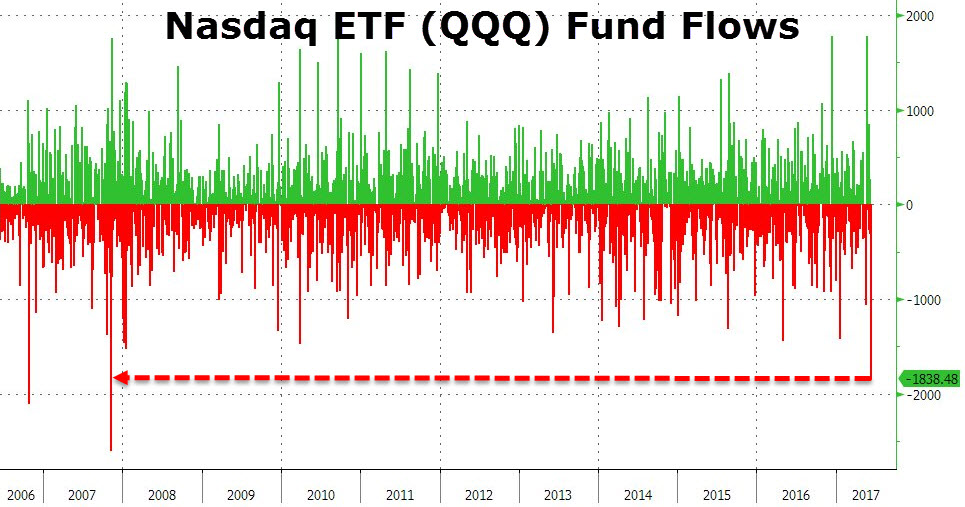

Dow Hits All-Time High As “Short Interest” Drops To A 10-Year Low

As both the Dow Jones 30 and the S&P 500 rose to new all-time highs this week, daily trading volume was 20% lower than the 3-month average and “short interest” in stocks fell to the 2007 lows.

Short interest is defined as the total Dollar value of stocks which investors have “sold short”, which they don’t own, with the idea of making a profit after buying them back at a lower price.

The combination of seeing the Dow and SP 500 rise to new highs on lower volume, and contracting short interest, is an illustration of a technical “short covering” rally.

Seeing index prices at new highs on lower volume suggests that “new money” is not coming into the market and that stock prices will revert lower after “short sellers” have taken their losses.

This technical combination doesn’t always trigger an immediate sell off in stocks. However, the market condition of “higher highs on lower volume” is often cited after a material correction in the market occurs.

As US earnings season goes into full swing next week, we’ll continue to watch the price/volume correlation and the potential impact on the market.